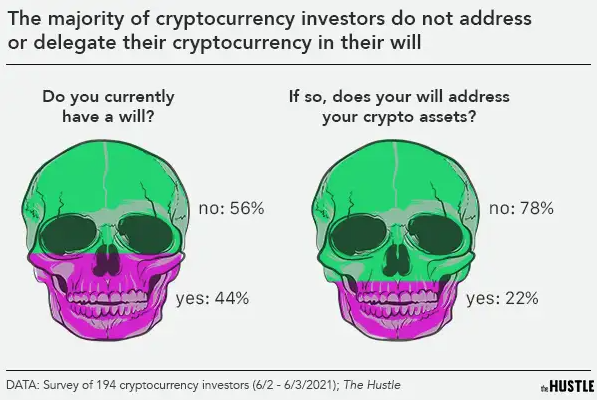

Crypto and Death: Coins Left Behind

When the holder dies, private keys often die with them — inheritance, volatile valuation, cross-border probate and the millions of Bitcoin already lost forever.

In our previous article, we examined the unavoidable machinery of crypto taxes. So, the one that tackles death — which is the other notoriously unavoidable thing — and the bizarre, undignified mess that ensues when much of a person's net worth is imprinted in strings of characters only the deceased was ever able to see?

Inheritance law is old. This approach has been honed for hundreds of years to cover houses, shares, bank accounts, jewellery, family businesses, and every combination of material and paper wealth humans have come up with the idea of passing down. What it has not been honed to work with is an asset class whose ownership is literally encoded in a secret known only to the owner, whose price fluctuations rival that of the stock market on a Sunday afternoon, and whose legal classifications ranges from property to commodity to security to whatever nebulous status that happens to describe when your breathed your last on this side of this border. At this point, the inheritance law of the blockchain-era is one that resembles law less than a pirate codex.

Keys Without Owners

The core issue is straightforward and often overlooked. These ways can be imposed by the court because the original possession exists inside some system — a bank, a land registry, a brokerage — that will attend court order. A judge signs a paper, a custodian executes an action, and the asset goes. Cryptocurrency kept in self-custody is not in any such system. It resides in a wallet whose ownership exists solely in the form of that private key. That wallet is essentially not owned anymore if only a dead person has access to that key. Not lawfully — the property still legally alive — but practically. You can see the coins on the blockchain. Everyone can see them. Nobody can move them.

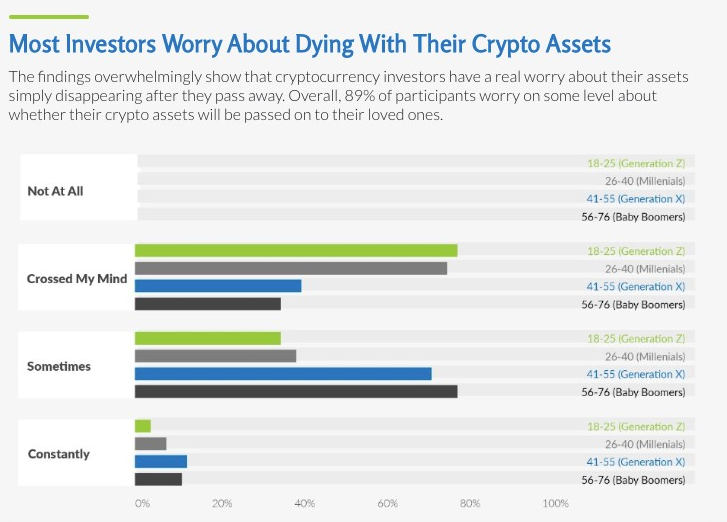

The statistics about this issue are striking. Even though estimates vary, most serious analysts agree an estimated two to four million coins should be considered permanently lost — or eleven to eighteen percent of total supply. That total counts early adopters who tossed hard drives before bitcoin was worth anything, miners that got lost to small balances and — most relevant to this article — dead people who left families with no way to get what they owned. By some accounting, this last category alone amounts to the hundreds of thousands of coins worth tens of billions of dollars at current prices. The first generation of crypto-people is coming of a certain age into their 60s and 70s, and the statistical curve around "people who held significant amounts of Bitcoin since 2013 and never wrote their seed phrase down" is not encouraging.

