The Story of Tether — Stability Over Hype

Tether’s arc from controversy to ubiquity: reserves, transparency debates, USDT’s role in liquidity, and why traders still reach for it in volatile markets.

Of all the cacophonous moons and planetary bodies in crypto’s great digital asset galaxy, there is one which has broken into orbit around them all: Tether. It is the liquid that keeps the cryptocurrency market afloat, a lubricant that makes it possible for billions of dollars to change hands around the world in seconds, and also a massive but mysterious force that helps explain how markets keep moving up and down even as economic growth staggers. But what is it exactly? Where did it come from? To understand the phenomenon of Tether and its USDT symbol, we need to travel back in time — all the way to when the crypto scene was an English-speaking “Wild West” of volatility, idealism, and technical shackles. We’ve got to go back a long, long time to understand the void it filled.

It was 2013, and the world of cryptocurrency looked nothing like it does today. Bitcoin was catching on, but it was famously volatile. It might fall 20 percent in one day, taking away the purchasing power of anyone who was foolish enough to think of it as a short-term store of value. For both early adopters and investors, this volatility was a two-edged sword. It presented huge upside potential, but it meant Bitcoin was a lousy medium of exchange for day-to-day business. If a trader ever wanted to get out of a position, they had to sell back into fiat currency — US dollars or Euros. This was laborious, costly and rife with friction. Banks were wary of crypto companies and would frequently freeze accounts or delay wire transfers days on end. There was no middle ground in cyberspace; you were on the rollercoaster or you had been thrown out of the park altogether. What the market demanded was a digital asset that moved like Bitcoin but held value like dollars.

In addition, no such thing as a stable digital currency so arbitrage between exchanges was almost always too risky an opportunity. If by chance Bitcoin was selling for $500 on an exchange in Tokyo and for $520 on an exchange in New York, a trader couldn’t easily take advantage of this divergence because moving fiat money between these jurisdictions took days, enabling cross-border arbitrage only after the opportunity had disappeared. The lack of efficiency resulted in huge disparities (known as premiums) and slowed the market’s evolution. The industry required something swift like the blockchain but stable like a central bank.

From Realcoin to Tether: History

It was out of this requirement that Tether’s predecessor came about. Launched as “Realcoin” in Santa Monica, California back in July of 2014.

Joining forces were Brock Pierce, a former child actor; Reeve Collins, who would go on to be the company’s first CEO; and Craig Sellars, coder and longtime student of the Bitcoin protocol. It was a daring but simple vision: to build a cryptocurrency that is pegged one-to-one with a real-world currency. Where Bitcoin had no backing other than what the market was willing to bear, Realcoin would be redeemable for fiat, turning it into a kind of digital voucher like that offered by British banking system Clearing House Automated Payment System.

The technology was developed based on the Mastercoin protocol (renamed later as Omni Layer), that formed a second layer over the Bitcoin blockchain. This enabled them to create metadata in the OP_RETURN field of Bitcoin transactions which effectively created new tokens that leveraged Bitcoin’s security while possessing unique properties. That was quite a hack, at a time before Ethereum and smart contracts came along and made it trivial to create tokens. The team rebranded in November 2014. “Realcoin” seemed rather generic, maybe too much like all the “altcoins” saturating in the market. They opted for a name describing better the token’s nature — its value pegged was to a fiat friend. Thus, Tether was born.

