Crypto Car Salesmanship: Lies That Damage the Community

Rug pulls and influencer shills mirror old sales tricks — why crypto scams spread fast, how accountability is returning, and how communities rebuild trust.

It begins with a whisper, then a hum, and finally a roar. A new token pops up on the decentralized exchanges, this one set to revolutionize gaming and finance — or so they say. Influencers with millions of followers post enigmatic rocket emojis and advise their followers that this is the “next 100x gem.” The Discord server is buzzing, with fervent acolytes trading memes and dreams of riches. The hype is not lost on John, a retail investor with a nine-to-five job. He’s been dipping into crypto, looking to get ahead on his mortgage.

He logs in and instantly finds himself at home on the server. There’s a messianic quality to the enthusiasm; everyone, one gets the sense, is in it together and part of something that the arrogant and decadent mainstream world just doesn’t get yet. That camaraderie, that sensation of playing for a winning team, persuades him to let his guard down. He reads the project’s ambitious roadmap, sees the slick marketing tactics, and tells himself this is his opportunity. He puts a few thousand dollars — a large amount for him. The token’s price soars. John feels like a genius for a few days. And now the chart has you seeing a lone vertical red line overnight. The price has crashed 99%. The developers’ wallets are empty. The Discord server is no more, the Twitter account gone. John’s shares are now worthless and he is hurt just as much by the betrayal as the financial impact.

This story has repeated itself again and again in the cryptocurrency world, sometimes with slight variations. The project creators had not hacked a protocol or cracked a cryptographic code. They simply lied. They hyped, they promised the impossible and then disappeared with the money — a “rug pull,” in the parlance of the industry. What they did was dishonest and ethically bankrupt, but frequently it fits into a maddening legal gray area.

We are not talking about clear-cut crimes — exchange hacks, ransomware attacks — that already have definitions and systems for criminal prosecution. We’re not talking about the occasional gamesmanship that is ignored because the laws do not yet adequately reflect advances in technology. Welcome to the world of crypto car salesmanship, an art that comes with a product that’s digital; a showroom nearly anywhere in the world; and lies delivered at light speed, but which can leave its victims financially and emotionally ravaged within that fintech time lag. The narrative of the whole space is that it’s a dangerous wild west, in which every stranger is a potential scammer and any project is a bomb waiting to go off.

Pattern of Deception

The practices of these online charlatans are as diverse as they are pernicious. Not all scams are blatant rug pulls: Some projects die a slow death as nameless developers cash out their team tokens over the course of months, releasing empty project updates to feign progress. There are non-fungible token (NFT) projects that offer up grand roadmaps that promise video game and metaverse experiences, only to leave them behind in the dust once a project sells out; with its founders delivering nothing more than a JPEG.

Another popular scam involves something called “wash trading,” which is a way for scammers to buy and resell an asset, such as a cryptocurrency or digital item, back and forth between their own wallets. This gives the impression of high trading volume and liquidity, deceiving investors that there is a strong demand for the asset. It’s the online equivalent of hiring a crowd to stand outside a new store, just so it looks popular. We have also witnessed innumerable influencers who are paid tens of thousands of dollars to shill a token but do so without telling their audience that they’re whale-dumping the same tokens down onto them unaware. This is not an indictment of the technology; it is an indictment of human ethics, empowered by a system that hides it easily and punishes accountability harshly.

This is not an issue that exists solely within the world of cryptocurrency. The ingrained dynamic — the relationship between sellers and desperate buyers, in which information is unevenly doled out and the more desperate party burns through defenses designed to protect it from itself — repeats itself in every high-stakes, information-asymmetry-ridden industry. Think about the stereotypical used car salesman — leaning against a dented, but polished-up sedan. “She runs like a dream!” he says, neglecting to mention the faint knock in her engine that morning or the altered maintenance report filed away in his desk. Technically he’s not lying about the car driving, but it's what he doesn’t mention that’s his deceit.

No, this guy, and others like him, create a shroud of mistrust that taints every honest dealership. The buyer comes on the lot bracing for a lie and we force those honest enough to be on the straight and narrow to prove two-fold that they are not lying. A handful tarnish the reputation of the multitude. We see it in real estate, where an agent might capture the right angles and use a smart bit of staging to obscure cracks in the foundation, selling a dream home that becomes an ordeal of repairs for the young family who buys it. We see it in the field of law with ambulance chasers who take advantage of innocent accident victims and corrupt the image of real lawyers fighting for justice.

The difference in crypto is the magnitude and velocity of the deceit. A dishonest car salesman can con only one person at a time. A crypto scammer can bilk thousands of people across dozens of countries at the same time — all from behind a keyboard hiding behind a cartoon avatar. With the absence of face-to-face interaction and the international, borderless nature of the market combined with the complexity of the tech itself all colluding to create an environment that is fertile for bad actors. The victims, typically with nowhere to go, have lost their funds into the maze of pseudonymous wallets.

Accountability Void

At the place it’s rotten happens, deep accountability is sorely lacking. In mature financial markets, regulators such as the U.S. Securities and Exchange Commission (SEC) have developed and refined rules to stop investors from being scammed or manipulated. There are very stringent rules as to disclosure, advertisement and reporting. If a company deceives its investors, the company’s executives can be hit with large fines and even prison time.

In a decentralized world like crypto, such a well-defined regulatory framework is still very much in its childhood. Scammers are operating in a sort of jurisdictional no-man’s land: They typically launch their projects from nations with few regulations and little oversight, aimed at a global audience. The effort to apply 20th-century securities law to 21st century digital assets has turned out to be a slow, clunky process for governments around the world. The notion of decentralization itself, as a term, is one that’s both powerful and tragic in that it’s frequently invoked — cynically — by scammers to describe their machines. They’ll say “it’s community owned” or that it is a “decentralized autonomous organization” (DAO) but they’ve got the keys to the treasury and could empty it out whenever they want.

