Crypto and Regulations: How Far Is Too Far?

KYC creep, code liability, and DeFi choke points — asking how much oversight ends innovation while users route around the slowest gates.

The history of cryptocurrency is a chronicle of war. It started as a whisper on the fringes of the internet, a brand new technology that broke through to the mainstream and laid bare society’s biggest problems after they seemed to be solved. Indeed, for well over a decade, the “code is law” ethos held sway that mathematics can supplant all-too-human governance, with all of its terrible failure and corruption.

But here we are in early 2026, and the terrain has irrevocably changed. The whispers are now a roar of legislative gavels and the scratch of bureaucratic pens. Our world today is no longer a land of the Wild West, it’s an age of the grand domestication of digital assets. The question that looms large over the industry, from the corridors of Brussels to the committee rooms of Washington, is no longer should we regulate crypto?, but have we gone too far?

In order to appreciate what’s going on today, it is necessary to compare that with the size of the regulatory frameworks that have been dumped upon ecosystem. These are not your ordinary speed bumps; they are gargantuan, sprawling constructs that will redefine at least how value flows through the internet. The intention is almost always expressed in terms of protection — protecting the investor, protecting the currency, protecting the state. But the execution often seems a form of containment, a means by which to declaw a tiger that the traditional financial industry fears it can no longer outrun.

