Crypto and Divorce: Who Gets the Wallet?

Crypto divorces collide with volatile valuations, self-custodied wallets, freezing orders, and the forensic hunters chasing hidden coins.

To be a divorce lawyer has to be one of the most secure jobs in the history of existence, and the motivation for this is sadly not cynical — it is anthropological. Those promises were made under a certain set of emotional weather conditions, and then the weather changed. The wedding photographer freezes a moment that rotten away on a timetable that none of us want to fess up to, and the lawyer gets the other end of the contract when that timetable rubber-bands up. Marriage is an arrangement for people who hardly ever become one flesh anymore considering the forlorn unification from romance to the friction of shared bathrooms, shared bills and shared disappointments. And when it does fail, it fails with a kind of pyrotechnic fury neither would have believed themselves capable of five years ago.

In this context, money has always been a placeholder for grievance. All of these become standards of battle that are marched into a courtroom. Crypto fulfills everything that regular assets do during divorce, and more than that it does several things that they have never done. The million-dollar question — what is this wallet worth? — is true for about the next fifteen minutes. In a nine-monther, that answer will be wrong, possibly calamitously so, by every date that matters.

Moving Target Problem

Every family court has been valuing a house for decades. You have an appraisal, you take a deep breath but maybe you get a second opinion, you arrive at an instrument-friendly figure. Stocks are volatile too, but there are known systems for mitigating this — date of filing, date of trial, average close over a number of days. The quality of the swings are qualitatively different, thus crypto pushes through those conventions. A portfolio that is worth a hundred thousand dollars the day divorce papers are filed could be a forty thousand when the exes sit across from one another at mediation, or it could be a two hundred. Neither side is lying about the number they remember, just that they remembered different weeks.

California courts opted for the filing date as an anchor and wades crypto into the waters of all volatile assets. Some other states also will consider the date of trial, or allow the parties to negotiate the valuation date as a part of the settlement. Date is everything, and whatever date it is can move a marital estate by multiples and neither spouse knows in advance where that date is going to land them. A 40 percent rally would likely change the mind of someone who was clear-cut in their desire for a trial. A person who felt prepared to put down roots goes quiet after a wreck and begs for an updated assessment.

Not even completing the altcoin part. Bitcoin is the stable one (as tired as this metaphor is). The back end of the market is moved with a scale and speed that currently makes Bitcoin a government bond comparison. A meme token had three or four hundred thousand dollars behind it in January before being a hundred thousand in February and drifting to eight thousand dollars by April — not because the project did anything in particular, but because the attention drifted. In short, best of luck with that price action explanation in front of a judge that has been valuing sliced up marital estates (which is how price action works) for 30 years using methods from before the commercial internet was ever a thing.

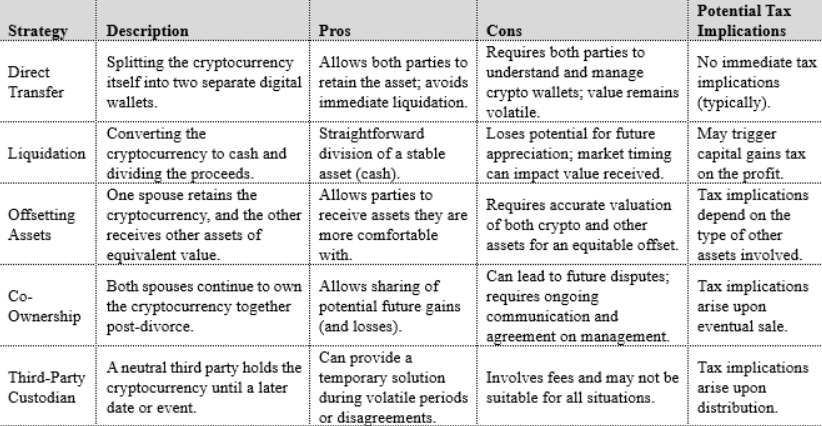

To get around the problem, some practitioners have attempted to divide the holdings "in kind" — so each party ends up with the same proportional share of each token. In theory this circumvents the valuation battle in its entirety, since whatever happens to the price post-split happens to both sides in equal measure. This seems simple in theory, but in practice it gets complicated fast. The husband may not want exposure to certain tokens at all or may not have the technical ability to manage self-custody properly. The spouse may have absorbed the original investment thesis and really wants the position; the other may have been just along for the ride and wants cash. Courts commonly find themselves with hybrid solutions where some holdings are divided in kind, some are sold and divided, and a third bucket is traded for offsetting traditional assets.

