Best Cryptocurrency Practices for Shopping

Split wallets, verify addresses, prefer stablecoins, mind congestion — plus Bandwidth and Energy literacy so retail crypto spending stays sane.

Few things are more frustrating than being at a checkout counter — in the physical or digital worlds — and having a transaction fail. You have done the research, located that perfect product and committed to the purchase only for everything to come screeching to a halt because some crusty old bank’s wheels decide they need greasing. Maybe a fraud flag because of a location you don’t usually visit, maybe it’s your daily spending limit that you forgot about, or could be some system maintenance window nobody told you about.

At that point, the thrill of buying has long since dissipated as you fumble through customer support lines and security questions. No one actually wants to deal with money or banks; they just want things that improve their lives. The currency is simply a means to an end, and when that means gets in the way then your pleasant shopping experience turns into drudgery. Beyond the hoax factor, there is a nagging feeling that someone has trespassed. Each swipe of a card contributes to a profile about your behavior, location and preferences — one made all the more potent because it’s often being sold or deployed without your agreement. The old banking system of course, heavily dependent on the control and oversight by layers of middlemen, often seems less like a service than merely another gatekeeper that you must placate in order to have any access at all to your hard-earned resources.

The Exchange: Ground From Barter to Blockchain

To understand why we are here, consider how we came to exchange value. Its origins are simple but not efficient; you trade a goat for a sack of grain. After all, if you didn’t have a goat, you could not buy the grain. How heavy, bulky and dangerous are such coins? Paper money came next, a value abstraction secured by governments that enabled larger economies — but opened the possibility of inflation and devaluation. The digital age brought us credit cards, which in turn gave rise to online banking, and a world of convenience — except that it all just digitized the old ledger system, now with layers of middlemen who are each taking a cut and want surveillance rights.

It’s the next logical step in that evolution. It marries the portability of digital data with the scarcity and independence of physical cash. It is money made for the internet, not money adjusted for the internet. When you shop with crypto, you’re taking part in a financial system that doesn’t stop — it operates 24 hours a day, seven days a week, without holidays and without banking hours and geographical limits. Never before has someone in Tokyo been able to pay someone in New York instantaneously, securely and with no banks involved at all. This is not just a new way to pay, but a rethinking of our relationship with sellers that returns the power imbalance we lost when we surrendered financial sovereignty to centralized institutions.

Luckily, we’ve got something of a paradigm shift in commerce happening under our feet. We’re concluding the days of centralized powers telling us what can be bought and when, and instead transitioning to a more self-reliant future driven by cryptocurrency. With the early days of crypto dominated by speculators and tech enthusiasts discussing holding strategies, today’s reality is a practical one. Purchasing with digital assets is emerging as an increasingly secure and sometimes cheaper option than traditional money transfers. It provides a lack of intermediaries that traditional finance cannot replicate.

When you pay with crypto, it is akin to handing cash to a merchant only the transaction can be made in an instant anywhere on earth. There is no middleman stepping in to kill the deal because he thinks you are purchasing too many electronics, and there is no three-day delay for funds to clear. But this transition is not really about the tech: It’s about taking back our ability to engage in transactions. As additional digital goods platforms and forward-facing retailers embrace crypto payment gateways, that friction of shopping is being worn down, and the end result now for consumers is a smoother more simplified process.

Real-Life Examples: the Traveler & the Gamer

To grasp the difference, think of an international traveler. Let's say Sarah is traveling in a country that doesn't accept her home currency. In Sarah’s old world of finance, she uses her credit card. And each time she uses an ATM to take out some cash for a souvenir, or pays for a meal with her card, there is a foreign transaction fee. Even worse, her bank would be likely to suddenly freeze her card if she tried to purchase something expensive for “suspicious activity” because she’s thousands of miles away from home. Then she’s stranded in a shop, trying desperately to call her bank and get her savings unlocked.

Now imagine the same situation, for a crypto user. They take their wallet app out of their pocket, scan a QR code and make the payment. The network doesn’t mind which countries they are in. It doesn’t charge an additional percentage for just crossing a border. It’s a done deal, secure and done in seconds. Already, the crypto user has their purchase and the traditional finance user is still on hold with customer support.

