Crypto and Mathematics: Is It Possible to Beat the Market?

Jim Simons showed math can find market edges — today’s quants port those ideas to on-chain data, models and limits where no formula guarantees a win.

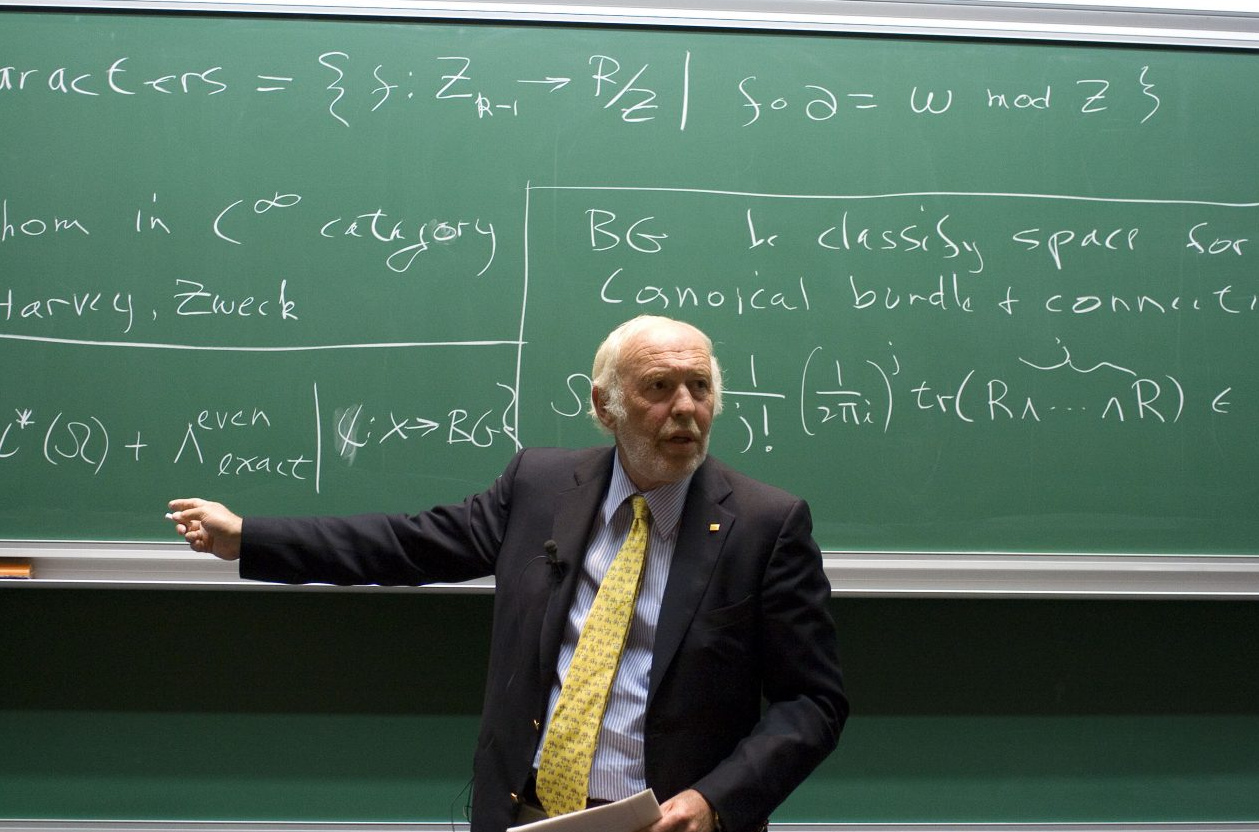

The story of Jim Simons is not that of a person who manages money, although he is one of the most successful money managers in the world. It is the tale of a man who peered into the squirming, uneasy world of Wall Street and saw not chaos but order — mathematical order in the form of mysterious and beautiful patterns. Simons, a renowned mathematician and ex-NSA code-breaker, had established the hedge fund Renaissance Technologies in 1982.

Its flagship fund, the secretive Medallion Fund, would later emerge as the most lucrative in history, yielding mind-boggling average annual returns of over 60% for three decades. While others trusted their intuition, their guts, and standard analyses, Simons and his army of PhDs in mathematics, physics and statistics trusted only two things: the data itself — electronic whispers from Wall Street replicated on their computers — and the models they built to interpret it. The man who broke Wall Street’s code; he was the “Quant King.” What set Renaissance apart, though, was its culture — less that of a high-rolling Wall Street firm than a university mathematics department.

Simons cultivated an atmosphere of high-level collaboration and curiosity, famously employing experts who had little to no finance experience. He thought that the best ideas came from arriving at the market with a new set of eyes, free from the preconceived notions of Wall Street. It was an offbeat style that paid; it enabled them to develop practices in statistical arbitrage and high-frequency trading well beyond the industry’s norm for years.

