Crypto and Venture Capital: Who Bankrolls the Next Bitcoin

Venture capital in crypto: the billion-dollar bets, the spectacular collapses, and why narrative beats fundamentals almost every time.

There’s a tenacious myth in startup land that venture capital is there primarily to service failed entrepreneurs who outspended their ideas but not their ambitions. The version that gets told at cocktail parties goes like this: all you really need is to know a guy who knows a guy, say the right thing in front of the glass walls of a conference room and then walk out with a check big enough to finance three years of runway-burning. This legend became much more elaborate with crypto. Between 2020 and 2022, it felt as if anyone with a whitepaper and Discord server could get themselves a term sheet. And for a time, in the broadest possible sense, it nearly was.

The reality is quite different. Venture capitalists are not a bunch of bored billionaires in search of something to do with their money out of idle curiosity. They run funds that have real liabilities — to pension funds, university endowments, sovereign wealth vehicles and wealthy family offices that expect returns by a predetermined timeframe. A VC that keeps funding losers goes out of business. What appears to be reckless gambling from afar is, at its most sophisticated, a probabilistic arithmetic: back enough high-upside bets, grasp that the majority of them are going to fail and ensure the winners pay out enough to cover everything else plus some.

Crypto was one of the most hotly contested battlegrounds for that calculation. That asset class generated both the biggest VC hits and biggest VC misses in recent memory — often, within the same fund cycle. To understand why some crypto projects were able to raise hundreds of millions while others couldn’t even get a meeting, it helps to look beyond the mythology and ask the blunt question: what does a blockchain idea really need to be worth funding?

Pitch That Actually Works

First, a serious crypto project needs not a revolutionary idea. Ideas are cheap. In the end, what matters is a credible capture value mechanism and founder who can get a room full of skeptical investors to believe that mechanism will work at scale.

There was one thing genuinely new in the venture investing framework that cryptocurrency introduced, however: the token. Different from an equity of a traditional startup, a token can have utility in the protocol (e.g., gas fees), governance rights over a decentralized network or direct claim on the economics behind the platform. This offers a different type of upside for a VC. While an IPO or acquisition can take a number of years, these token-based investments can be liquid within months. That liquidity premium is part of why crypto pulled in institutional capital faster than traditional tech could often manage.

But liquidity cuts both ways. The very feature that had made tokens appealing to investors also made them appealing to fraudsters. A token that enables insiders to sell before the public catches on that a project is worthless is not an investment vehicle — it is a mechanism for extraction. Sophisticated investors understood this distinction. The firms that weathered the collapse of 2022 were mostly those that had done the tedious work of evaluating tokenomics: how tokens are allocated, what percentage of the supply insiders own, how vesting schedules work and whether incentive design actually aligns founders with long-term value versus a short-term price run up.

Andreessen Horowitz — known in the industry as a16z — also became the most prominent institutional player in crypto in part because they had built an entire dedicated team to evaluate these kinds of questions. Its first crypto fund was launched in 2018 with $300 million. By 2022, they had already raised a $4.5 billion fund — then the largest dedicated crypto venture fund ever put together. Their portfolio included Coinbase, which went public in April 2021 at an opening valuation of over $85 billion; Solana, whose ecosystem became one of the defining battlefields of the ensuing years; and Uniswap, which revolutionized how decentralized exchange mechanics operate. These were not lucky guesses. They are also the result of a framework: target protocols that exhibit strong network effects; credible founding teams, and token economics aligned enough to pass the bear market test.

There’s no value to a blockchain that nobody uses. It is worth fighting for one with ten million active wallets. The logic is similar to the way traditional VCs think about social platforms or marketplace businesses — the more participants, the more useful for each individual participant that network becomes. In crypto, this means metrics such as total value locked in DeFi protocols, daily active addresses, transaction volume and developer activity. This is where VCs who got the memo early paid attention; this was signal of real traction, not just capital-enabled promotion.