The European Benchmark: MiCA

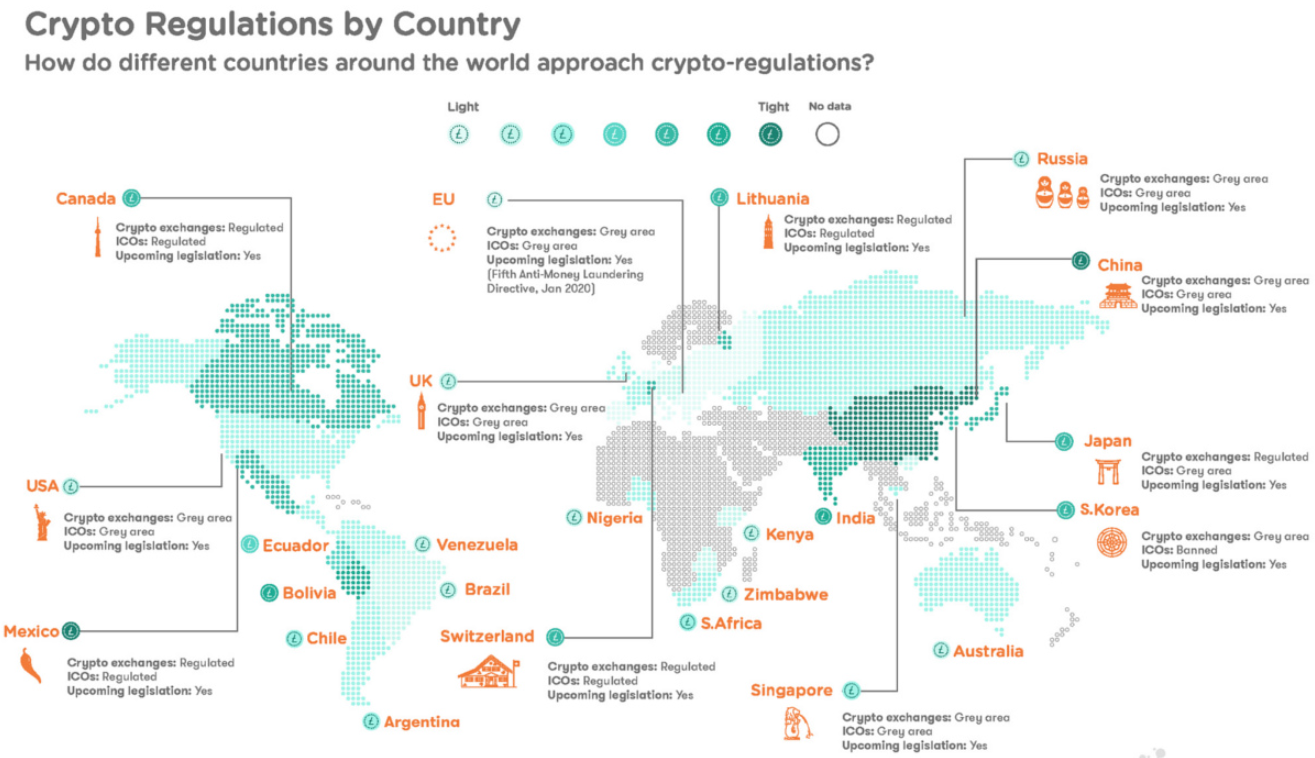

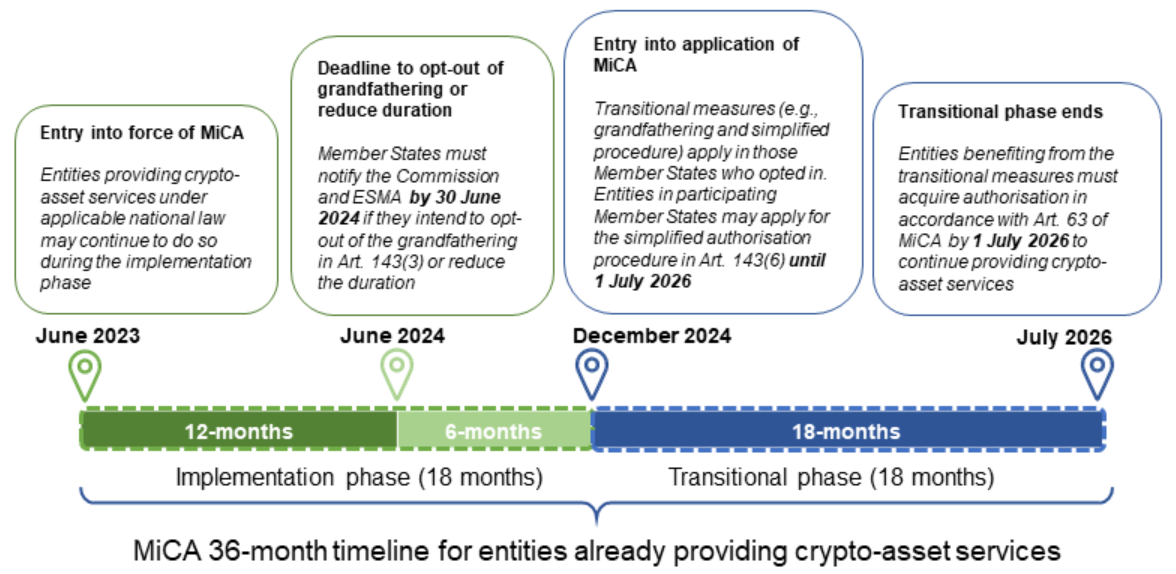

The first and arguably the most historic of these structures is the European Union’s Markets in Crypto-Assets regulation, or MiCA as it is more familiarly called. When it became fully operational, it was a game changer. Never before had a major economic bloc tried so hard to embrace the entire crypto sphere.

MiCA is an acronym for Markets in Cryptocurrency Assets: The backdrop to MiCA was the balkanisation of the European market. Before it was introduced, a crypto company would have had to wend its way through a labyrinth of twenty-seven different national rulebooks. France had its registry requirements, Germany had its licenses and smaller state of states had no direction at all. MiCA pledged to standardize this, building a “passporting” system in which a license from one country allowed access to all of the European Union. It was the selling point: The industry is growing up, crypto putting on its suit and tie.

Yet the disadvantages of MiCA have become increasingly obvious to those innovators on the ground. The biggest negative is the burden and expense of compliance. The framework has stringent capital requirements, custodial standards and reporting obligations that typically work for large incumbents but choke the life out of early-stage startups. We also have a strong “moat” effect in place, in which incumbent exchanges and banks are entrenched because they are the only ones with another expense to spend to figure out how to do what is legal.

Additionally, the constraints on stablecoins — in particular limitations on non-euro pegged tokens — however would wall off the European market from global circulation of value where USD denominated fiat pools dominate. This resulted in a friction point where liquidity was thinner in Europe and spreads wider than their Asian counterparts.