This is a chillingly familiar worst case scenario for anyone with skin in the game in crypto-adjacent legal practice. A father dies. The family is aware he was a Bitcoin holder — he would not shut up about it. They might even see the documentation displaying tens or hundreds of thousands of dollars in holdings from years in the past. And sometimes, the wallet address is perfectly clear on the blockchain. But the seed phrase, the hardware wallet, the handwritten note in a drawer — none of it exists. In essence, what the estate possesses is a legal claim on assets that — for all practical purposes — are locked away forever behind an impenetrable doorless vault. The children go to the funeral, enter probate, and then inherit nada, because the nada is cryptographically perfect.

Bizarre tales such as this have started to regurgitate regularly now. The most notorious is the late founder of a Canadian exchange, who in 2018 was the only person with access to the cold wallets where customer funds were stored, and unexpectedly died on a trip abroad. About $190 million in customer assets went missing with him, and years of forensic investigation and litigation have left little trace of recovery. Few private family cases ever reach this magnitude, however they often play out in a very similar way: demise, bewilderment, a frantic rummage through private information and devices, and, usually, a gradual recognition that what was notionally left has in reality boiled right down to be ungraspable.

Valuing What Moves

(To be fair, say the keys are located.) The wallet is accessible. There is a consensus around what is in it. So this leaves us with the question: what value does it have?

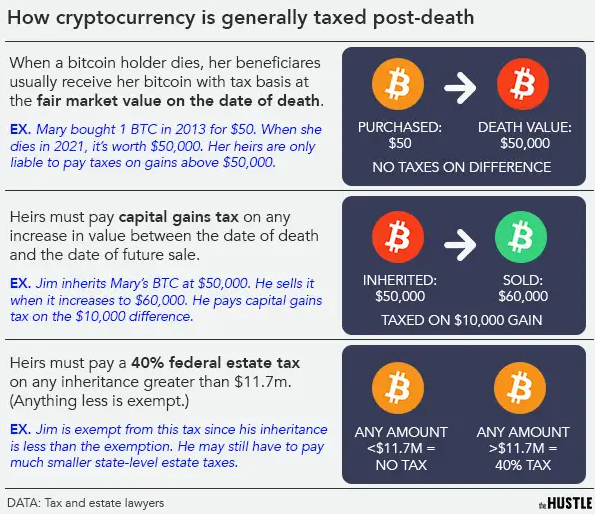

For estate purposes, US tax law classifies crypto as property, valued at fair market value on the date of death or alternatively six months later. It sounds easy — until you realize crypto markets are open twenty-four hours a day, seven days a week, even on the day of the death. There is no closing price. At 2:17 a.m. on a Tuesday there is a price, and at 3:04 p.m., there is a price, and those two prices can vary by significant amounts. What the IRS eventually choose to settle on is the price on the exchange where the trade that would have been executed at the moment of death took place, but this leads to arguments of its own — which exchange, which timezone, which averaging methodology.

This is where the valuation problem meets the fairness problem. Say a will devises the family set of wheels to one of the children and the other a wallet with two Bitcoin. The two bequests have an approximately equal value at the time the will is executed. The car has lost at least half its value (as cars tend to do), the wallet is now worth double, or 1/3 — whichever the funeral week happens to fall. They never disagreed before; now they argue. The person who got the car can cite the will as evidence the parent wanted to be fair, and the person who got the wallet can cite the current price as evidence that market forces have betrayed the will's intent.

And then there is the step-up-in-basis rule that further complicates the picture. In the U.S., the heir inherits the asset at its fair market value on the date of death instead of the original cost. That can be a boon — an old Bitcoin purchased for $300 and inherited at $60,000 resets its cost basis for capital-gains purposes so that the heir who sells immediately is taxed only on anything that moves from that date. If the heir HODLs through a crash, that can also be a trap — the basis doesn't reset down on its own. These are just the sorts of details that sound technical until they suck ten percent out of the estate.

Whose Court, Whose Law?

That may not be that weird, but it gets weirder when the family is across the country — and often they are. A father passes away in Germany and holds crypto on an exchange in Singapore with a daughter in the US, son in Portugal, and a will prepared in accordance to British common-law standards. Which jurisdiction's valuation rule applies? Which inheritance tax? Is this an asset classified as an asset — property, financial asset, personal item? The answer is always some maddening mix of all, solved by treaty wherever possible and through costly litigation where not.

There are fourteen countries with which the United States has estate-tax treaties, and these do provide assistance, but they do not make the problem go away entirely. Generally the U.S. estate tax applies only to U.S. situs property and the classification rules for where cryptocurrency is considered to be located are not yet fully developed. If an American device accessed the wallet, is crypto U.S.-situs? What if the exchange is registered in the state of Delaware? If the heir is American? Tax authorities have given various answers, in some cases even within the same year, so that the practical effect is that a family with meaningful crypto holdings spread out across multiple countries may pay inheritance tax on the same assets twice over in two jurisdictions, each of which will believe it is the correct claim.