Evangelical Founder Problem

Here’s something the standard venture analysis framework glosses over, but is material: in crypto, the founder often is the product.

Michael Saylor did not create a token or develop a protocol. What he did was transform MicroStrategy, a business intelligence software provider, into the most aggressive institutional buyer of Bitcoin in history — and in doing so arguably impact the price of Bitcoin more durably than any mining company or exchange. MicroStrategy announced in August 2020 that it had bought 21,454 Bitcoin for $250 million. Saylor framed the purchase not as speculation but as a principled accountability of holding depreciating cash: the dollar was being debased, Bitcoin had a hard supply cap and any rational treasurer should make the obvious choice. The reasoning was not new. The scope over which he acted on it publicly was.

The framing was just as important as the trade. He became one of the most voluble crypto communicators of his time — tirelessly evangelistic, rendering the case for Bitcoin as self-evident logic. Other companies followed. His template was cited as asset managers launched ETF products. Corporate treasurers started following his playbook. By the middle of 2025, public companies held together almost a million bitcoin worth over a hundred billion dollars and MicroStrategy alone had held more than 629,000 — about three percent of all bitcoin in existence.

The lesson for investors was an uncomfortable but obvious one: narrative is capital. A founder able to articulate a vision with sufficient strength and consistency could move markets and attract institutional money in ways technical merit alone never would. In crypto, where so much of what’s being built is intangible infrastructure for systems that won’t exist at scale for years, if not decades to come, the founder’s ability to maintain belief through prolonged periods of uncertainty was often the only thing keeping a project afloat during stretches when outward progress could be measured in millimeters.

Justin Sun knew this at another register. Depending on whom you ask, the founder of the TRON network is either a marketing genius or a cautionary tale about promotional excess. The way Sun built TRON was through carefully chosen partnerships with celebrities, well-timed announcements and an intuition for generating headlines which kept the project in the conversation even when its underlying technology hadn’t done something impressive that week. TRX prices skyrocketed in less than a day by over one hundred percent when he pumped 30 million dollars into Donald Trump’s World Liberty Financial project at the end of 2024. The mechanics of how it happened precisely involves market dynamics and attention cycles, but the principle is straightforward: Sun had constructed a personal brand strong enough that his involvement in something was enough to move capital.

In 2023, the SEC accused Sun of securities violations and undisclosed paid promotions — allegations he denied. The case is an example of the power and the risk of this model: If the founder is the product, any threat to the founder turns into a threat to the investment. TRON holders were banking not merely on a blockchain but on Sun's ability to keep accessing markets. That’s a different kind of risk than backing a protocol with distributed governance and no single public name.

Greed Is the Engine, Not a Bug

There is an argument line — best heard inside policy discussions and in progressive media — that the venture capital funding of speculative crypto projects represents some sort of moral failure. The argument goes like this: here are folks with access to amazing piles of capital, and instead of investing it in housing or healthcare or climate adaptation, they’re giving money to the hundredth stablecoin or the new hot thing in Layer 2 rollups.

The answer is simple and unsentimental: They invest because they expect to make money. No one invested $900 million in FTX at an $18 billion valuation in July 2021 because they believed Sam Bankman-Fried was going to end poverty. Sequoia Capital invested in FTX on the belief that it was becoming the next unstoppable crypto exchange — steady revenue, a charismatic founder building bridges with regulators, a market position that seemed structurally not gettable. Sequoia had marked its entire $214 million stake down to zero when FTX imploded last November, after it was revealed customer funds were used for operational capital and to help fund the firm’s sister trading business, Alameda Research. SoftBank took something like a hundred million loss. Ontario Teachers’ Pension Plan — a fund for real Canadian schoolteachers — lost its spot, too.

This story isn’t really about VCs being reckless. It is about deliberate concealment. This investment thesis was rational based on information available — provided meticulously by a fraudster. Sequoia’s total fund was still in the black because losses were canceled out by profits elsewhere, and that is precisely how the math works when you construct a diversified portfolio of potentially explosive bets.