On the plus side, it can be said that MiCA rescued the industry’s reputation in the West. As an investor, it effectively eliminated the ‘fly-by-night’ risk during these early 2020s bull runs by providing clear liability rules for Crypto-Asset Service Providers (CASPs). Hedge funds and institutions, who had been reluctant to take on reputational risk, came off the sidelines. Pension funds and insurance monsters: They wanted legal certainty above anything, and MiCA delivered it by the truckload. It converted crypto in Europe from a casino to a regulated asset class.

It has been a tale of two MiCA reactions. The finance industry and big, centralized exchanges cheered it on, seeing it as a confirmation of their business and a deterrent for upstart competition. The “cypherpunk” faction of the community, on the other hand, saw it as a betrayal, an emasculation of the technology that robbed it of its revolutionary potential. The fallout is still settling, but the trend is clear: Europe has become a port in the storm for slow-moving, lumbering corporate crypto, while most of the high–risk, high-reward innovation has gone elsewhere.

The US Landscape: Regulation by Enforcement

Across the Atlantic, what is unfolding in the United States is an altogether different story. But rather than one clean, all-encompassing package of regulation like MiCA, the US languished in a kind of regulatory purgatory for years and operated via what the industry insiders dubbed “regulation by enforcement”. This method, spearheaded mainly by the Securities and Exchange Commission (the SEC), involved applying laws drafted in the 1930s to technology created in 2010s.

What was at stake here was a jurisdictional battle. What was a token — a security, a commodity or something altogether different? In the absence of a clear legislative directive from Congress, agencies filled in the void with litigation. This led to advocacy for bills such as the Financial Innovation and Technology for the 21st Century Act (FIT21) and its various iterations. These legislative efforts sought to establish clear lines of demarcation between the SEC and the CFTC (Commodity Futures Trading Commission).

The downside of the US approach has been disastrous for domestic innovation. The lack of clarity for so long led to a “brain drain.” On a global basis, there was widespread confusion about their legal obligations with developers trying to hide by moving to Dubai (Singapore or Hong Kong). The hostile approach to staking services and privacy tools drove a lot of new blockchains to geoblock Americans from the bleeding edge of decentralized finance.

The effort of everyday life looking over one’s shoulder for a Wells Notice resulted in a depletion of resources as that money could have been deployed to account towards product development versus paid out in legal defense funds. This has stymied progress in one of the world’s largest economies and created an atmosphere of fear rather than one of experimentation.

Colombia But still, one cannot overlook the pros. The aggressive stance of US regulators must, after the high-profile blow-ups of 2022 and 2023, undoubtedly have flushed some if not all of the most poisonous elements from under their rocks. While the strict custody and disclosure requirements were clunky, it was a way to force projects to be upfront about their tokenomics and insider allocations. For the average retail investor, the US market — albeit truncated — became one of most difficult locales in which to run a plain old Ponzi scheme without being burned.

The response in the US has been deeply divided along political lines, which is toxic for any technology. One camp says the crackdowns are necessary consumer protection, while another views it as the traditional banking lobby trying to snuff out a competitor. The result is a two-track global market: an “onshore” compliant market that much resembles traditional finance, and an “offshore” market where the original ethos of crypto persists, but often out of reach for American citizens.