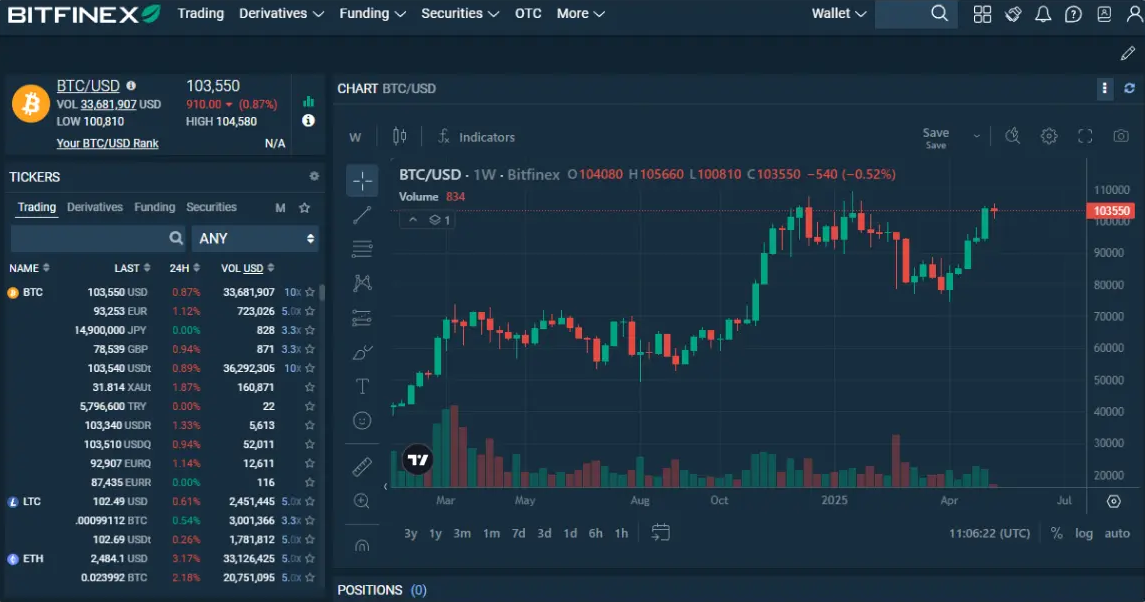

It was hardly glamorous in the beginning. The stablecoin was met with skepticism. The early crypto community’s libertarian ethos was heavily skeptical of anything related to fiat currency or centralized banking reserves. However, the utility was undeniable. The first cryptocurrency exchange to integrate Tether was Bitfinex, which would be closely associated with its history. Bitfinex introduced trading pairs against USDT where you could hedge your portfolio and never have to touch a bank account. This was a paradigm shift. It was grease for the markets, greasing arbitrage and liquidity provision.

Banking Blockade and Survival

But the path to preeminence was fraught with challenges that would have killed a lesser offspring. One of the earliest high-profile tests happened in August 2016 when Bitfinex was catastrophically hacked and lost 119,756 Bitcoin. Although this wasn’t a hack of Tether, the two companies’ fates were already interlinked. Bitfinex’s choice to socialize the losses among all users (by issuing “BFX” tokens that reflected their share of the debt) established a bond of common suffering and eventual healing that permanently bonded its user base when those tokens were eventually redeemed at dollar value.

But the real existential threat to Tether came in early 2017. The traditional banking system fought back as the crypto market was heating up. Two years later in April 2017, Tether lost its main banking relationship with correspondent bank Wells Fargo and received only temporary relief so that it could transfer funds out of the account and into one held at another intermediary bank. To a normal company trading in dollars, loss of banking access is a corporate death sentence. Tether essentially ended up frozen out of the United States financial system. It triggered an era of wild improvisation and opacity that fed years of conspiracy theories. Since its founding in 2010, the company had been reduced to using an ad hoc network of payment processors and shadowy banking partners to move money. This was when the “Bitfinex and Tether” story developed into a key industry drama.

This theater was compounded later in the year when the “Paradise Papers” leak showed that there were major overlaps in who managed Bitfinex and Tether — Philip Potter and Giancarlo Devasini specifically, contradicting past assertions that they were controlled by separate entities. Critics said USDT was being "printed out of nothing" to hold up the price of Bitcoin, in a theory reminiscent of the 2017 "Willy Bot." Researchers at the University of Texas have even written one paper after another suggesting that Tether issuance was timed to stave off Bitcoin downtrends. And yet, despite these scandalous allegations, Tether's market capitalization continued to expand - driven by voracious demand for a stable settlement layer amidst the historic bull-run of 2017. Traders were dismissive of the FUD (Fear, Uncertainty and Doubt), they needed a solution to move value between exchanges which didn’t possess fiat rails.