Terra/Luna told a similar story but with different mechanics. The algorithmic stablecoin project secured roughly $200 million from a cohort of backers including Binance Labs, Coinbase Ventures, Galaxy Digital, Pantera Capital and Polychain Capital. The project’s founder, Do Kwon, pitched himself with the kind of aggressive confidence that bull markets are known to reward. When the peg of UST broke back in May 2022, $45-55 billion in market value was lost over a single week. Investors who provided backing to Terraform Labs took losses commensurate with their exposure. Retail investors who had sunk savings into the ecosystem because a twenty percent annual yield sounded good didn’t have anything resembling that cushion. In December 2025, Do Kwon was sentenced to fifteen years for fraud. The supporters of the protocol then headed to their next investments.

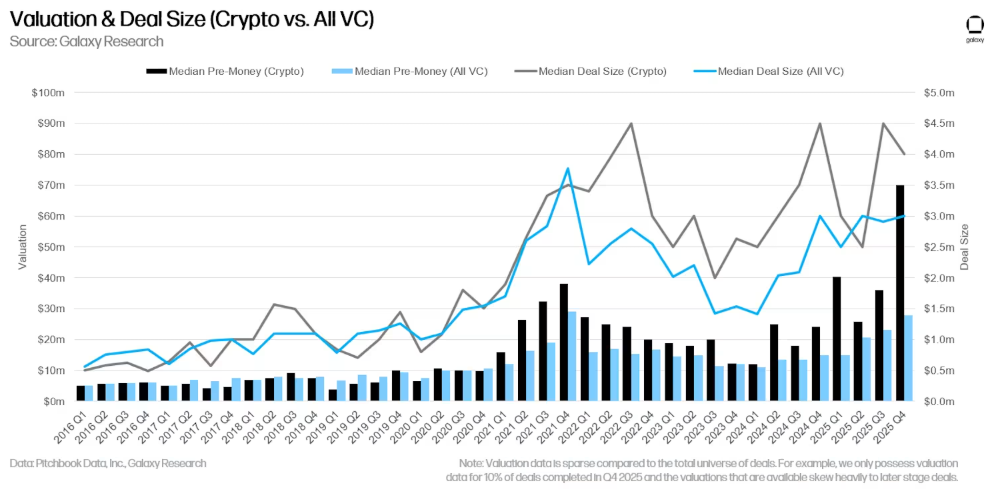

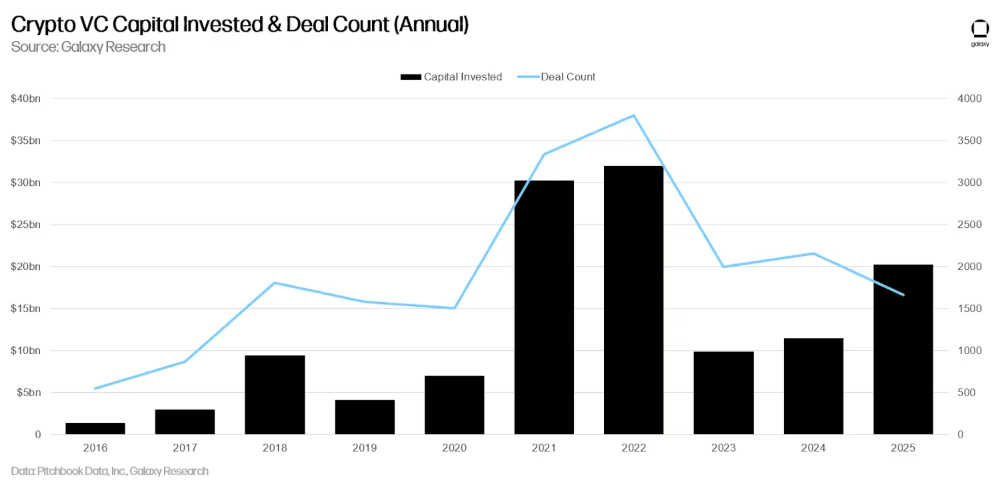

By most measures, 2021 was the peak year for crypto venture capital — about $29 billion deployed, a 720 percent increase from the previous year. In 2022, that total climbed to $33 billion before the wave of failures started. Terra/Luna’s implosion this past May set off cascading failures of its own: Three Arrows Capital, a large crypto hedge fund known for masterful plays in derivatives trades, effectively went insolvent. Celsius Network — which raised nearly a billion dollars of venture capital — halted withdrawals in June and filed for bankruptcy in July. In November came BlockFi, which is backed by firms including Peter Thiel’s Valar Ventures, Tiger Global and Bain Capital Ventures. FTX went down the same month. By the end of 2022, roughly $2.2 trillion in market value had been wiped away from the crypto ecosystem.

Funding fell to $10.7 billion in 2023 — a sixty-eight percent decline. The survivors came out with tougher questions and tighter filters. The ones that did not survive had mostly gained projects on the basis of something they called price momentum, instead of any lasting assessment as to whether the underlying businesses could operate without a rising market.