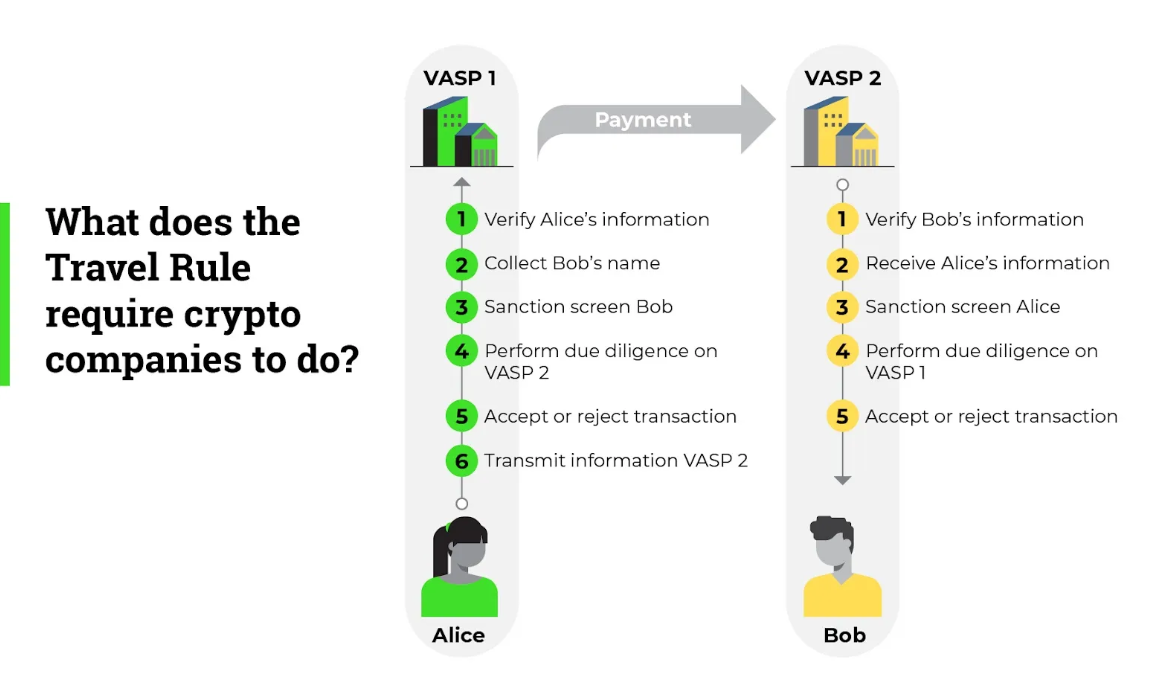

The Global Travel Rule

Once we are outside country specific borders, as in the case with the Global Travel Rule suggested by the Financial Action Task Force (FATF). This is probably the most far reaching and technically challenging of all.

The subject is the struggle against money laundering and terrorism financing. The conventional banking system has for years asked that when you send money from Bank A to Bank B, information tying the sender and the recipient must travel with it. And they were told to demand their Virtual Asset Service Providers (VASPs) to do so.

The downsides of the Travel Rule are technical and existential. Blockchains are pseudonymous by design. Real-world identity data attached to on-chain transactions establish huge “honeypots” of personal information. When an exchange is hacked — and they are, frequently — it isn’t just the money that gets stolen, but also the private financial histories and identities of millions of users.

And the “sunrise issue,” which means that countries are rolling out the rule at different speeds, has led to transactions failing and funds being frozen. A compliant exchange in Japan couldn’t have settled a transaction with an uncompliant exchange in Brazil, creating stuck assets and unsatisfied users.

The pros are mostly in the realm of crime prevention. And the lack of a Travel Rule makes crypto the ideal ransom demand and evasion-of-sanctions vehicle, law enforcement agencies say. By driving currency exchanges to share data, they build a paper trail that makes it much harder for bad actors to off-ramp their illegal gains into fiat currency.

The reaction here has been a resigned acceptance from centralized exchanges, who view it as just another cost of doing business, and abject horror from privacy advocates. The response has been the emergence of “noncustodial” or “self-hosted” wallets as an act of protest. Privacy-inclined users have moved off of central points and have opted to take on management of their own keys in order to stay out of the dragnet.

The DeFi Dilemma

Which brings us to the most controversial frontier of all: regulating DeFi and unhosted wallets. This is where the irresistible force of the state encounters the immovable object of decentralized code.

What’s at issue here is the specter of a “shadow financial system.” Regulators look at Decentralized Finance (DeFi) — robotraders, decentralized exchangers, algorithmic stablecoins — and see a black hole into which capital controls disappear. Ideas have been floated to mandate developers include “backdoors” or identity checks in the smart contracts themselves, or treat open-source software developers as financial intermediaries responsible for what their code is put toward.

The downside of trying to regulate DeFi in this way is existential. If developers are responsible for the protocol they created and no longer control, no one will code. The moment a smart contract is dependent on that passport scan, the DApp is no longer decentralized; it’s simply another complicated database update coffined in fintech clothing.