This lack of accountability then leads to a "buyer beware" mentality, which may encourage individual responsibility, but is not an acceptable defense against clever and well-financed frauds. The idea that you have to become a forensic blockchain investigator in order not to be cheated is an unreasonable expectation of the average person.

Real projects are competing for precious attention and trust in a sea of scams. The signal from the genuine projects is often drowned out by the noise from the fraudulent ones. This fear and doubt slow adoption and as a byproduct, the people with capital don’t get to invest in the best projects that have an honest mission/use case, such as new TRON Energy marketplaces being created from grassroots adoption. A sustainable and efficient renting Energy market depends on user trust and each time a headline-grabbing scam gets the headlines, confidence starts to decline. When new users get burned by a memecoin scam, they are unlikely to stick around and explore the more complex but legitimate parts of the ecosystem.

A Ray of Hope: Bad Actors Being Held Accountable

But behind it all, something is starting to change. The notion that the crypto space is a total wild west carries lessons. We are also starting to see examples of bad actors actually being held accountable, indicating that this is a solvable problem.

Among the most significant cases has been that of OneCoin, a giant Ponzi scheme in disguise of a cryptocurrency that duped investors out of billions. Its founder, Ruja Ignatova, is famously out of sight (though not forgotten); but many co-conspirators and boosters have been arrested, tried and sent off to prison. The OneCoin case was prosecuted not as a cryptocurrency crime but rather as an elaborate, large-scale financial fraud — showing that when a crypto-adjacent scheme tips over into old-fashioned, clearly defined crime, the legal system can and will get involved.

Related to the “shady but not illegal” stuff, even more regulators target wannabe influencers over their involvement in aggressive pushes for crypto assets. In the past, the SEC has filed charges against a number of celebrities accused of not disclosing that they were being paid to promote specific crypto tokens. These enforcement actions are typically guided by the “Howey Test,” a well-established legal precedent used to judge whether something is a security.

In easier terms, when folks are pooling money into a common enterprise with hopes of profits from the efforts of others, it’s probably a security and is subject to SEC regulation. Applying this test to crypto assets, regulators appear determined to show that the old rules of finance still hold. Those cases, which result in significant fines, deliver a clear message: Marketing a security without disclosing it properly is illegal. This doesn’t prevent a project from being a terrible investment, but does help ensure that when people are advertising directly to consumers, people know what’s going on. That is an important first step, from a landscape of zero accountability to one in which there are rules of the road for marketing and promotion. These cases show that with directed effort from the regulators and the courts, the accountability vacuum can be bridged.

Building a Community on Trust

The ultimate answer won’t be found in completely removing regulators. The only way to have a truly robust and reliable crypto ecosystem is through home-grown libraries. The community is most qualified to marginalize bad actors and promote honest projects. This requires a multi-faceted approach.

First is a reinforced culture of self-regulation and self-policing. This is already happening via the community-led watchdog groups now emerging, on-chain sleuths and others who publicly trace and expose scammer wallets, as well as audit firms vetting smart contract code for holes. Establishing industry standards for transparency — like specific vesting schedules for team tokens or public multi-signature wallets for project funds — can be a way to sort the get-rich-quick schemers from the serious builders. As legitimate projects become more transparent when it comes to the other trenches, the worse shadowy ones will look by comparison.

The other, and maybe more important, answer is education. The response cannot be to just warn newcomers what not to do, but instead the community must educate newcomers regarding what to do. The worst enemy for the scammer is an educated investor.

There are many important red flags everyone can learn to recognize. The first one, the most blatant, is a conjured team. If the people behind a project won’t put their real names and reputations on it, you should wonder why. Another red flag is the guarantee of high, impossible returns. All investments are risky and any project that claims otherwise is likely a scam. And, last but not least, investors should be skeptical of any project that serves no purpose other than to generate publicity. A project that has a whitepaper, has a working product, and describes concisely what it will be doing is always better than the one whose value was solely driven by memes and influencer marketing. The community can grow a strong defence against deception by promoting critical thinking and due diligence. Trust is the cornerstone of any financial system, and for crypto to reach its full potential, it must be earned, protected and nurtured.

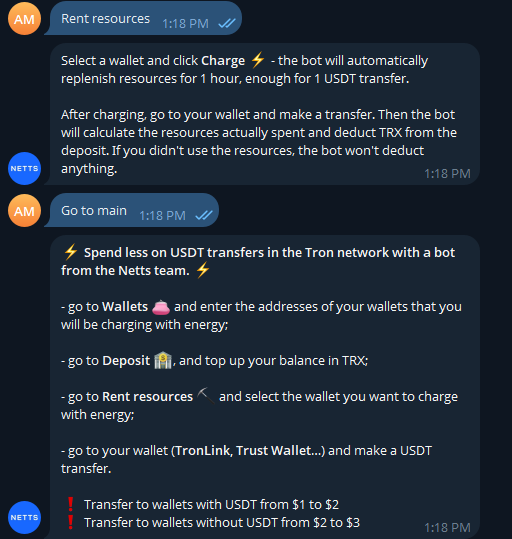

In a cluttered digital economy, discovering tools with simple, clear utility is crucial. If you are working within the confines of the TRON market, for example, simply managing transaction fees can be a major challenge. This is where services like the Netts Energy Charge Bot come in, providing a clear answer. Users can deposit TRX and the bot will easily fill up their wallets with Energy that is required to transfer USDT, thus minimizing the fees involved.