Crypto and Commerce: Selling for Tokens

Merchants meet a thousand tokens — volatility, checkout UX, and USDT fee reality on busy chains when “money” stops being just cards and fiat.

The traditional wisdom of the marketplace is that the customer is always right. It is a mantra that has driven service and sales for decades – making the person with the purse strings feel important, respected and listened to. But in our digital economy, there is a practical revision to the rule that every business owner understands but few say out loud: The customer may always be right, except when he isn’t. “Money” used to be a simple thing. It was the paper money that filled a wallet, the check you used to pay for groceries, or even the little plastic card — perhaps increasingly virtual — that linked to your bank account.

But now the definition of what counts as “money” keeps expanding at a pace that would leave an old-school banker dizzy. It’s no longer a world just about Dollars, Euros and Yen. We’ve moved into the age of decentralized finance, where value is held in thousands of tokens, each with its own community, rules and volatility. There’s also the emerging reality that, for a merchant looking to keep up with the times, it’s no longer just “cash or credit?” It is a complicated calculus of which digital assets to invite into their shopping experience and which to leave at the door.

The Paradox of Choice

However, there are so many cryptos available that a paradox of choice is starting to occur. Thousands of tokens percolate in the digital ether, from trillion-dollar behemoths like Bitcoin to some random pitchfork launched yesterday by a teenager in a basement. Which ones do you accept? Which ones do you neglect for other parts of your business? The answer is not as easy as it seems to follow most popular tags. It takes a deep, nuanced insight into your customer base and how they act.

Now consider a user who wants to buy your product but insists on using a token that you’ve never heard of. Maybe they’re the early adopter of some new decentralized finance protocol or perhaps they just can’t be bothered with converting their holdings to a more traditional form of money. There’s the rebellious factor, too. Many of those who use crypto see themselves as outside the traditional financial system. Some individuals may simply decline to employ certain fiat payments out of principle, while others might not have access to legacy banking rails because they live in countries where political or geographic barriers are an obstacle.

If you turn down their opaque cryptotoken, they’ll walk away. And if you do, you assume the risk of owning an asset that could be illiquid, or even worthless when you want to sell it. This friction — between what the user has and what the merchant desires — is what constitutes the chief battle of crypto commerce in 2026. The most reasonable tokens to add to a buying service for the majority of sites, start ups & companies is one that tries to aim a balance between user adoption and merchant stability.

Bitcoin, Ethereum, and Stablecoins

The first and most obvious one is bitcoin. It is the U.S. dollar of crypto, as well as the “digital gold” that the majority of cryptocurrency holders own. It’s a signal of legitimacy, an indication of being open to the new economy (even if its transaction times can be slower for point-of-sale retail). The second codebase should be Ethereum because it fuels a huge ecosystem of applications and is common among the friend group that has technical knowledge. No, the real bridge between crypto and traditional commerce are stablecoins.

Tokens like USDT and USDC are pegged to the U.S. dollar, providing the speed and borderless nature of cryptocurrency without plummeting you into heart-stopping volatility. For a business that must pay suppliers, rent and salaries in fiat currency, stablecoins are frequently the most practical on-ramp. They make it so a customer can transmit USDT anywhere in the world instantaneously, clearing the transaction with finality equal to cash but making it as convenient as sending an email.

The gap between the two types of businesses greatly changes which tokens should be taken and which should not. A digital goods reseller with high margins (like software subscriptions or digital art), for example, has a very different risk profile from a low-margin physical electronics retailer. The seller of digital goods has zero/marginal costs of production almost. Even if they do accept a volatile token that falls ten percent in price between accepting it and converting it, they’re still hugely up.

They can be more experimental, by maybe accepting a wider range of “meme coins” or community tokens to reach niche audiences and create brand loyalty. The electronics store, by comparison, survives on razor-thin margins. A 5 percent decline in a token’s value and they could lose their entire profit on a sale; worse, actually find themselves with a loss. Volatility is also the enemy of this business. They have to stick with stablecoins, or rely on payment processors that convert crypto into fiat at the current moment before a purchase is made. They can ill afford the luxury of keeping a speculative asset for even hours.

The Challenge of Volatility

Which brings us to the key challenge: Volatility. Instead of building as much as you want, you're just going to nibble a bit and try and figure out if it's worth taking time to get into something that could be gone in a week. For most businesses, the answer is a clear no. The crypto market is strewn with corpses of projects that were shilled so hard one month and then tossed the next. Adopting a new token in any payment system does not come for free. It costs in developer time and effort to set up the wallet infrastructure, accounting time to determine how to track this new type of asset, as well as staff education on handling customer service issues around the new payment mechanism.

All that investment goes down the drain if that token drops 90% or gets delisted from major exchanges. Identifying whether hiring managers are vetting sales candidate as much as possible. A token should have been around for a substantial amount of time, be part of a successful project with heavy daily trading volume and be listed on major exchanges to even consider acceptance. The idea is to enable commerce, not operate a crypto hedge fund. The merchant should be taking value, not going long on the future price of a digital asset.