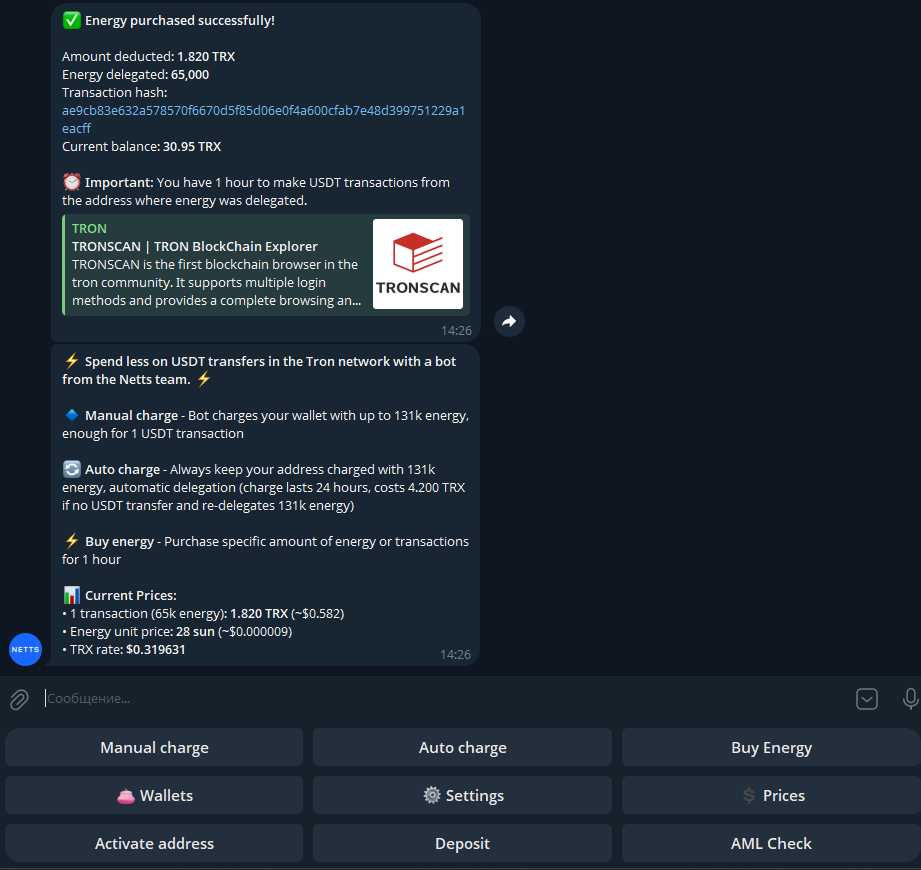

Then the mechanics of actually moving the coins… However, without access to the wallet [itself] the assets have to be either allocated or transferred. Suppose you have three heirs in three countries and each heir is entitled to one-third of the estate, somebody or something has to do the transfers, pay the network fees, and manage the timing. In fact, getting USDT over the chains like TRON needs Energy and Bandwidth. If the executor didn't know to refill Energy from a rental service before the transaction, the network will get it from burning of TRX simply (and this happen again and again over dozens of estate transfers). A somewhat tech-savvy executor using something like a TRON Energy bot can cut that friction down considerably; a random who doesn't know that this tool exists will just throw a couple hundred dollars to the network for no reason.

Deathbed Instructions

Let's turn to another situation: Less adversarial, but no less complicated to deal with. A father who has years of experience in the crypto since 2014. He is a true believer. He has seen his positions rise, and fall, and rise again, and he has some even more passionate opinions about what his family ought to do with his holdings on his passing. As for his will? It reads crystal clear: the Bitcoin will remain sealed for five years, at which point it will cover his grandchildren's tuition fees. He has no doubt that in five years the price will be orders of magnitude higher. He writes it in.

Then he dies. The heirs look at the plan. The market just dropped 40 percent. The kids are grown, with tuition payments coming due in eighteen months, not five years. Taken literally, the will forces the family to sit on a depreciating asset for another few years while the bills mount and the market continues to do whatever it is that the market is always doing. The testamentary visionary had faith; his successors have mortgages.