Another similar scenario is when buying expensive electronics or luxury items. Consider David, a tech fanatic who's in the market for a high-end workstation setup that will set him back several thousand dollars. He tries to pay for it with his debit card, but the sale is denied because he has reached his daily spending maximum — a cap imposed by the bank as a hedge against fraud, although quite likely only an arbitrary one.

He then must log in to his banking app, find the setting he needs or call support to raise the cap temporarily, which can take an hour. All of this time for the specific thing he is interested in — and the limited quantity of that item goes out of stock. If David had been paying with crypto, the idea of a “daily limit” would not even make sense. If he has the money in his pocket, he can spend it. The blockchain does not nanny him; it just takes orders from him. He makes the payment, the order is confirmed and he purchases his equipment without having to look for permission to use their own money.

But now think about a gamer or digital native who spends money on virtual goods. Consider Mike, who desires to acquire a unique item in an online game from a seller living on another continent. Via traditional banking, a wire transfer might take days and incur fees that added up fast. And even services like PayPal might have high conversion fees or freeze suddenly if they decide the transfer seems risky. Now, if Mike is using cryptocurrency (let’s say a fast network like TRON), then it becomes peer-to-peer. He sends the agreed-upon amount, the seller gets it a few minutes later, and the merchandise changes hands. The efficiency is incomparable. All borders, bank hours are pure friction. This is true whether you’re purchasing software services, VPN subscriptions or any digital product that has immediate access as its aim. The crypto user has already initiated a download and use of his purchase, yet the bank user is still waiting for an email confirmation.

Privacy and Autonomy in Purchasing

The primary reason you might argue that paying for stuff in crypto is more rational than using fiat isn't because it saves fees, but because it grants the user privacy. Under this old regime, your bank statement is a diary of your life. The bank knows if you purchase a particular kind of medicine, a book perhaps that’s controversial, or just any spending in an establishment you might not want to be known for visiting. This stuff can affect your credit score, insurance premiums or just help people target you with ads. But for the crypto user, this is not the case. That’s because, despite the fact that all content goes on the blockchain as a public ledger of what has occurred, your personal identity isn’t attached to every transaction in the same sense. You control your wallet. When you buy something, you are transmitting value, not your entire life story.

In the age of data as the new oil, corporate interests are mining your financial habits to create predictive models of how you’ll act. They know when you buy groceries, how frequently you travel and what entertainment you consume. This data is harvested, then sold off to third parties and used to influence your future buying behavior. Shopping with cryptocurrency disrupts this cycle of surveillance. The merchant gets paid, and you get your stuff but the invisible web of data brokers is cut out of the equation. You’re not a data point to be mined, an extractive resource that can be pillaged continuously. You are just a customer making a transaction. This move toward simpler, more private forms of commerce is not about hiding from the world for its own sake but about preserving human dignity in an age that increasingly views people as vectors of shadowy forces.

Imagine you are going to buy a gift for a spouse, but you want it to be a surprise. If you share a credit card, the surprise is gone once they check your banking app. With crypto, you can have that as the freedom to discreetly do whatever you want with your money. This is not an issue of hiding criminal activity, it is a matter which only addresses the reasonable expectation to privacy in one's personal life. As we continue on our path toward a digital-first world, the ability to transact without bequeathing a permanent fingerprint for corporate surveillance is becoming ever more valuable. The added sense of confidence that your shopping and purchasing habits are no one else’s business offers an extra layer of security during the payment process as the mainstream banks simply can’t provide.

Security & Responsibility: You Are the Bank

With the extreme affordability of financial freedom comes an equally powerful duty for security. With regular cards, you have a safety net: If you screw up or get defrauded, the bank can generally reverse the charge. In the world of cryptocurrencies, transactions are immutable. That means once users send the money, it’s gone. This is the essence of buyer responsibility where customers are not simply passive dependents on institutions. It sounds scary, but it’s actually liberating. It promotes a level of mindfulness about your money that’s often missing in the fiat world of “one-click buy.”