Video Game Loot and What It Taught the Courts

Before crypto made it an issue, though, courts have already wrestled with intangible, unpredictable, internet-native value. Video games, of all places, provided the early test cases. For two decades now virtual items in World of Warcraft, EVE Online and Second Life have been traded for real dollars, occasionally for considerable ones. In 2013, a Chinese court ruled that the assets associated with the game WoW, and purchased using real-world money, were property. By contrast, a 2010 U.S. court examining Second Life came down the other way, finding that in-game items were a form of play, not legally speaking property. Various jurisdictions, various philosophy, only one fundamental conundrum: is something an asset if its existence only exists on a company's servers and its price rests entirely on the interest of other players in it?

However, that question set is bigger now, because crypto takes those same questions and does the basic math — global markets, instant transferability and 24/7 trading. The slowest-moving item of value — even virtual gold in a video game — behaves like a cryptocurrency to the degree that in-game economies are bound by the slow-moving nature of its internal economy (farming rates and patch schedules, for example). Nothing more, nothing less than the collective mood that bounds a speculative token. In an action for divorce that stretches over months, this is essentially the difference between a cubit of wood and a cubit of weather.

Freeze

The common response is a freezing order where one spouse seeks to restrain the other from dealing with the crypto or moving it to a new wallet when they suspect the other is about to move or sell. We have had this for other assets for ages — bank accounts get frozen, safe-deposit boxes get sealed, real estates get tagged. That in the courts has already begun to be applied to crypto, and the order can be expanded, so that covers not only the personal fees of the partner, but also the legal exchange that may be their facilitation. This means if your ex is attempting to send money via a large exchange, that exchange can be served and forced to cooperate.

The challenge is that a freezing order against a self-custodied wallet is real in writing only. The holder has the private keys. The court can lock them out of moving funds, and could impose punishments on them for doing so, but the network itself is not a party to the order — it gets on with its business and processes the transaction anyway. Enforcement is a forensic exercise — you retrospectively prove the breach of the order and the court comes down hard on the breacher. Better than nothing, of course, but not the same as actually preventing.

There is also the psychological tax on the frozen period itself. Divorce is inherently slow, contentious and draining. One particular pain involves layering on a six-figure crypto position that you cannot touch at all, and then within a few weeks it's moving in either direction 20 percent. You see a number that in theory is half yours, free fall, knowing that the eventual split will be determined as of a date no one has yet put on their calendar. Or perhaps, depending on the spouse, would actually rather lose the entire title than endure it for a year?

Notably, a larger percentage of couples with material crypto exposure now tackle the issue head-on — in prenups or postnups that clarify how digital assets will be dealt with in the event of a split. Such agreements can even set out a valuation protocol, an expert to carry out the valuation, and require both sides to maintain an updated schedule of wallets throughout the marriage. It isn't romantic, but it sure is cheaper than finding out six years down the line that you've married someone who has crypto on five chains you'd never heard of and a tax situation that nobody ever recorded.

Crypto Hunters and Hidden Wallets

This is an understatement the size of a house as no two divorce is ever civilized. And in the worst situations, one spouse attempts to hide or remove the assets prior to any obligation to disclose them. Cash can be converted to bitcoin and sent to a wallet whose address never appears in any other document. Bitcoin can be exchanged for Monero or other privacy coins, which are constructed to withstand precisely that type of analysis to which investigators have become so accustomed. This means that funds can be routed via mixers, divided into minuscule denominations, routed through multiple jurisdictions and recombined at the other end.

This in turn has given birth to a niche industry. Even crypto tracing forensic accountants will scour bank statements for transfers sent to exchanges, obtain exchange records via subpoena, then follow on-chain trail. In a widely reported case, a husband transferred half a million U.S. dollars worth of Bitcoin to a private wallet during divorce proceedings; the wife hired a crypto investigator to locate the funds and did; they were eventually returned. Another widely disseminated case involved a New York wife whose husband was making millions a year — she spent six months on discovery with a forensic accountant, only to find a secret wallet containing twelve Bitcoin.

