Most Drastic Miscalculations in Crypto History

3AC, Terra/UST, FTX, lenders, and The DAO — how strategic ego, leverage, and bad design vaporized billions and rewrote crypto risk culture.

The history of the cryptocurrency economy tends to be romanticized as a lawless frontier, where fortunes can be made and lost overnight and where risk-taking entrepreneurs upend existing financial system with cutting-edge technology. But that story is a partial truth, and below the surface there’s a dark parable about what technology really wants — an important lesson clouded by those high-profile disruptors that failed not miserably enough, but spectacularly.

These are not the growing pains of early adoption, or little foibles with a new technology: These are failures at a strategic level. Take, for example, the so-called tragedy of Laszlo Hanyecz, who in 2010 famously spent 10,000 bitcoin on two pizzas — often referred to as a common “mistake” in mainstream culture. This was, in fact, a pretty essential proof-of-concept for a fledgling currency that had no value to begin with. When Hanyecz sat down to eat the pizza on May 22, 2010, he most likely had no idea he was eating a multi-million dollar lunch and his taste buds were marking bitcoin history in more ways than one.

And yet… the real miscalculations — the ones that vaporized billions in value, and wiped out life savings — were made by sophisticated participants who had every tool at their disposal to measure risk, but elected to turn a blind eye. These were men and women who mistook leverage for genius and market momentum for the new rules, and they constructed edifices that could not withstand their own heft.

Illusion of a “Supercycle”: Three Arrows Capital

The crypto hedge fund 3AC, or Three Arrows Capital, was no fly-by-night operation; it was the premier one in cryptoland, managing billions of dollars and earning the respect of every major trading desk. Their tragic failure was based on a belief system they proselytized with religious zeal: the “Supercycle.” The founders deluded themselves that the crypto market had evolved beyond its violent booms and busts of old, instead entering into an era in which prices only went up, fueled by institutional adoption and mass acceptance.

It wasn't merely a marketing slogan; it was the operational underpinning for their fund. Expecting prices always to go up, or at the very least never crash in a major way, they loaded up on enormous leverage that would give them as much exposure as possible to this perpetually rising bull market.

The strategic mistake was not just being bullish, it was building a multi-billion dollar portfolio under the assumption that a "black swan" (worst possible case) event could never occur. As the market turned in 2022, 3AC wasn’t just exposed; it was levered long on assets that were quickly going illiquid. Their particular trade with the Grayscale Bitcoin Trust (GBTC) is a textbook case of a dead end strategy. For years, GBTC has traded at a premium to the underlying Bitcoin, enabling funds to arbitrage that difference. 3AC gambled that this premium would remain or at least be positive. When their position turned into a massive liability was when the premium flipped to a discount.

They were stuck in a trade that was losing money, and yet the Supercycle thesis blinded them to the fact that they needed to take losses. Instead, they doubled down and borrowed from just about every big lender in the space to service those loans — effectively turning a hedge fund into a house of cards. It wasn’t just that the fund went bust; it triggered a contagion that destroyed lenders like Voyager Digital and Genesis, illustrating how the strategic blindness of one firm can show up as a blind spot for an entire industry in a hyperconnected marketplace. The failure of 3AC illustrated that no matter how successful you have been in the past, you are never above simple principles of risk management.