To shop safely, you need to know the tools of the trade. First there are hot wallets and cold wallets. A hot wallet is accessible via the internet — it could be an app on your phone or a browser extension. These are great for everyday shopping, storing small amounts of crypto that you intend to spend (much like the cash you keep in your wallet). Or have you? You wouldn't travel with your life savings in the pocket of your trousers, would you? Of course not! And like most people, walking around crowded streets or underground trains with everything they own on them — including their retirement fund — which is essentially what you're doing when keeping all your life savings on a hot wallet. For larger amounts, savings or long term — a cold wallet (the wallet is an actual physical device that stays offline) is used. The savvy shopper stores the majority of their savings in cold storage and only sends what they need for the week or month to their hot wallet.

And on top of that security, your shopping is even protected in how you transact with the sellers. In the world of crypto, payments are pushed rather than pulled. When you use a credit card, you hand over your card details and give the merchant permission to take money from your account. And if they get hacked, so do your details. You do not disclose your private keys when you make a payment with crypto. You just send the amount you're asked to directly to the merchant's address. Even in the event where the merchant's systems are hypothetically fully compromised, your funds remain safe as you never gave them the "keys to the castle"! This "push" method is also more secure for the buyer than a "pull" from traditional cards.

Navigating Fees and Resources

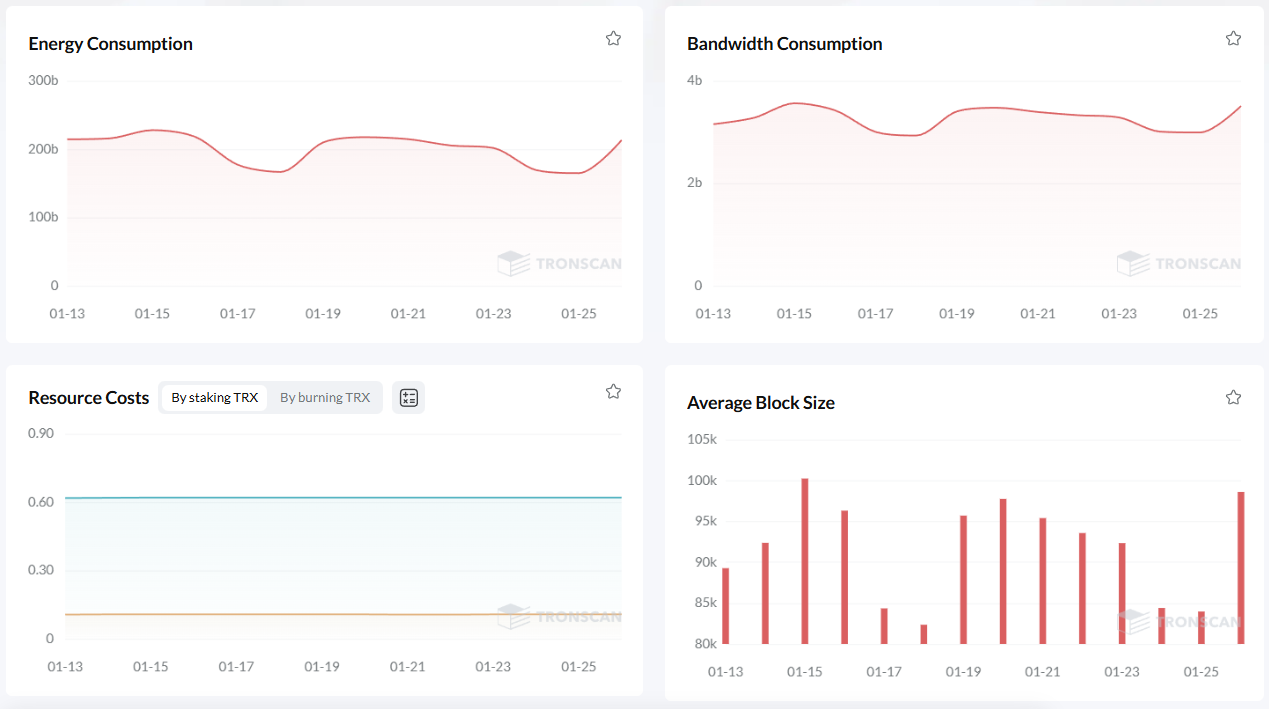

Naturally, there is a bit of a learning curve to shopping with crypto. Volatility and network fees are often causes of concern for newcomers. Yes, transactions can be expensive on some networks for example while congested. Fortunately, these problems have solutions in the ecosystem. This is a point where knowing the underlying mechanics of your blockchain becomes important. For example, payments and transactions are popular on the TRON network, largely made in stablecoin USDT due to its low fees and speed. However, even on TRON, ordinary users can get stuck over-consuming the network and burning more TRX than they need to.