Courts have gotten tough on spouses hiding crypto. Penalties vary from being required to pay the other side's fees, to the whole asset being awarded to the spouse who laid bare the ruse. Contempt charges are increasingly common. All of these things do not entirely solve the privacy coins and advanced mixing problem, but it achieves a strong enough deterrent that, outside of a handful of the smartest and most sophisticated hiding techniques, attempts are often too clumsy to evade detection. The blockchain forensics world today is more robust than many would have guessed and an investigator that is tenacious and armed with a subpoena is truly difficult to beat.

Concealers are rarely outed by the sophistication of their crypto dealings, but by the triteness of their daily routines. Those in hiding with hundreds of thousands of dollars do not typically lead lives of poverty. In the early stages of an investigation, lifestyle analysis — cars, vacations, credit-card activity, jewelry purchases — is often more useful in producing leads than blockchain analysis, and blockchain analysis will confirm the theory. When paired with subpoenaed exchange records of on- and off-ramps, an experienced investigator can create a case that's damn near impossible for even the most advanced wallets to fight back against.

Ten-Wallet Problem

A clean divorce also stumbles on problems crypto imposes less in malice than in structure. Now think of the long-term holder that built his portfolio the right way over a decade and is now a divorcee with respect to his partner. He has ten wallets. One of the three is a hardware device. One of which is on an exchange that he no longer trades on. Two of those are hot wallets on phones he had at different times. Those four are tied to DeFi protocols where tokens are staked for yield, lent out to others or locked into liquidity pools. He is in a dozen tokens. Many of these are not listed on major exchanges and only trade on infrastructure like the TRON Energy market and other dedicated ecosystem venues. So what on earth is the marital estate supposed to do with all this?

You hire an analyst. The analyst creates a live dashboard, scrapes prices from numerous sources, matches wallet addresses to on-chain assets, and compiles a paper that will be rendered obsolete by next week's hearing. They charge you by the hour, and hours build up. They will also have to deal with items that traditional accountants would rarely encounter:

1. Tokens that get locked in and untaken up periods of a few days or weeks, but early withdrawal comes with a penalty.

2. Liquidity-pool positions that are held by both assets that are flowing simultaneously, causing the position to go up or down depending on the price ratio between these two assets.

3. NFT holdings with theoretical floor prices that are probably not being offered, since there is no buyer for the floor at the time of valuation.

4. Tokens you earned as yield during the process (and whether that goes into the marital pot depends on the jurisdiction's law about income accrued after filing).