Lawsuits and Search for Transparency

This is when the “Stablecoin Wars” of 2018 introduced a new wrinkle. The company Circle issued (USDC) one of a whole bunch of “regulated” stablecoins that have come out, promising transparency and compliance with US law. The story went, that with these “safe” options institutions would rush in and leave the “offshore” Tether. Yet, the opposite happened. One saw adoption in DeFi, the other proved to be king of liquidity. The market valued Tether’s censorship resistance — or at least the appearance of it — more than regulatory compliance. Being offshore was a feature, not a bug.

It all came to a head with the beginning of New York Attorney General (NYAG) probe that kicked off in 2019. The investigation revolved around claims that Bitfinex had relied on Tether’s reserves to hide an $850 million loss of client funds. They were funds that had been confiscated by Polish, Portuguese and US law enforcement from Crypto Capital Corp., a Panamanian payment processor controlled by Reginald Fowler with whom Bitfinex was compelled to do business after the corresponding account at Wells Fargo shut down. The investigation was a crucible for Tether. It showed that at any given time USDT was not actually 100 percent backed by cash in a bank but partially-backed by an unsecured loan to Bitfinex. The announcement rocked the market, but most importantly, the peg stood.

The settlement with the NYAG in February 2021 was a turning point, involving an $18.5 million settlement and a ban to operate out of New York for Bitfinex. Instead of killing Tether, it made the company grow up. They started issuing quarterly attestations on their reserves. This led to a fresh round of scrutiny, this time over what the reserves consisted of. At one point a big chunk was in commercial paper — short-term corporate debt. Critics warned that this was risky, as fallout could spread from the implosion of Chinese real estate giants such as Evergrande. In response, Tether underwent a huge overhaul of their portfolio by gradually removing commercial paper replacing it with US Treasury Bills. In the process, they not only de-risked the asset but transformed it into a profit machine with interest rates tightening globally.