Simons’s own biography was hardly that of a Wall Street titan. Long before he revolutionized investing, he was a highly regarded academic. His contributions in geometry and topology would contribute to the discovery of Chern-Simons form that was considered later as a significant complex mathematical object for string theory and quantum field theory. This capacity for abstract, multi-dimensional thinking set him apart. He didn’t see the market as a collection of individual companies, but rather as a dynamic system ruled by underlying principles, like a physical force. He was taking investing as a scientific problem, as if you could solve it by collecting sufficient data and applying the appropriate algorithms to separate signal from noise.

His team hoovered up huge amounts of data, from historical stock prices to weather patterns, looking for any predictable, non-random effect they could trade off. They created sophisticated algorithms that could place trades automatically to profit from minuscule, fleeting inefficiencies that human eyes could never even see. They didn’t predict the market’s direction over the long term; they just found tiny, reliable edges and then plundered them millions of times over.

This approach was also hugely reliant on clean data and strong infrastructure — topics that traditional funds by-and-large were seriously lacking. The key belief was that with enough data, subtle patterns predicting consumer behaviors would emerge — and those patterns might be very small but could still lead to massive profits if they were leveraged at scale.

An Old Strategy, but With a New Frontier

Of course today’s financial world is a different beast from the one Simons conquered so long ago. The markets are faster, more globalized and infinitely more complicated. The low-hanging fruit of inefficiency that the Medallion Fund plucked has long been removed from the market, arbitraged away by hordes of quantitative traders who followed in Simons’s wake.

His original models, if they were unveiled today, may appear quaint or irrelevant to the breakneck, algorithmic trading of the day. However, to take that as a reason to disown his legacy would be entirely the wrong lesson. The real genius was not in any one model, but in the basic approach: that markets, every market, even those that seem perfectly efficient, are full of cracks and seams. “The idea is to construct a mathematical lens sharp enough to observe them.”

And now, this same approach is being used on the newest and most out-there financial frontier: cryptocurrencies. With its sky-high volatility, rapid developments and the fact that it is a digital native (with only walled gardens represented by centralized exchanges), economists find crypto heaven. It is a data-based world, where all transactions are written into an unchangeable public ledger. This offers mathematicians and data scientists a rich mine to explore.

This on-chain data consists of transaction volumes, wallet balances, smart contract activity and network fees, providing a transparent and real-time view into the market’s plumbing. This is further compounded by a deluge of off-chain data, such as exchange order book depth or the loud — and sometimes chaotic — influence of social media sentiment on platforms like Twitter and Reddit. The task is formidable but the principle is straightforward.

The aim is not to predict whether Bitcoin will reach a new all-time high next year, but to discover the subtle, exploitable patterns in the daily chaos of the market. It’s finding what structural inefficiencies there are, whether in the pricing of derivatives, the flow of capital between exchanges or even the fundamental mechanics of a blockchain’s transaction system.” The quest for alpha has gone from trading floors of Wall Street to the decentralized world of blockchain.

