Cryptocurrency and Household: Does It Pay the Bills?

Paying household bills with crypto in practice — volatility, fees, cards, stablecoins, and where “crypto-native” finance still hits real-world limits.

There’s nothing like the sinking-in-the-pit-of-your-stomach moment when new monthly bills arrive. Nor is it simply a financial burden — significant enough in an era of fluctuating economies and escalating costs. It's something much more insidious — a kind of psychological burden that weighs down on the responsible citizen. If you sit down to “pay” your utilities, mortgage or insurance payment, you are not paying for anything. Here you are at a ceremony of total exposure. The government and the banks aren’t just watching the money, they’re watching you. They are tracking every single penny that you make and keep from feeding into the daunting, insatiable maw of the system. It seems more like an inspection and less like a transaction, a monthly audit of your existence in which you’re guilty until proven innocent.

Just imagine the mountains of data that come along with each and every payment. Not one fingernail clipping of privacy remains in this entire process. In fact, in order to keep the lights on or the water running, you are required to include your full name, your current address and often your phone number — and sometimes even social security number — with the transfer. This information is compiled, saved and studied. It builds a comprehensive profile of your life, your daily habits and where you are.

And it’s not just the government that is watching. It is the credit bureaus, the marketing agencies and the data brokers that feast on this information. Your financial hygiene is rated, ranked and sold to the highest bidder. Did you lapse just one day on your payment? That is recorded. Did you repay a loan too quickly? Ironically, that could harm your score because you are less profitable to lenders. The system is there to keep you predictable, tethered and transparent - while those observing it remain opaque and unaccountable.

You are monitored and logged systematically and routinely on a motion by motion basis each month, and society makes you feel helpless to prevent it — it's the price of living in the new world. The transparency is lopsided: you get a faceless institution demanding money from you (you have, basically, sent money to their phone; if they wanted to know whose account it came from they could find out that very moment), whereas they learn every little thing about you all the way down to the device that transmitted your payment. It’s a glass house, and the walls are built of your financial need. It doesn’t help to have a banking system that is “too big.” Transfers can take days. Errors are difficult to rectify. Rates are buried in fine print.

But you know, because these are “bills” — the grown-up stuff of life — we’re supposed to be thankful for the opportunity to navigate this bureaucratic labyrinth. Yet we are told that this torpid, intrusive surveillance state is the maximum safeguard of our security and order. But all one needs to do is cast a glance at the lunatic fringe of our financial world to see that this is a lie. There are areas of money where it moves at the speed of thought, where privacy is assumed and respected, and where the user is served with a level of respect and efficiency that no retail bank can hope to reach.

Paradox of Forbidden Efficiency

It’s deeply ironic that the most effective, user-friendly and private financial experiences are often found in industries we as a society tell each other to stay away from. Take the world of online sports betting or gambling through cryptocurrency casinos. These are terrain that moralists and regulators have long regarded with suspicion — dens of vice and danger. And still, if you consider only the mechanics of the deal, it’s night and day. In the world of crypto gambling, whenever you are ready for money to be gone from your wallet — poof! Then it gets there all at once. There are no waiting periods, no obnoxious questions about the origin of funds, let alone your grandmother’s maiden name.

In the "shadow world" you are a total noname to the sender. Your whereabouts or employment record need not be disclosed to the recipient. All they should have to believe is that the cryptographically proved funds actually exist. You’re not even worth spying on. All of a sudden, the "like" button would be screaming to its users that clicking it is an authentic token of cold scientific value, unadorned by the snooping that burdens the “real” economy. Why is the most important stuff, like being able to pay for heat, and electricity and shelter get watched with an eagle eye but something that’s frivolous or bad for you like online gambling literally gets 100x better service than the government provides when they’re going to steal your money from you?

Moreover, consider the operational hours. Bankers keep “banker’s hours” — a thought that even sounds old-fashioned in the digital era. Attempt to pay a bill on Friday evening, and it may not clear until Tuesday. But the "vice" trades never slumber. Crypto game sites and gambling services are open 24 hours a day, seven days a week, every day of the year. They do not observe holidays. They don’t get weekends. Their computer systems (which are frequently built on smart contracts) run according to a set of algorithms, which get the job done 24/7, whether it’s Christmas morning or just another random Tuesday at 3:00 A.M.

This kind of constant reliability is diametrically opposed to traditional finance "system maintenance" downtimes and random pauses. Everything seems to work pretty perfectly in these crypto-native spaces. Support is often 24/7. Interfaces are sleek and intuitive. The friction is non-existent. It is a salient and uncomfortable question: if a casino can handle a million dollars in seconds without someone finding out your blood type, how come paying a hundred dollar electric bill takes up to three days to clear and an address book’s worth of information? A similar level of household finance could be just as quick and private with technology that already exists. The bottleneck is not technological; it is architectural. The incumbents want control and visibility of the population’s resources; that is a conscious decision on their part.