Such rules risk killing off the innovation that makes blockchain stand apart — its permissionless character. It imposes a centralized framework on a decentralized technology, then stands like King Canute trying to command the wind. The chilling effect such legal threats will have on the open-source developer community cannot be overstated.

The pros, in theory, are on systemic risk. If DeFi gets big enough, a failure within a major protocol could spill over into the broader economy. Regulators say they simply cannot let an alternative banking system operate without the safety rails (capital reserves and insurance) that, for better or worse, exist in traditional banking.

The response has been far and away the most intense. And it has mobilized its “crypto native” base to create DAOs (Decentralized Autonomous Organizations) specifically in order to lobby and battle these rules in court. The fallout is a tech race war: where regulators attempt to enforce borders, developers create privacy-caretaking technologies like zero-knowledge proofs (ZKPs) that allow us to mathematically prove compliance without revealing the underlying data — attempting to out-code the law.

The Cost of Compliance and Efficiency

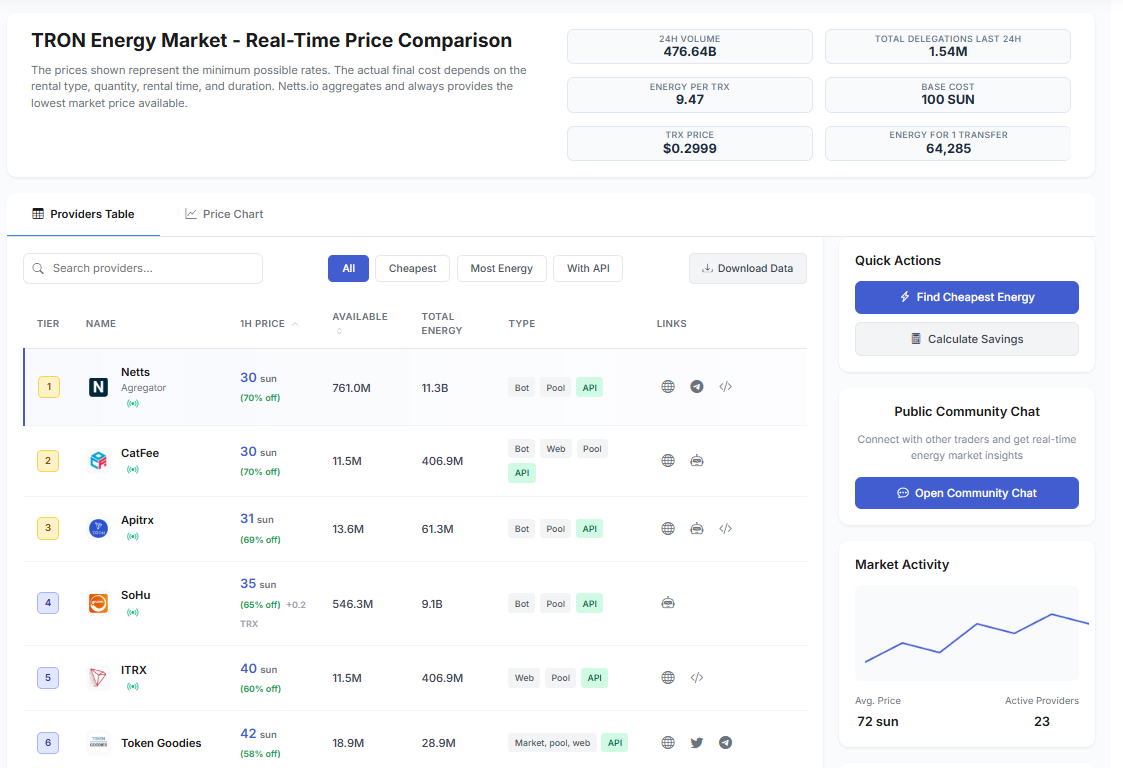

In this stiflingly regulatory environment, the economic situation for the user has evolved. Compliance costs money. Exchanges offload these costs onto users through trading fees, withdrawal fees and wider spreads. This has sent much of the market scurrying to find efficiencies wherever they may lie. The "base cost" of the interaction with c-high compliant chains has increased, rendering even more important the quest for low-cost (in terms of throughput), high-throughput alternatives.