Crypto makes this acute not just because the time value of money is so compressed, but because this is a surprisingly common type of conflict in estate planning involving volatile assets. Although the courts tend to enforce the express wishes of the deceased, they can do so, at least in limited circumstances, only if that mechanism furthers that purpose of the bequest; if it does not, the practical interests of the beneficiaries may prevail. The heirs will likely find themselves in a court arguing that the holding period was advisory not mandatory. The estate may sell for a poor price just to finally put the disagreement behind them. In any case, the exact intent of the deceased does not survive first contact with the other people who have to live with it.

The reverse happens too, and is equally hurtful. Otherwise a family sells the inherited crypto as soon as they can, cashing out of the market on the day probate is settled, and they move on. Five years on, the coin is five or ten-fold the value at which the heirs sit hand-rubbing, behind closed doors, calculating how much of a slam-dunk they left on the table by not carrying out the instructions of the dearly departed. That would not be an ideal outcome here. Volatility generates regrets both ways. Holding was wrong. Selling was wrong. Neither is satisfying, and both are defensible.

A growing workaround for this, the crypto-specific trust, is a legal construct that essentially holds the digital assets for the benefit of the beneficiaries under terms the grantor picks for themselves while alive. A trust could provide for simultaneous or staged emptying or for a professional trustee with discretionary power to act if the original author could not have foreseen other contingencies. It is expensive to create and maintain, but it does prevent forcing the heirs into the false choice of either turning over all control with one voice to an instruction years out of date, or compelling them to publicly disregard the wishes of a deceased. This is the default recommendation among estate planners who understand crypto for large estates with significant crypto exposure.

What Actually Works

The uncomfortable truth about crypto inheritance is that it is not so much a legal issue as an operational one. The law, as clunky as it is, mostly copes once the coins are in circulation. The real flaw is what is happening before any lawyer steps foot: the private key, and no one to use it.

Over the past ten years several methodologies have come about to deal with this ranging from the simple and risky to the intricate and stable. The most basic form is a sealed envelope containing a seed phrase and stored within a will or in a safe deposit box where the named executor has access. The in-between is a multi-signature wallet, generally requiring two of three keys to move assets — one with the owner, a second with a trusted family member and a third with a professional custodian, which means that the loss of a single key is not fatal, and that the compromised authority of a single key is not deadly. A slightly more complex solution creates dedicated legacy services that store key material encrypted, with access to pre-registered inheritors released after a verifiable death, sometimes using dead-man's-switch systems that automatically trigger when the owner fails to check in on some cadence.

Each approach sacrifices some access for security. A multi-sig in the hands of three people give huge protection but also require that all three remain alive, sane and findable, a seed in a drawer is accessible, but also readily stolen, and now you introduce the 3rd counter-party risk of the capitalist inheritance firm which hereditary crypto purists have traditionally avoided. The answer largely depends on the size of the holdings, the family constellation, and the jurisdiction. The wrong move — inaction — is by far the most prevalent, and the single largest factor in why so many coins are irreversibly out of the market ever again.

Courts and estate practitioners are slowly but surely catching up. Crypto-aware wills are standard-issue digital-executor clauses. Today, there are companies specializing in providing probate assistance for estates with significant cryptoassets. While some regions have started putting digital assets directly into their inheritance law, the field remains fragmented and most rules are being decided on a case-by-case basis. One day, this will be a lot less chaotic than it currently is. Until then, preparation as an individual is still the separator between a family inheriting wealth and a family inheriting a mystery.

Ultimately, the last reminder is to discuss it while you are still alive. Many crypto families are secretive — sometimes for valid security reasons, sometimes for general mores, and the secrecy extends to neither talking about what is going to take place when the holder passes away. But no one inherits that of which he is unaware, nor can any executor perform a will that was never delivered. Costing not a single cent, a conversation with an assigned one member per family annually and updated each time the portfolio materially changes, save the most avoidable losses. The coins are indifferent to the conversation. The people left behind do.

Netts Energy Charge Bot — for anyone managing a TRON-based estate whose final settlement will include USDT movements — or just an executor dealing with distributions over several wallet addresses, it is a little tool worth knowing about beforehand. It operates within Telegram, enables the user to seamlessly purchase Energy on-demand through linking wallet addresses via the Dapp, pre-funding a TRX deposit, and clicking Charge before any USDT transfer. The bot takes payment only for the Energy actually used — if a transfer does not use the rented resources, nothing is spent — and each one hour rental is sufficient for one transfer. Cost can be from $1 to $2 for transfers to wallets that already contain USDT, also from $2 to $3 for wallets with no USDT balance. Less money lost to a single transaction, multiplied across all the transfers an estate executor may have to do, will amount to real money saved over the default of burning TRX.