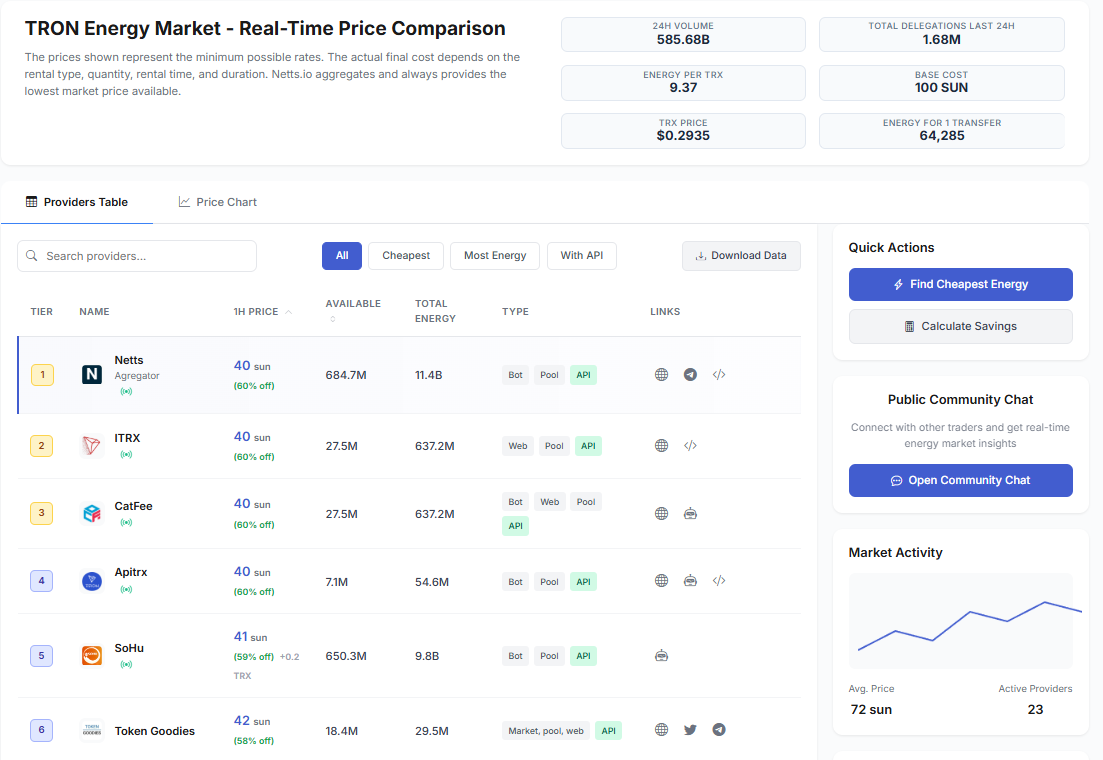

However, shopping on the TRON network is only unique in that here shopping burns the TRX transferred. When making a purchase, your wallet needs two primary resources: Bandwidth and Energy. The former is spent on the size of the transaction data, while the latter is burned when executing smart contracts. And transferring TRON TRC20 token is, in fact, running a smart contract. By default, your wallet gets burned every time you make a purchase. If you shop regularly, you may lose more than you can afford on the rapid burn of your TRX. Of course, the situation can be affected by reasonable actions, since the user can rent Energy. In the case of renting, the cost of transactions is significantly lower. Instead of always burning such a large amount of TRX, you can burn much less at the very beginning. This is how to get a pre-paid processing power for a tiny piece of the burn cost. Renting resources: why would a buyer do that? If you have found an acceptable option for you to buy something at TRON, then renting Energy is a kind of membership that allows you not to pay for shipping. Assume you buy something every week, such as art and digital subscriptions, and then need to send to a friend to buy something together.

The novice user does not make use of this practice but the adept user does. The novice whinges about fees; the power user leverages them. There are different service and platforms that enable to do so by renting an exact amount (in GigaJoules) for a specific period. It’s a small move that changes the economics of using crypto for everyday shopping. Instead of fretting that the fee will chew up your buying power, you lock in your resources ahead of time. This predictability makes spending crypto feel a lot more like the flat-fee or no fee models we already know and hate, but without centralization. It eliminates the friction of “is it worth paying that much for this transaction?” and brings the attention back to “do I choose this item?”