Court of Public Opinion

It would be disingenuous to talk about crypto venture capital without acknowledging that there is a real hostility around it in big parts of the public. The frustration isn’t completely irrational. In 2021 and 2022, at the height of the funding cycle, billions flowed into blockchain projects whose utility was dubious while articles about housing shortages, insufficient social services and inadequate public infrastructure shared space in a news cycle with those headlines. The question — why are people throwing money at the fiftieth NFT marketplace instead of making something useful? — is one that even crypto champions find it hard to answer gracefully in public.

Senator Elizabeth Warren emerged as the leading political voice harnessing that frustration. Her rhetoric positioned crypto largely as wiring for criminals, money launderers and sanctioned states. The industry’s answer was to spend millions against her re-election — Ripple Labs, the Winklevoss brothers and others funded a super PAC that raised more than her opponent’s own campaign. Warren won anyway, but the tussle revealed something: crypto was now rich enough to defend its own political interests, which to its detractors proved precisely what they had been talking about.

The environmental argument was on a different track. The energy consumption of Bitcoin’s proof-of-work mechanism is commensurate with mid-sized nations, and this frame dominated most mainstream discussions of the technology for half a decade. The move to proof-of-stake eliminated some of that criticism, but not all of it. The counterargument — which goes that venture capital is not a vehicle for charity allocation, nor has it ever claimed to be one — is logical but tends not to play well in public. The asymmetry of who gets the upside and who bears the downside when a project goes boom or bust is not exclusive to crypto, it just made it disproportionately visible.