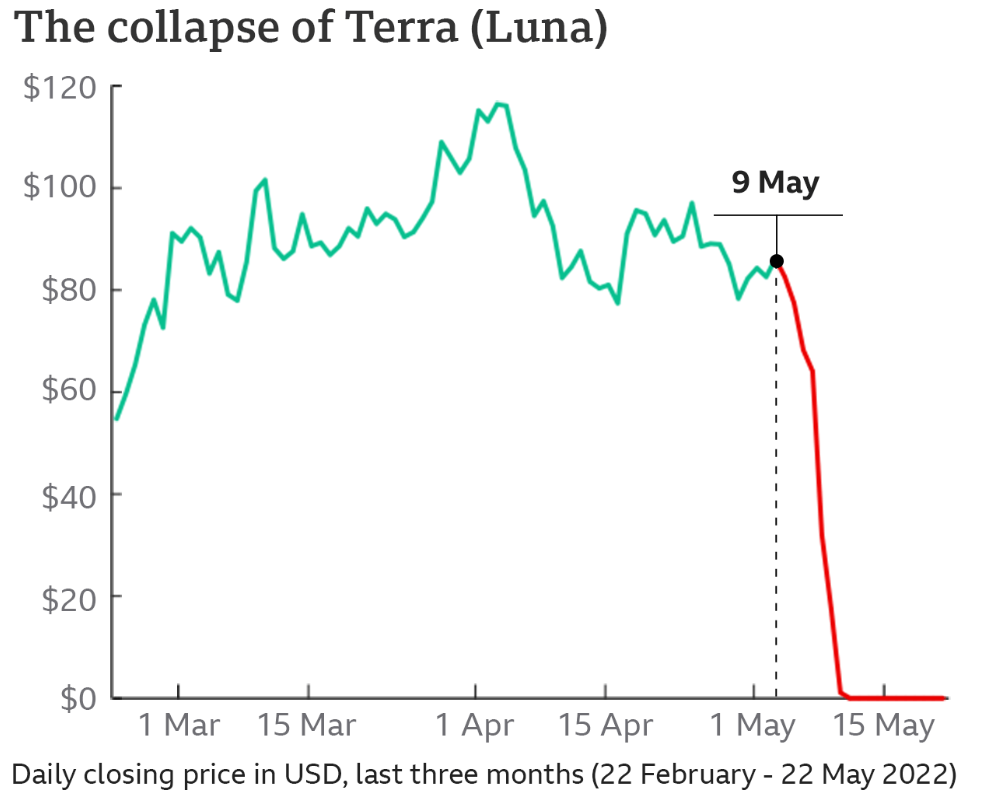

Algorithmic Hubris: The Terra-Luna Collapse

If 3AC was a risk management failure, the Terra ecosystem mega-crash and its stablecoin UST was a mechanism design blow-up & hubris. Do Kwon, the founder of Terraform Labs, had imagined a decentralized stablecoin that wasn’t backed by traditional collateral like the US dollar. What went wrong tactically was the assumption that an algorithmic peg would survive a long, coordinated attack or a true crisis of confidence without external support. Kwon’s play hinged on the arbitrage dynamics of the LUNA token and UST. As soon as UST dropped under $1, traders would burn UST to mint LUNA and “refeed” the peg. This was fine in a bull market but introduced a “death spiral” risk during panic.

The real strategic failure, however, came months before the final crash. Realizing that the peg was very fragile, Kwon created the Luna Foundation Guard (LFG) and commenced a movement acquiring billions of dollars worth of Bitcoin as a reserve. On paper, this seemed prudent. It was, in fact, a fatal strategic mistake. By tying the health of UST to the price of Bitcoin, Kwon eliminated the one benefit an algorithmic stablecoin could potentially offer — uncorrelated stability. The peg broke, and LFG had to sell billions of dollars worth of Bitcoin into a panicked market to maintain the price. This sell pressure forced the price of Bitcoin down, whose decline dragged the whole market - including LUNA - lower, undermining confidence into LUNA even more.

It was a self-fulfilling prophecy of doom. So the system of using volatile coins to back stablecoins in order to attract users and meanwhile promising 20% fixed yields via all sorts of Anchor Protocols (featuring every imaginable letter) was bound to implode as soon as growth slowed. The fallout was massive: the destruction of $40 billion in value over a matter of days, along with a regulatory crackdown that set the industry back years and ruined retail investors who were promised UST was “safe.”

House of Cards: FTX's Liquidity Flash Crash

And then there was the strategic overreach that passed for innovation: FTX. As fascinating as the criminal fraud of commingling client assets with Alameda Research is, the business error that they clearly based everything on is just as splendid. Sam Bankman-Fried built a fortune on the idea of “cross-margining” and high-speed trading, marketing himself as the “JP Morgan of crypto.” But his tragic flaw was making his own exchange token, FTT, central to his financial viability. FTX and Alameda had treated FTT as though it were just as liquid and stable as the US dollar. They borrowed billions against it, certain that they could either always control its price or find buyers if necessary to liquidate. This created a dangerous feedback loop where the health of the exchange was solely dependent on the faith in a token that the exchange itself had printed.