Path to Sovereign Living

The good news is that the winds of change are beginning to blow that promise a new financial paradigm. Change is in the air, with forward-looking jurisdictions around the world starting to understand that what has been wrong can no longer be right. We are witnessing notable regulation progress signaling acceptance and practicality of cryptocurrencies not merely as speculative assets, but as real medium of exchange in day-to-day life. The narrative is changing from “banning” to “integrating,” and this has begun to unlock a whole new realm of opportunities for families to regain control over their financial privacy.

A few countries are well along in the way of paying their bills without issue using crypto. The future is already here, in places like El Salvador, Lugano in Switzerland and various progressive towns and cities across Latin America and Europe. Residents can walk into a store, scan a QR code and pay for groceries as easily as they might send a text. And, most significantly, it can be used to pay municipal taxes and utilities in digital currency. What people already enjoy in those countries is just the tip of what’s possible. Picture paying your property tax in seconds, by phone, without a bank teller or one scrap of paper. The transaction is on the blockchain — immutable and transparent in its activity, but private for the people involved.

This adoption is not just a flight of fancy for the tech literate, but lifeblood for those who are unbanked. Billions of people across the world are shut out from the conventional financial system due to not possessing the right paperwork, or living in “high-risk” jurisdictions. For them, settling a bill often means risky trips — fraught with cash — or usurious remittance fees. Crypto bypasses these barriers entirely. It enables a freelancer in the developing world to get paid and pay their Internet bill directly — with no intermediary that takes a 10%-per-transaction cut. This is democracy in the most basic terms we know: household economics. It turns the millions of smartphones in the country into their own bank.

This convenience is powered by state of the art technology running in the background which helps to reduce the expenses. On chains like TRON, for instance, efficiency is achieved through features such as fee-less or very low cost transactions.

To optimize the management of such transactions, the developers and service providers use tools such as a tron energy renting API which are to manage efficiently these network resources. By enabling the automation of Energy renting, these platforms eliminate technical intricacies and provide a seamless experience for the user at very low prices. This is the new economy’s “plumbing,” and it’s getting to be strong enough to serve millions of households — fast.

Crypto adoption is a feedback loop not a linear one. The greater the number of utility companies that accept crypto — as well as those other ones that use third-party processors — the more the friction of living on a fiat standard becomes apparent. They’re realizing that they don’t have to tolerate the surveillance and slowness. And they can opt for a system that wishes them well, with their time and with their privacy. Technology is scaling to meet this, with Layer 2s and parachains offering faster transaction speeds than Visa or Mastercard at literally 1% of the price.

Old World Hookworms

But just as in any revolution, there are counter-revolutionaries and the path toward monetary sovereignty is no different. We have to talk about enemies of progress. There’s a whole ecosystem of parasites attached to those traditional revenue sources, and they won’t let go without a fight. These institutions feed off the complexity and opacity of an existing system. They profit from the friction. Every delay, every blank to fill in, every single verification step is something that can be used by someone there, somewhere down the line either to charge a fee or prove they are doing their jobs.

In the USA this is especially alarming. There’s even a company that lobbies politicians NOT to so easily get this tax income documentation because they are getting their hands on the money! How dirty is that? Government has the information already they could send a premade bill to the person. But the companies that sell tax preparation software spend millions of dollars to make sure the process is complicated, confusing and stressful. They create the problem so they can sell you the solution. It's the same logic that prevails in the banking industry. Banks want their percentage too. They push for rules that make it hard for crypto competitors to enter the market. They have closed the accounts of customers who do business with crypto exchanges. They then rely on the laundering mechanics of “consumer protection” to shield their monopolies.

The creaky SWIFT network that supports worldwide banking, for example. It is a 1970s messaging system that is slow, prone to error and expensive. Send a bill payment abroad — perhaps to help family members in another country, for example — and the money will be directed through several correspondent banks, each extracting a fee. It is a game of telephone with money as the call and, by the time we pick up, it has been so rubbed down that it’s impossible even to read who wanted what. All that whole infrastructure is pre-Crypto. It's a direct communication link between the payer and payee, destroying that parasitic chain of middle men.

These leeches are deeply entrenched. They have the ears of legislators and enough money to back campaigns. They weave tales about money laundering and terrorism finance to threaten the public away from peer-to-peer finance, taking advantage of the reassuring fiction that most dirty business is done with cash or good old-fashioned bank accounts. If crypto is going to take on all those leeches, it has an awful lot of problems. It’s really an asymmetric battle, one side a loose movement of open-source developers and another a horde holed up in fortress of institutions. The banks have the laws, but crypto has the code.

Underdog’s Inevitable Rise

That will be a hard fight to win, but there is every reason to be very optimistic. All we need do is look back a short 15 years to see how far we have come. Don't forget — when bitcoin was just born, people still laughed at whether you can buy SOMETHING with it in principle! It was “magic internet money,” a toy for geeks and libertarians. Critics derided it as a Ponzi scheme, a bubble, a joke. They said that it was not backed by anything of value. They told us governments would shut it down. They said it couldn't scale.