So it’s in this combative cost-price environment that we see the persistent critical importance and relevance of networks such as TRON. As Ethereum and its Layer-2s struggle their way through the jungle of blog space, and sequencer decentralization, TRON silently held onto its crown as the rail for stable coin settlements. Still, when used frequently--even on those efficient networks--the charges can add up if you’re just burning the native token every time you deal. This economic pressure has spawned a 2nd market based solely on maximizing resources.

It won’t be long before the more savvy users and developers will figure out that burning TRX as gas every time you make a transaction is close to paying the “rack rate” at a hotel. Instead, there is a strong market for resources in the ecosystem. Renting TRON Energy has been a staple to anyone pushing solid amounts through. Whether you are a trading company executing thousands of arbitrage swaps per day, or a payment business settling merchant invoices, at the end of the day it is basic math: why burn 100% through staking when you can leverage rentals to lower that overhead dramatically lower?

These are markets where large TRX holders can freeeze their token and create Energy that is then delegated to a user in the platform that needs it. It is a symbiotic relationship. The holder receives yield on their asset without having to sell and the user gets cheap TRON Energy to perform transactions. And this layer of efficiency is not an oversight – it is a characteristic of the Delegated Proof of Stake (DPoS) consensus protocol that TRON currently implements. It incentivizes long-term agreement (staking/freezing) and therefore partly subsidizes active usage.

1. The clampdown on centralized on-ramps is adding impetus to on-chain activity.

2. On-chain activity necessitates Energy (computation) and Bandwidth (size).

3. These resources are most expensive when obtained directly from the protocol.

4. Affordability is driven by the second-hand rental market that offers the necessary discount to make business models feasible.

The very fact of these rental markets, in turn, suggests a fundamental misunderstanding on the part of regulators about who’s actually using their products. Regulators are fixated on the “who” — who is sending money, who is receiving it, who is issuing the token. Users can’t get enough of the “how” and the “how much” — how quickly can I send this, and at what cost to me. Rigorous regulations turn the "who" side of things into more time-consuming and costly processes and all that's left to decide upon which networks live or die is the "how much".

And if we analyze the trajectory of these regulations, stretching from MiCA to the Travel Rule, there is a pattern of cordoning off the open plains of crypto into walled communities. The “cons” are almost always about exclusion and cost; the “pros” around safety and legitimacy. But to the average user, to the one in Nigeria who is trying to use USDT to protect against inflation or the developer in Vietnam who is trying to build a game, all that high-minded discussion on systemic stability doesn’t matter as much as what that transaction fee says on their screen.

This is why anything that abstracts away complexity and cost has a good chance of being the new valuable infrastructure layer. In a universe where sending value would likely initiate three different compliance checks and a tax in and of itself the transport layer needs to be kept as cheap and efficient as possible. The energy bandwith market is far from a sui-generis financial derivative, it's essentially an insurance policy against ATOMIC compliance risk which adds to retained earnings.

Conclusion: Finding the Balance

So, how far is too far? When regulation makes a friction-less technology start to look more like a friction-full one, it arguably has gone too far. When it drives users back into the clutches of the same middlemen they were trying to escape, it has missed it. But the strength of the crypto ecosystem lies in its flexible nature. When a high gate of costs and red tape bars the front door, communities construct a side door of optimization and efficiency.

An excellent example of its flexibility and efficiency is the blossoming eco-system for TRON's resource model. Getting the best rate for your transaction requirements from a mix of providers can be complex, since depending on network demand or provider liquidity, prices change. This is where Netts steps in.

Netts gives you an all-in-one aggregator - TRON Price Comparison where you get also a live comparator of Energy (Compare over 20 suppliers). With Netts, users can now immediately find the cheapest energy available — often as much as 90% cheaper than burning TRX — and rent easily with one click. Whether for a one off transfer or regular monthly payments, Netts.io makes sure that you are always taking the most efficient route for all your on-chain operations, and that the bloom of decentralized finance does not get out of hand even as the regulatory skies cloud over.