This is the textbook mistake of confusing “mark-to-market” with “realizable” value. Alameda had billions of dollars on paper in FTT. If they actually dumped even a fraction of that on the market, the price would crash to nearly zero. Bankman-Fried’s plan was to convert this imagined equity into actual assets — Robinhood shares, venture investments, political sway and real estate. Essentially, he was buying the world with a currency that he had manufactured himself, and believing that the music would never stop. He also misjudged the social dynamics of his industry, thinking that his carefully crafted image of “Effective Altruism” would protect him from public censure.

When the chief executive of Binance, Changpeng Zhao, said last month that he’d sell some of his FTT all at once if it could somehow be traded, it laid bare how strategically fragile the whole FTX edifice is. There was no actual liquidity, just the appearance of it. The aftermath of this all was a total loss of confidence in centralized exchanges, and the industry went through an agonizing process to make up for it with proof-of-reserves and stricter audits. And the FTX fall was more than just a bankruptcy; it was a betrayal that would reset the public perception of cryptocurrency for a generation.

Digging deeper into history we can examine the strategic blunder (or general inattentiveness) made by Mt. Gox, at one time the largest Bitcoin exchange on earth. It was largely run like a software project rather than a financial business, Mark Karpelès said as he assumed control of the exchange. There was perhaps a miscalculation here about the prioritization of things. Goals in the early days of 2013 and 2014 were “growth at all costs.” Secondary to keeping the site live and supporting all of the new players were security measures, account reconciliation and cold wallet policy. Karpelès was not able to appreciate that as the custodian of hundreds of thousands of Bitcoin, his product wasn’t the trading engine: it was security. He focused on features and maintenance, not the foundational security architecture necessary to safeguard user funds.

For years before the collapse, hackers were siphoning money out of the exchange without anyone noticing, partly because the internal accounting systems were so scant as to be nearly nonexistent. The decision — strategic and eventually fatal — was to run a skeleton crew on the technical side while dealing with volumes that matched those at traditional banks. When Mt. Gox finally collapsed, 850,000 Bitcoin was lost in the wind. The result was a “crypto winter” that lasted years, as the market came to terms with the fact that the infrastructure supporting this new technology was horribly fragile. It handed the industry a painful lesson: it doesn’t matter how early you rush to market if you can’t protect the assets you have. The Mt. Gox debacle was a warning about the perils of putting scaling ahead of security — a lesson ample numbers of exchanges have failed to take heed of since it happened, with predictable results.

Yield Trap: Celsius and BlockFi

The world of financial services is always a favorite target for scams, but nothing might be more fitting of the current hype/lust/mania than cryptocurrency lending platforms like Celsius and BlockFi.

Another species of strategic failure was characteristic of the saga of BlockFi and Celsius. At the heart of these companies is an attempt to close the gulf between DeFi (Decentralized Finance) and traditional banking. Their pitch was straightforward: put crypto in, and get high interest rates out. The tactical error was the duration mismatch and under-pricing of risk. To pay depositors 5% or 10% yields, these companies had to earn even greater returns. They did this by providing loans to institutional borrowers like 3AC or participating in risky DeFi tactics. Known for his “Banks are not your friend” t-shirts, Alex Mashinsky of Celsius positioned his company as a more ethical and safer alternative.

The mistake was in treating these loans as safe, low-risk activities. When markets tightened, their borrowers could not pay back loans and the illiquidity of the investments left them unable to process customer withdrawals. They had lent as if they were a hedge fund but advertised like a savings account. This strategic dissonance was unsustainable. They missed the correlation risk of the crypto market — when one borrower goes bust, they all want to go bust. The failure of these lenders demonstrated the perils of “rehypothecation,” in which the same collateral is pledged multiple times across the ecosystem, creating a chain of liabilities that snaps when liquidity disappears. It resulted in the wholesale collapse of hundreds of thousands of creditors leaving them with pennies on the dollar and also shattered any illusions that “yield” in crypto could ever be risk-free.