Wallet Management and Security

The crypto space has several problems in store for the unprepared trader. One of them is the practical nightmare around wallet management. It can be tempting to simply make a new wallet for every single token you want to accept. Before you know it, you’re trying to keep track of 50 keys and seed phrases associated with 50 different wallets, introducing a security risk and an administration headache. Stone’s colleagues learned that when you lose a private key, the money it protects is gone for good; there is no bank manager to whom you can call and ask him or her to reset your password.

It is also very hard to sweep money around in this fragmented trading of liquidity way. You could, say, have 500 dollars in the form of fifty various currencies and yet not be able to pay a single bill any better for any of it. That said, many businesses try to solve this issue by adding a middleman — better known as a third-party crypto payment processor. These services offer to take care of all technical complexity, accepting whatever token the customer wants to send and depositing fiat in the merchant’s bank account.

It sounds like a dream, but it does have a price. These middlemen tend to charge an outsized fee for their services — and in some cases much more than traditional credit card processors. They also reintroduce centralization risk. If the processor's platform crashes, or they failed your account due to some mysterious "flagged" transaction, you are out of luck and cannot get at your own hard earned money. In addition, businesses may be thrown off by the technical details of blockchain transactions.

Transaction Costs and Network Fees

In contrast to credit card networks with a typically steady percentage, blockchain network fees can spike wildly from congestion. On networks such as Ethereum, the “gas” fee necessary to conduct a transaction can cost more than the item being bought, particularly in cases where it is for small-ticket purchases. Enter a very bad user experience: you want to sell someone a ten-dollar t-shirt but have to ask another twenty dollars in transaction fees.

This is why many high-TX merchants opt for coins that are engineered to handle lower fees and higher throughput, such as TRON. But even on TRON, there is a catch. The network is regulated by a resource allocation mechanism called Energy and Bandwidth. Whenever you transfer USDT, or interact with a smart contract you spend these resources. If you don’t have enough Energy and Bandwidth staked or rented on your wallet, then the network will burn the TRX you already hold to cover the costs of it. This is supposed to be a spam deterrent, but for a legitimate business, it feels like punishment for success.

For a business doing hundreds or thousands of transactions daily, this incineration of TRX can chip away at profitability in silence. It's one of those things that when people look at their monthly balance in horror and ask "Why don't I have my TRX?" they fail to calculate. Doing that takes a bit of a mindset shift. You then need to start thinking about “transaction cost management” in a fashion that is not present in traditional finance. You need to understand how your blockchain works.

For one, on TRON network: Sending USDT to an address that already has some USDT will consume less Energy than sending it to a zero balance. This is because the network needs to set up a new record for empty address, which takes more computation cost. A smart business owner, or a technical lead on staff must understand these things. They should calculate fee charge implications for various scenarios and change their price levels or treasury management policy. Not taking advantage of these mechanics is like leaving all the lights on in a warehouse with no one there, just wasting resources to do nothing.

Tax Compliance and Privacy

Regulatory and tax environment is also something to think about. Accepting crypto is not just a technical hurdle; it’s a compliance one. When a customer pays in crypto, it’s considered a taxable event. If you have that crypto, and its value goes up before you sell or trade it for something else, that is also a taxable event. If the value falls it is a capital loss. For traditional accountants who are used to dealing with cost basis on a handful of transactions, the thought of tracking thousands of tiny micro-transactions is enough to give them nightmares.

This is another case for the fast conversion into stablecoins. If you keep everything in USDT or USDC, you have effectively pinned the value of that thing to the dollar, making accounting a breeze and saving yourself from both FOMO and surprise tax bills at year’s end as phantom gains somehow vanish without actually running through your accounts. Your "lazy or rebellious" user may not be interested in your tax obligations, but the IRS takes a different view. It also opens a data privacy liability since wallet addresses are now matched to customer identities. Under rules such as GDPR you are required to treat this data with the same care as a credit card number.

The Future of Crypto Payments

The trend is obvious, however. The barriers to entry are falling, and the tools are improving. We are transitioning away from the early ‘Wild West’ days, in which it was strictly required to run a full node on a server sitting in your back room along with all our emails. Today, the infrastructure is maturing. We are beginning to see the emergence of decentralized payment gateways where businesses can accept payments directly into their own self-custodial wallets without any middlemen seeking rent.

Such tools also tend to plug in directly to major e-commerce platforms, so the “pay with crypto” button is merely an alternative along with Visa or PayPal. This disintermediation is the real promise of crypto and commerce. It brings back the immediacy of buyer and seller, it gets rid of the banks and processors who have put themselves in the middle of every transaction for fifty years. It enables a coffee shop in Berlin to accept payment from a visitor from Seoul without paying a three percent foreign transaction fee. It makes it possible for a freelance developer in Nigeria to work with a client in New York without losing 10 percent to wire fees.

However, self-sovereignty implies responsibility. If you are going to be your own bank, you need to act like one. You must secure your keys. You must verify your addresses. And you have to understand the cost of doing business on the blockchain. The businesses that make their way through this new landscape will be the ones who educate themselves.” They’re not just going to take any token; they’re going to define a list of assets that make sense for their bottom line.