World Domination and TRON Effect

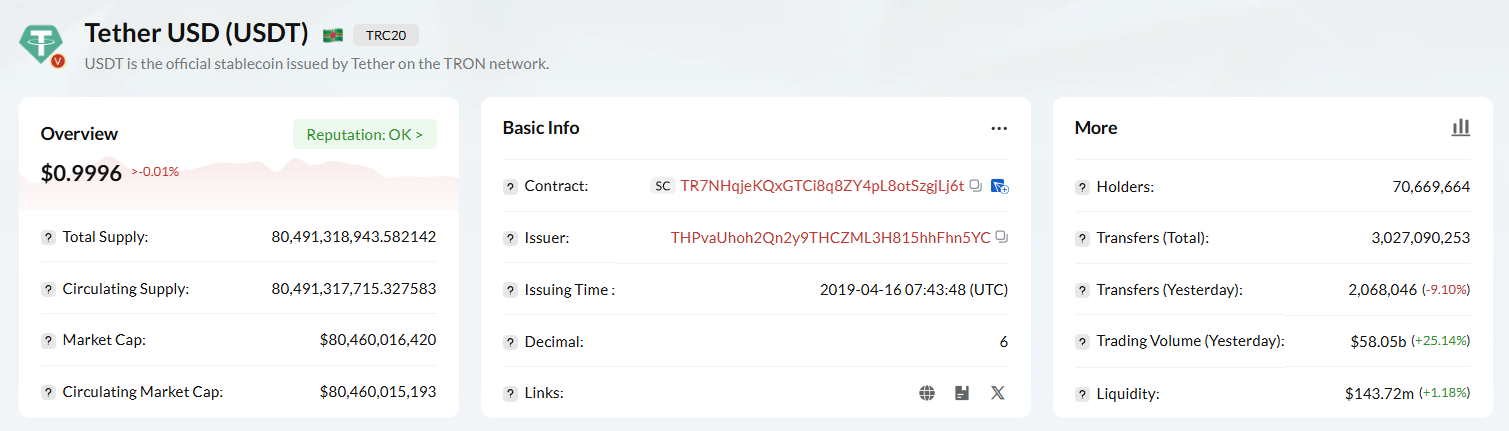

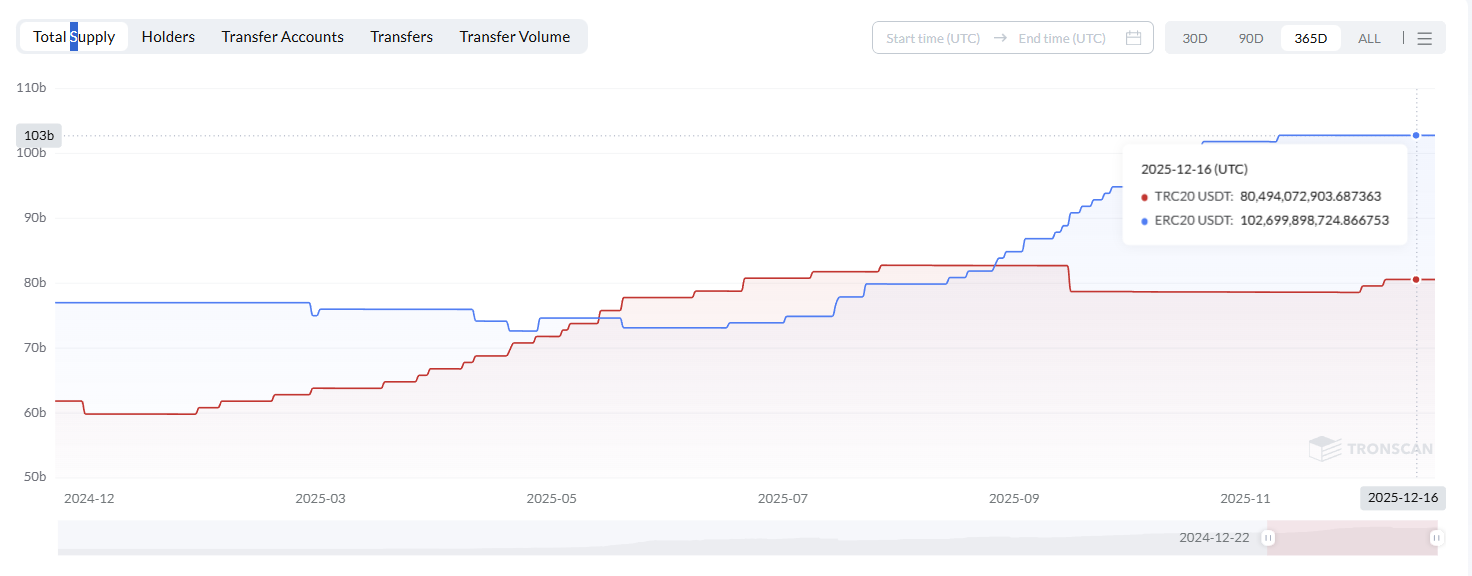

So, why Tether? Why did it prevail when the likes of USDC or algorithmic stablecoins like UST tried to take the throne? It has to do with the nature of what you’re accessing and just utility (aka, the “Lindy Effect”). Tether was the first mover. It had the most liquidity, famously serving as base pair in the “3pool” on Curve Finance during DeFi Summer 2020. When traders had to get out of a position in the crash, they didn’t care about regulatory niceties; they cared which pair had the most volume. USDT was everywhere. What’s more, Tether surged aggressively outside of the Bitcoin Omni layer. Its jump to the Ethereum network and, importantly, to the TRON network was absolute genius. It was no longer a question of sending USDT only for high frequency trading, but also possible for micro-transactions and payments in third-world countries with the low fees and fast speed provided by TRON network.

The growth of USDT on TRON is unprecedented. While Ethereum was grappling with gas fees that could be in the $50 range to make a transfer of $100, TRON provided transfers for pennies. This accessibility meant that USDT became the default currency of millions of people in the Global South. USDT proved to be a lifeboat for locals in countries such as Turkey, Argentina and Lebanon, where the value of their local currencies was being decimated by hyperinflation. It was no longer just a trading tool; it was a way to survive. This organic uptake created a floor of demand that “corporate” stablecoins such as USDC would never be able match. Whereas USDC was a darling of the DeFi crowd and Silicon Valley boardrooms, USDT had been swapped on street markets or over-the-counter desks in Asia and Latin America.