Optimizing Your Crypto Shopping Strategy

To really maximize shopping with cryptocurrency, one should consider best practices. First, verify you’re on the correct network. It is common to send tokens on the incorrect network and you may lose funds in this fashion. Second, have your shopping wallet and savings wallet in separate places. It reduces your exposure in the event of a hack. Third, like you say yourself, take care of your network. If you are in TRON, don't just burn TRX. Explore TRON Energy leasing alternatives. It’s a small piece of administrative work that will lead to big savings.

1. Maintain a “spending” wallet with just enough to cover the need.

2. Double-check the recipient address, comparing the start and end of the address.

3. Purchase using stablecoins like USDT to avoid price volatility while the transaction is being completed.

4. Track congestion and pay lower fees in off hours — less of a factor for networks like TRON.

5. Keep your wallet software up to date, so you always have the most current security features.

6. Learn resource cost models such as Bandwidth and Energy to reduce transactional costs.

By following these steps, online shopping is safe and easy. You quit having to worry about the details and get on with enjoying life. The technology should work for you, not the other way around. The more you get used to it, the more intolerable the friction of legacy banking will feel. You’ll find yourself wondering how you ever tolerated the arbitrary limits, the glacially slow processing times and not having any privacy. Switching to crypto isn’t merely a matter of switching currencies, but rather of upgrading your entire experience as a consumer.

Stablecoins in the Retail Space

One of the big drivers for this has been stablecoins. For years, the volatility of digital currencies like Bitcoin made them less than ideal for everyday shopping. If your money can be worth 10 percent less in an hour, you hesitate to spend it and businesses struggle and are slow to accept it. Stablecoins found a way around this by linking their value to fiat money such as the dollar. This provides a familiar shopping experience – but one that is augmented by the virtues of blockchain.” You could keep your shopping budget in USDT or USDC and understand what you were able to spend without an added calculation.

Stablecoins in conjunction with a express, low-cost network is the endgame payment rail. You enjoy both reliability in planning and lightning-fast transaction speeds. That calculus is what is behind the adoption on digital goods platforms. It is also favored among sellers because they receive the money immediately, with none of the risk of chargebacks — a major problem in traditional retail. And buyers like it for the same reasons we’ve already discussed: speed, privacy and control. It’s a win-win for both sides, and the process is something that more and more of us are coming to expect with internet shopping.

Looking Ahead

There’s no question the future of shopping is digital and decentralized. We’re heading toward a world in which value replicates as easily as information. Banks meanwhile are trapped in the past with woefully outdated systems. Facing an online fintech movement that could explode — literally. Although regulators may try to apply rules to it, the decentralized nature of crypto is such that you cannot strangle the core utility. Innovation moves faster than legislation. Peer-to-peer payments are no longer going away.

And that's great news for the consumer. It means more competition, lower prices and better service. It connotes that you are the owner of your money, not only a custodian. And people will stop fearing the new when its benefits cannot be denied. Just as we don’t really think about the byzantine protocols behind an email, one day we won’t care to know much about the inner workings of a blockchain that allows us to buy a cup of joe. It will all just “be paying,” but improved. But till the time that happens, a proactive learner who knows how to look after your wallet, secure your keys and rent TRON Energy, will extract every ounce of juice from this revolution.

The future is not passive, at least as far as the smart shopper of tomorrow goes. They are informed. They know that everything has a cost, and how to minimize the cost of each transaction. They value their privacy and do what they can to maintain it. They make no bones about it: the old way of banking doesn’t work for a global, digital life — and they know it. They are partaking into more than just an alternative way to pay, they’re becoming part of a world of improved financial freedom and efficacy.

In the world of running your crypto better, network cost management services create an indispensable tool in your digital wallet. And for those constantly using the TRON network, smart shopping for energy rates can make all the difference in fee elimination. Netts service - TRON Energy Market Aggregator - compares and rents Energy at minimum rates possible! It offers over 20 providers on aggregation directly on a real-time basis to guarantee at all times you are receiving the lowest market price available for your transactions.