Where the Money Flows Now

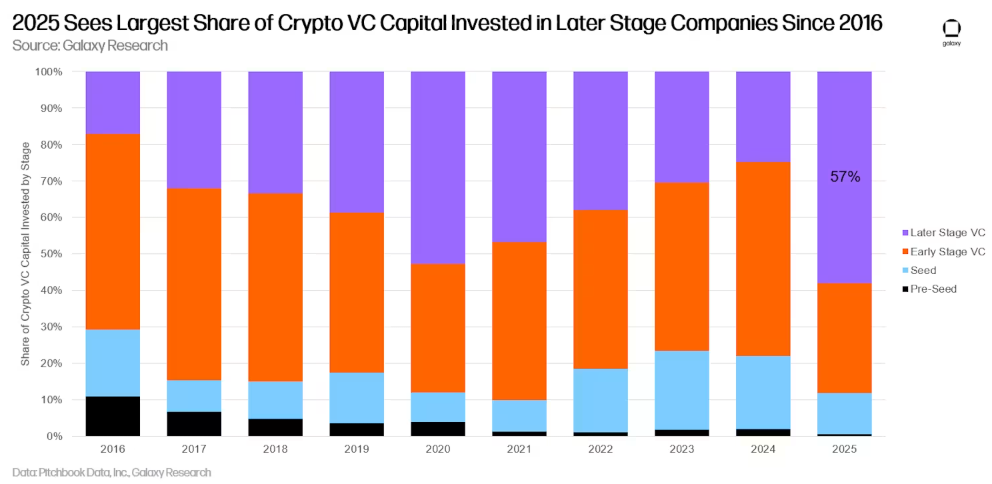

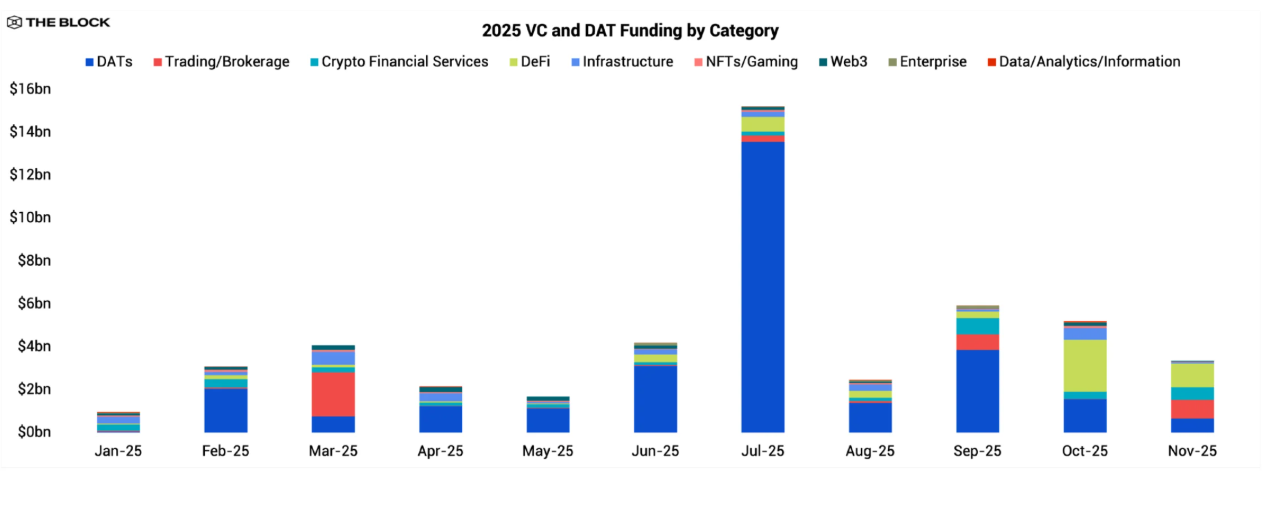

The 2025 crypto venture landscape is meaningfully different from the peak in ’21, despite the amount of total capital deployed getting closer to similar figures. VC investment in crypto more than doubled between 2024 and 2025 — the first time since 2022 that quarterly flows consistently topped eight billion dollars — but the make up of that capital changed radically.

The single fastest expanding category was the tokenization of real-world assets: bringing traditional financial instruments — bonds, real estate, private credit, money market funds — onto blockchain infrastructure. This pulled in over $2.5 billion just in 2025. Seemingly straightforward, tokenized real-world assets were far more legible to institutional investors who had been skeptical of crypto as just speculation. The references of these products were cash flows, credit ratings and legal structures that slotted into existing portfolio frameworks. BlackRock’s tokenized money market fund, opened on Ethereum and then extended to other chains, became the model dozens of would-be rivals try to copy.

The second major trend was the merging of artificial intelligence and blockchain infrastructure. Decentralized AI projects — networks where participants contribute computing resources in return for token rewards — raised more than half a billion dollars across the first half of 2025. The argument went something like that AI inference capacity is now monopolized by some cloud providers, and blockchain coordination could create more open markets for it. Whether that is the case remains the kind of bet that defines a generation of venture funds.

The companies that were able to survive the collapse in 2022 didn’t decide that crypto was a bad bet. They decided they needed better frameworks for assessing which bets in crypto were worth making. By 2025, Paradigm, which had $12.7 billion in assets under management, declared that it was branching out into AI, robotics and frontier technology. a16z was reportedly preparing for its fifth dedicated crypto fund at roughly $2 billion.