Skeptics wouldn’t be laughing then. Today, crypto is a trillion dollar asset class. It sits on the balance sheets of publicly traded companies. It is the medium of exchange for sovereign countries. It is debated in the halls of congress and parliament. The very institutions that used to deride it are now rushing to offer their own ETFs and custody services. The durability of this technology is a fact. It seems to have flourished despite crashes, bans, hacks and scandals and each time it has come out more resilient, more decentralized and more impossible to kill.

It’s also unclear who is going to prevail in the end — and it is often the underdog. And the implication is that there are unavoidable forces attracting efficiency and freedom from cryptocurrency. At the end of the day, people tend to gravitate towards what works better. But if a family can pocket transaction fees, safeguard their privacy, and pay bills instantly without choking on bureaucratic acrimony, that’s what they will do. The “parasites” might slow it down, but they cannot stop it. The genie cannot be put back in the bottle. The code is open. The network is running. And as the infrastructure continues to grow up, that possibility to essentially live entirely outside of the surveillance grid of traditional finance is an actuality for more and more people.

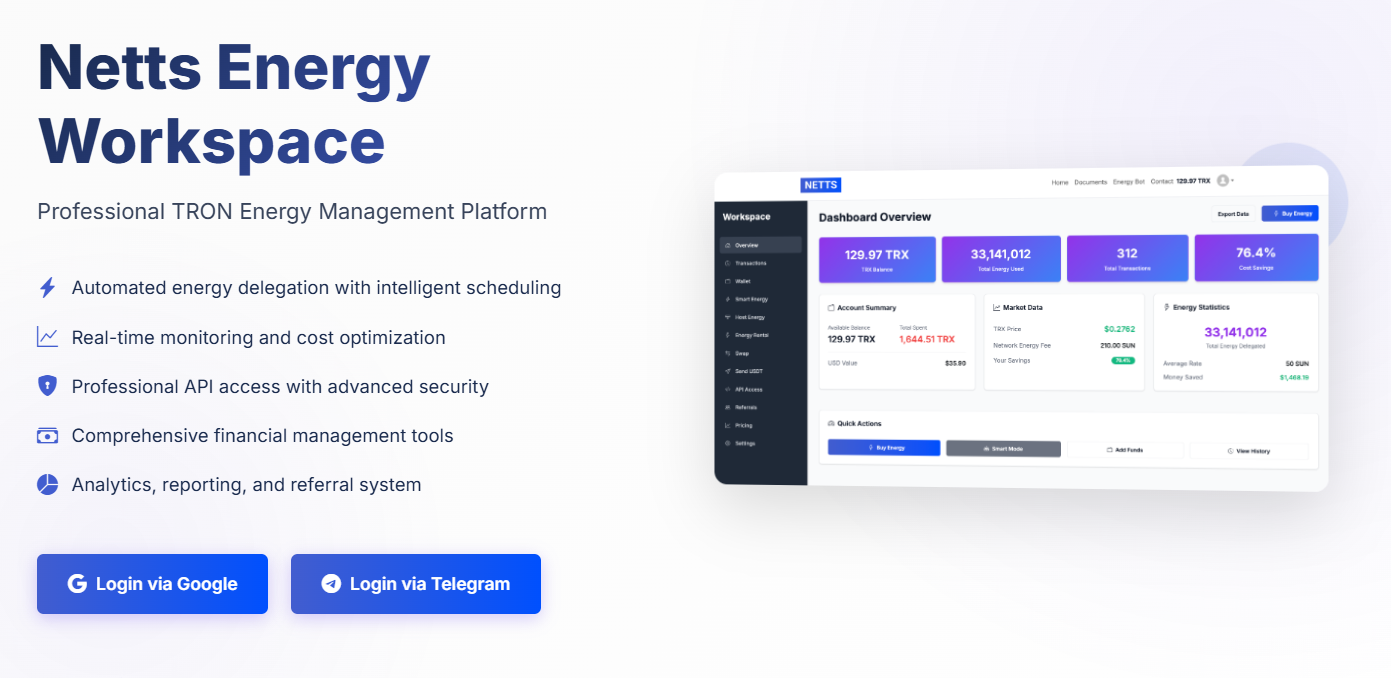

In order for a user to navigate this unfamiliar landscape effectively, they need services that bring together the intricacies of blockchain mechanics with everyday practicality. That’s where platforms like Netts Workspace step in. It is designed to be professional command tools for managing the TRON blockchain operations and offers such features as an automatic energy delegation so that users could greatly save on transaction fees which can be cut by up to 80% versus burning TRX.

Offering a treasury of features such as the TRON Energy renting API, real-time alert system and smart scheduling mechanism, Netts gives users the opportunity to manage their resources effectively. With their 'Smart Mode' to delegate automatically based on balance triggers, and their 'Host Mode', which allows keeping a constant in/out power supply of masternodes. It’s the sort of user-centered innovation that is turning crypto-household fantasies into practical realities, illuminating a future where covering bills isn’t a weight on your shoulders, but something as straightforward and private and efficient as pushing a button.