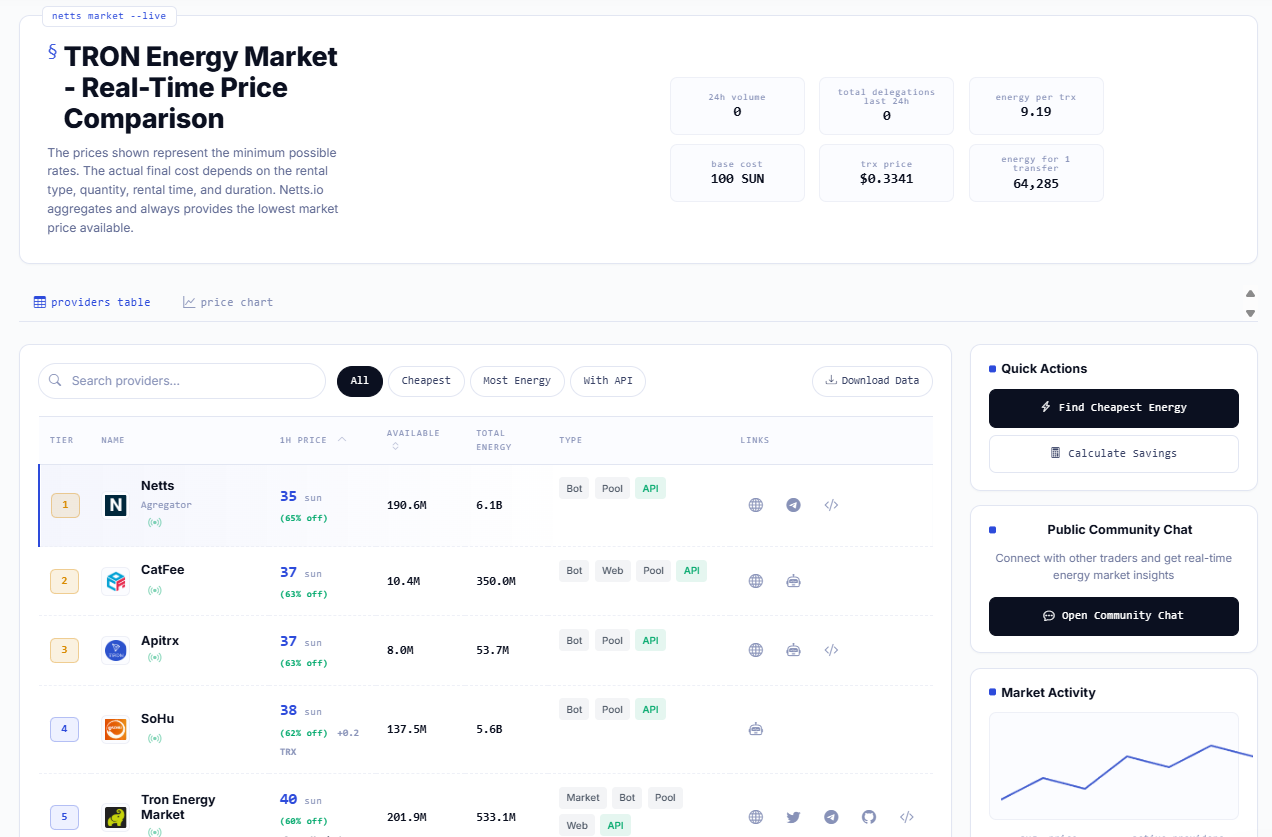

5. Holdings of TRC20 and equivalents, for which the transfer consumes resources such as Energy and Bandwidth, impacting any effective liquidity assessment.

It's that last category that often gets overlooked by the casual observer. For example, moving a portfolio on the TRON network isn't free — each transfer requires Energy, and if you didn't have any staked or rented the network burns TRX to offset the cost. A pair cashing out hundreds of USDT transfers during the settlement may find themselves with a nontrivial transaction overhead, unless both are aware to buy TRON Energy ahead of time or route via an aggregator with cheap enough TRON Energy to make the endeavor economical. It's one of those details that will keep a forty-thousand-dollar transfer clean, or, it will cause a couple hundred buck erosion into network costs before dollars hit either spouse's account.

The result is that a sufficiently-complicated crypto divorce resembles less a real-estate dispute and more a corporate-merger due-diligence exercise — only the target company is revaluing itself every minute and the shareholders are scrambling to get divorced during the audit.

Slowly, courts are developing a body of case law, and by and large, it is trending toward treating crypto as just another asset that cannot be wished out of existence. Judges are becoming more fluent. A whole sub-practice of divorce lawyers have begun carving out a practice specializing in digital-asset divorces. Once something of a novelty, forensic investigators have quickly become a standard line item in pretty much any divorce involving significant crypto holdings. This will all look as mundane in twenty years — as customary as simply valuing a brokerage account looks today — but right now we are slogging through its awkward adolescence.

What has not been resolved — and perhaps will never be resolved cleanly — is the very nature of valuing a price that is set by a global, 24/7, permissionless market. Courts can pick a date. They can pick an average. They are free to choose whichever convention they like. The markets will keep moving, and there will always be someone who will feel that they have come out of the deal with the short end of the stick. As with any volatile asset, that is true, but the volatility in crypto is structural yet both sides widely seem to know that by the time they are standing at the altar together.

Whether liquidations — wallet-to-wallet transfers — final settlement payouts — whatever the case, for anyone with activity inside the TRON ecosystem finding out what each transaction costs is as simple as comparing live prices across providers. Netts manages an aggregator-style Energy market that draws real-time rates from over twenty competing services, with the cheapest at present about 37 sun effective below the 100 sun burn base rate (a nominal discount of roughly 63 percent on the maximum effective TRX burn). This live comparison shows users the quickest route from "what does this cost me" to "sent"; ideal for anyone that needs to move USDT in bulk, or anyone that just wants to buy TRON Energy at the lowest rate available without searching multiple provider sites.