The screening questions that serious crypto VCs apply now as baseline filters seem almost obvious in hindsight:

1. Does the protocol have revenue that would remain profitable through a major token price crash?

2. What, specifically, is the realistic road to ten million active users — and who are those users?

3. Can the founding team weather a long regulatory investigation without the project falling apart?

4. Is the token distribution asymmetric and ponzi-like in that it rewards insiders at the expense of outsiders?

5. Can the project realistically be difficult to copy by a well-capitalized enemy that has access to the same technology?

These questions would have been unremarkable in any traditional software venture assessment at any time over the past two decades. The fact that they became the default filter in crypto — not the exception — tells us what industry learned from its failures. But not all firms learned at the same speed. The ones still running big funds in 2025 mostly did.

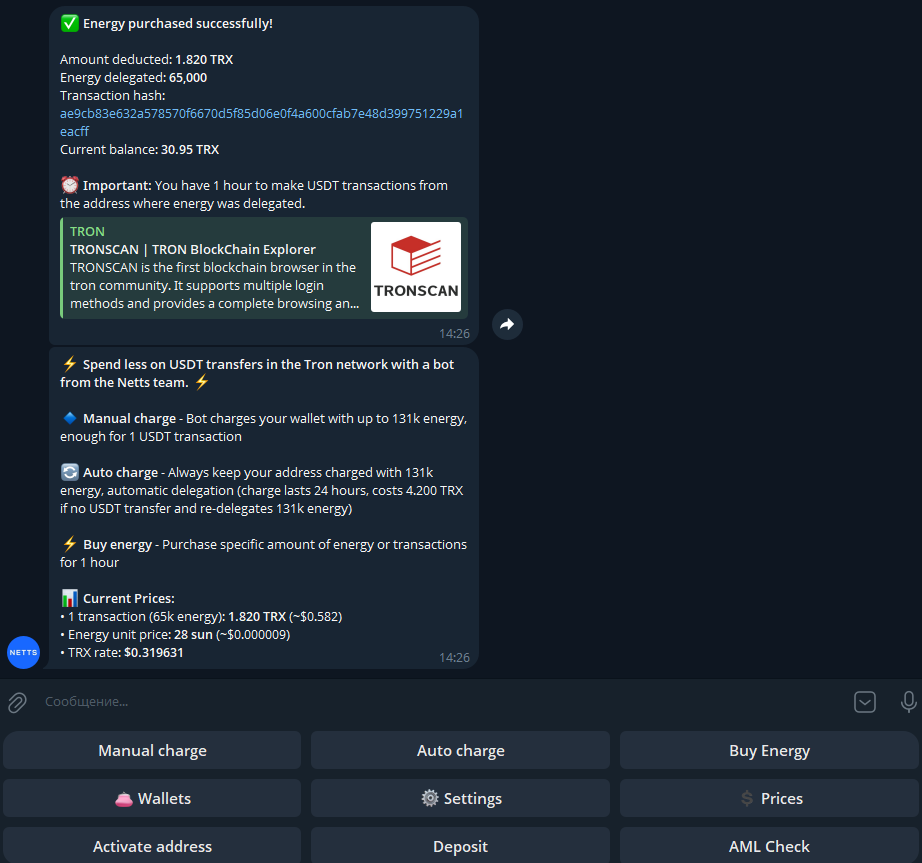

The more immediate challenge is simpler: bringing transaction costs down. That is exactly why the TRON Energy Telegram bots became a thing, and Netts Energy Charge Bot is among the most useful implementations so far. Users enter their wallet addresses, make a TRX deposit and there is an Energy supply (on demand) prior to each USDT transfer — with users only being charged for the actual consumption. For those with frequent transfer needs in Energy and without desire to stake TRX or 'waste' it via burn, Netts bot can be used for the task from Telegram; it supports standard TRON wallets like TronLink or Trust Wallet.