They won’t simply pay what the network asks for; they will find ways to predict and minimize those costs. They will also treat Energy and Bandwidth as tangible resources, rather than abstract quantities, just like how we manage inventory or the flow of electricity. They will realize that efficiency in crypto is not only about how fast, but also how wisely resources are used. The customer who wants to pay with their tokens isn’t going anywhere.

Indeed, as a generation that is more comfortable with digital wallets than bank accounts comes of age, this demographic will only grow. They like the privacy, the speed and the independence that crypto provides. For them, money is programmable, global and open. A company that ignores this transformation is shutting out the future. But the business that embraces it uncritically will be welcoming chaos. And that middle way is one of wise acceptance. It is also a way of saying, “Yes, we accept the future of money, but we do so in terms that guarantee we will still be here next year.” It’s about constructing a system that is resilient enough to withstand the volatility, clever enough to keep fees from leaching its gains and flexible enough to accommodate whatever new token captures the public imagination next.

Tools for Efficiency

While we continue to navigate these complexities, one type of tool has surfaced that helps businesses handle the technical burden of processing cryptopayments — especially on a high-traffic network like TRON. Controlling USDT transfer costs are the lifeblood of any merchant in this industry.

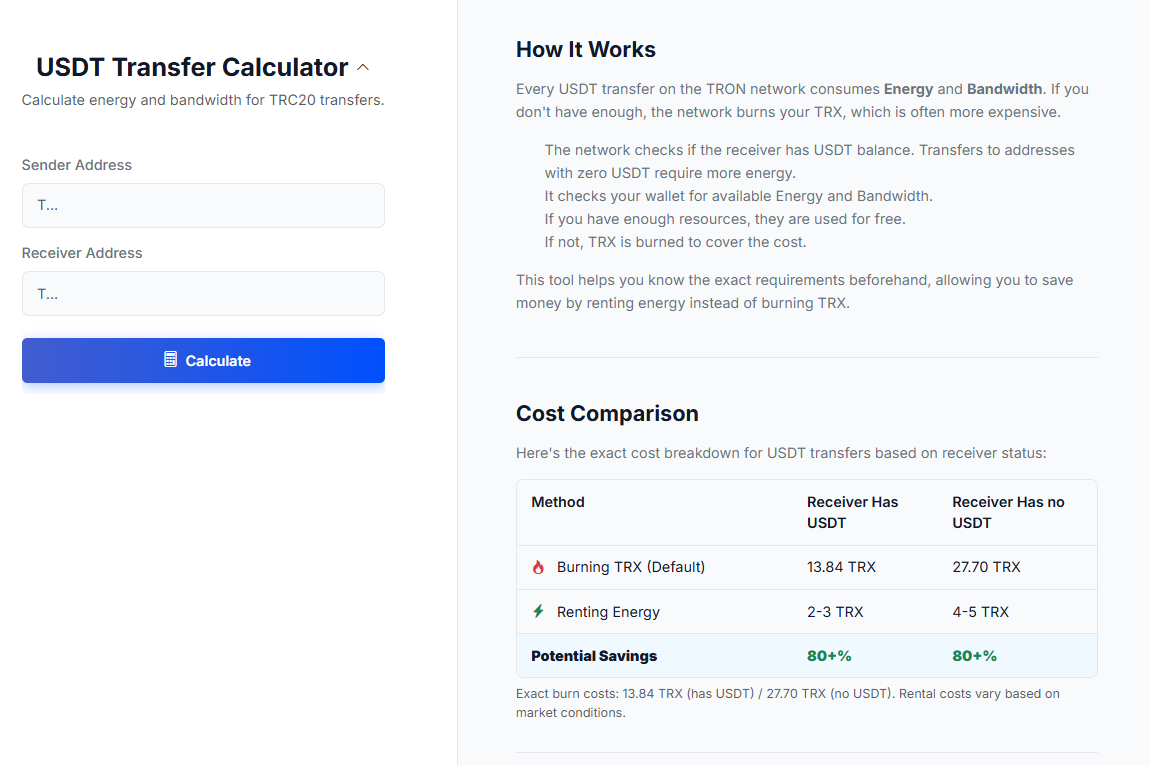

Netts USDT Transfer Calculator is a must have tool for any business operating in the TRON network. It lets you estimate energy and bandwidth costs for TRC20 transfers with granular accuracy. To do this it starts with sender and receiver addresses (“T…”) to predict the cost using the on-chain state. It takes into consideration the dynamic of the network, that is transfers to addresses with 0 USDT account for way much more Energy (and thus cost) than to an address with already a balance.

The calculator gives you a transparent price comparison – the standard process for burning TRX is going to cost 13.84x TRX, and that jumps up to 27.70x if the recipient doesn’t have USDT on hand. Instead, the tool shines in its ability to rent Energy, potentially costing just 2-5 TRX — over an 80% saving. This is not just a minor optimization, but if you’re a business sending out thousands of payments, it’s good savings. The service also provides an API to enable the automatic scanning by developers. Business(es) can plug these cost computations directly into their backend logic and make sure that every send USDT is done at a minimal fees. It comes with a rate limit of 6 requests per minute per IP, giving you a stable and constant way on how to query the network state before throwing money at it.