The history of Tether, though, is not one that can be told without the people who guided the ship through these storms. The new parent company also rolled over quite a few existing talents after the original owners had moved on and van der Velde with Giancarlo Devasini (CFO) managed to keep things running. But the public face of Tether was now Paolo Ardoino. The company's former CTO, Ardoino, an Italian computer scientist, interfaced directly with the community. He didn’t take refuge within an ivory tower — instead, he got into arguments with critics on Twitter, explained technical details, and promoted the idea of what is known as resilience. His ascent to chief executive heralded Tether’s journey from a secretive start-up into a global financial juggernaut.

Geopolitical Financial Powerhouse

This transformation is reflected in its current business model. We’re no longer talking about a niche crypto tool. We are discussing a geopolitical financial weapon. This was amply demonstrated by events that took place in the later months of 2024, particularly in the year 2025. And in a major regulatory victory, Tether said that the United Arab Emirates has formally adopted USDT as a compliant fiat-backed token. This distinction will permit licensed firms from the region to operate legally with the stablecoin, which paves way for institutional adoption in the Middle East.

And the company’s ambition has spread into more traditional sectors, using its ample profits. Reaching back to the ancestral home of its leadership, Tether made a bold power play in sports. In June 2025, the company was second-largest shareholder in the Italian football club Juventus F.C. This interest is both personal and strategic: Tether’s public face and figurehead, Paolo Ardoino, is an Italian. They even made a bid to the club in December, offering to purchase Exor’s majority stake at €2.66 per share, and valuing the club at more than €1 billion. The offer was rejected by the Agnelli family, but it was an audacious reminder of how stretched thinly Tether’s mega leverage made it.

Another development is that the new wealth wizards have amassed hard assets. Tether is even becoming a captain of industry in the commodities space. The firm added 26 metric tons of gold in Q3 2025 bringing its holdings to a total of 116 tonnes, more than any Central Bank globally during the period. That aggressive diversification has made Tether a massive whale in the gold market, reinforcing its digital tokens with material, time-tested value.

The tale of Tether is a story of survival. It persevered through banking blockades, regulatory assaults, mistakes within and outside its own walls — and the fall of even its competitors. It showed that in the world of crypto, it’s all about stability and liquidity. Sending USDT is as ubiquitous today as sending an email is in many parts of the world. It’s used as remittances in Lebanon, savings in Argentina, and for B2B payments settlement across Asia. It’s a kind of parallel banking system for the unbanked.

But even as USDT is the alpha dog of stablecoins, the technical grist of using it in practice — especially on USDT’s most utilized network, TRON — comes with its own technical quagmires. Even though TRON is faster and cheaper than Ethereum, it works on something called “Energy” and “Bandwidth.” Every transaction consumes these resources. In case another user doesn’t have enough Energy in the wallet, the network burns some amount of TRX for covering the fee. This provides a “Catch-22” scenario for millions of users, they have USDT but no TRX. They can’t just transfer money by shifting some funds; they first have to go on an exchange, buy TRX and then withdraw it to their wallet — a cumbersome process that creates immense friction for basic payments.

And this is where contemporary offerings like the Netts Transfer Tool come into focus, designed to remove that friction without needing anyone! It's like a utility to be able to send USDT on the TRON network without having to own any TRX and not have to deal with ever complex Energy/Bandwidth system. The mechanism is running on a “zero Energy fee” model, where the commission is instantly paid right in USDT that you are sending and nothing more, making it easier than ever.

This is such a simple, ingenious mechanism. The user needn’t set up its own Energy rental or deposit some TRX for staking however, the service does it in the background. All that the user needs to do is connect his wallet (TronLink for example) and enter the address of the recipient then sign the transaction. It uses the current network fee to compute the amount and subtracts it from the transfer value.

This gets rid of the “Energy wall” that aggravates most casuals. It turns what’s an ordeal of several steps involving exchanges and gas tokens into a seamless process. For businesses and developers, it is far more versatile because it allows recipient to pay the fees which in effect allows for USDT to be integrated without requiring end recipients to have TRX. At a time when Tether is working towards global mass adoption, solutions that act as blinders to the complexities of blockchain mechanics are what's left to seal the deal by proving that stability isn't just an idea - it’s something any user can depend on.