Even well-intentioned efforts like “The DAO” in 2016 fell victim to a strategic blind spot: The idea that the principle of “code is law” could supersede human intention and safety. The DAO was invented by a group of people who created a new form of decentralized venture capital fund, containing an enormous volume of Ether. Their goal: to build an unstoppable, self-sustaining organization. But they underestimated the difficulty of writing bug-free code for a pioneering application. And when a hacker took advantage of a recursive call bug to siphon off the money, the community had a philosophical crisis. The theory of immutability butted up against the fact of theft. The fallout — the hard fork of Ethereum — demonstrated that social consensus was still paramount to code, a realisation that has split the community ever since.

The industry, in the aftermath of such disasters, has had to grow up. The Silicon Valley mantra “move fast and break things” turned out to be a disaster when applied to people’s life savings. We’ve seen the pendulum swing towards newer, more conservative strategies that involve divorcing custody from trading and fundamentally auditing reserves. The survivors are the ones who had settled for risk management, instead of maximum yield. The regulatory environment in 2026 is a far cry from that of the wild west of 2020, with comprehensive rules around asset segregation and capital reserves now the rule rather than the exception.

But even in this new normal, efficiency is a battlefield. Resource is one of the constantly faced problems among companies and heavy users on blockchain networks (such as the TRON network). Every transaction takes resources, and this becomes a lot when you are running hundreds of transactions. Here is where the theory of resource management shifts from tactical good idea to strategic definer.

Convenience and Performance – the Way Forward

In 2026, we are no longer in the business of speculative growth and investors have swung towards operational optimization. This time, companies aren’t merely looking to pump tokens; they are aspiring to run sustainable businesses with healthy margins. So what about the ins and outs of everyday, like renting Energy to transact across and not burn through loads of fees? It is the capacity of efficient control over these costs, which becomes a micro-strategy that distinguishes successful operations from loss-making ventures.

The renting of energy is a common practice for efficient dapps on the TRON network. If businesses chose to rent Energy instead of paying TRX each time a transfer was made, it would drastically cut down on the monthly cost. It’s a modest but much-needed correction from past abuses — an acknowledgment that resources are finite and must be husbanded carefully. The next cycle's survivors will be those who make the most out of every component of their business, from their balance sheet to their transaction costs.

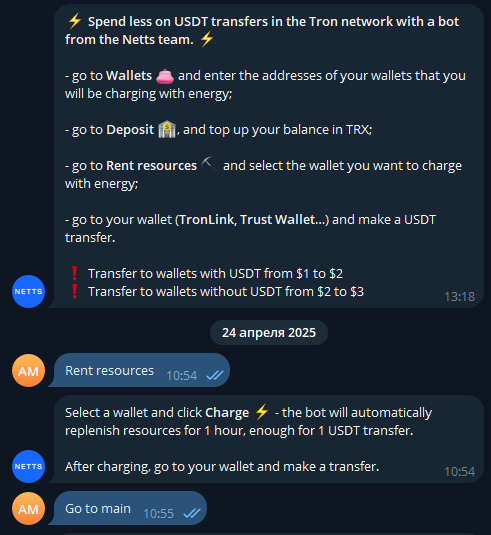

Within this landscape of optimal resource use, services like Netts Energy Charge Bot are now an indispensable companion for the contemporary crypto enthusiast. Such a bot will enable end-users to borrow resources for their Tron transactions effectively, avoiding overpayment on trivial transfers. Users can also choose a wallet, deposit their balance in TRX and click to charge that automatically refills resources for one hour — long enough for a USDT transfer. When a transfer goes through, the bot gets the exact amount of resources spent and subtracts it off from your deposit - if you don't spend any resources there won't be any deduction. It'll reduce the cost of transfers as it offers standard rates for wallets with USDT and without, in line with the efficiency and precision that characterizes today’s market maturity.