Modern Mathematical Arsenal

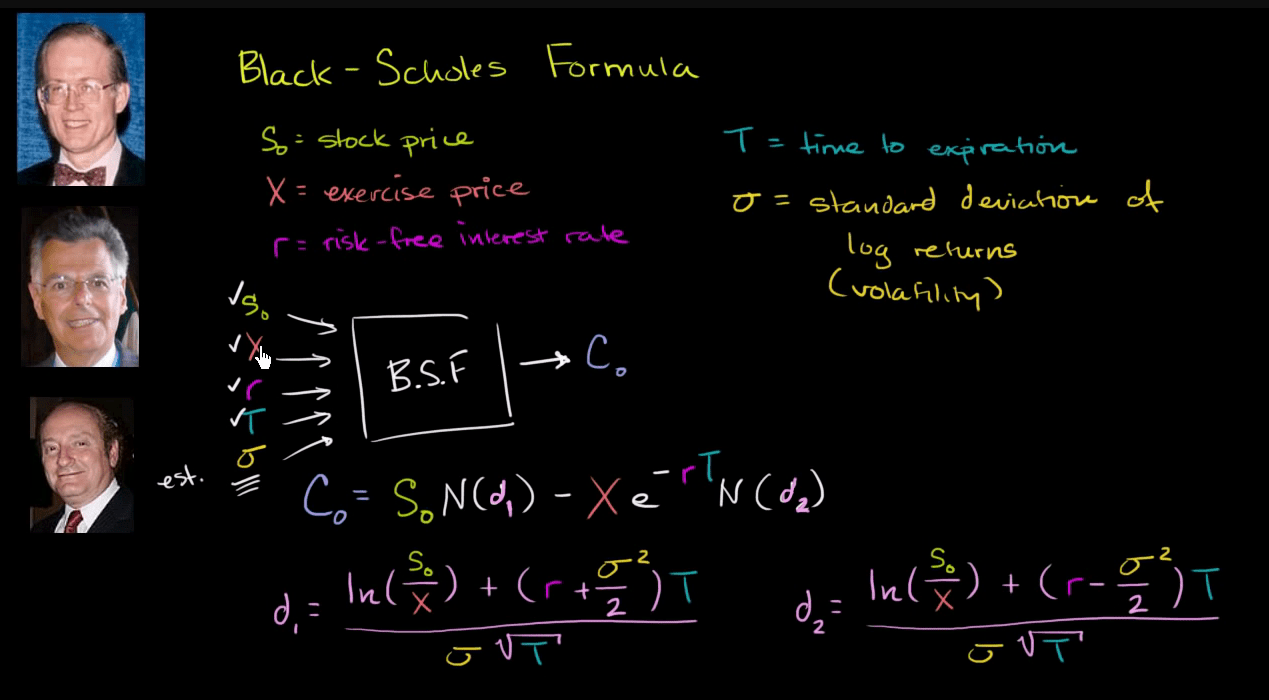

To help them traverse this new landscape, today’s quants are armed with an extensive and sophisticated arsenal of mathematical models that present different ways to frame and understand what is happening in the markets. They range from modified versions of classic financial theories to entirely new models designed to address the unique idiosyncrasies of digital assets. One of the most basic ideas, deriving from traditional finance, is the Black-Scholes model. Fundamentally, it is a formula to calculate the price of derivatives.

On a set of idealized assumptions — markets are perfectly efficient, asset prices follow a predictable, random walk known as geometric Brownian motion and volatility is constant. And although the crypto market is far from perfect, Black-Scholes is still an essential intellectual basis that we need to compare our options pricing against in this world of burgeoning crypto derivatives. But its stiff assumptions often break down in the land of cryptos, where volatility is famously unshackled and “fat-tailed” events — that is, extreme price swings — are a regular occurrence.

To overcome these limitations, quants often use more sophisticated methods. One of these categories is called Stochastic Volatility Jump Models. These models are in response to the failure of Black-Scholes. They recognize two key market facts: that volatility is not constant, instead, it changes with time in a random (stochastic) fashion; and prices might suffer sudden major jumps or swings (for example due to big news releases or liquidations). Using mathematical terms to account for fluctuating volatility as well as significant price jumps, such models offer a more realistic (though complex) view on the dynamics of asset prices — and may prove particularly valuable in the turbulent world of crypto.

Yet another set of such tools are Monte Carlo methods. Instead of a single beautiful equation as in Black-Scholes, the Monte Carlo is a blunt force approach. It works by conducting many thousands, if not millions, of random simulations of the market’s future path based on initial inputs like today’s price and some measure of estimated volatility.

By examining the whole distribution of these simulated outcomes, a trader can develop a probabilistic intuition about the worth of an option derivative or about how much risk there is in a portfolio. That flexibility is invaluable in crypto, where assets frequently lack the long historical track record required by more traditional models, and where complex, path-dependent derivatives are increasingly prevalent.

This is precisely where more modern views on portfolio construction, such as the Stochastic Portfolio Theory (SPT) may come in. SPT, formulated by E. Robert Fernholz, is descriptive rather prescriptive. It doesn’t start from the assumption that markets are perfectly efficient; instead, it works off of hypothetical behaviour of actual, observable market prices as continuous-time random processes. This is in contrast to the classic portfolio theory where an investor minimizes the expected value of cycle returns and a constant level of variance.

This in turn permits the very strategies that seek to outperform the market as a whole, not by predicting which way it will go, but rather by periodically rebalancing their portfolio to pressure the varying growth rates of its constituents. It’s a more nuanced take, one that is better adapted to the multiplicity and lack of correlation seen in the crypto world.

These are complemented by a second wave of methods that were designed for the digital era. In the chart-designing rooms, crypto prices are being modelled using methods borrowed from Bayesian frameworks to treat them like particles under a dynamic non-linear potential. The key idea behind Bayesian statistics is beautiful in its simplicity: you have a prior belief about something and then update that belief as you gather new evidence. In the fast-paced world of crypto, that’s a strong concept. A Bayesian model is able to update its forecasts continuously as new price data, transaction volumes or perhaps even measures of social media sentiment arrive, allowing it to respond in real time as market conditions change in a way more static models cannot.

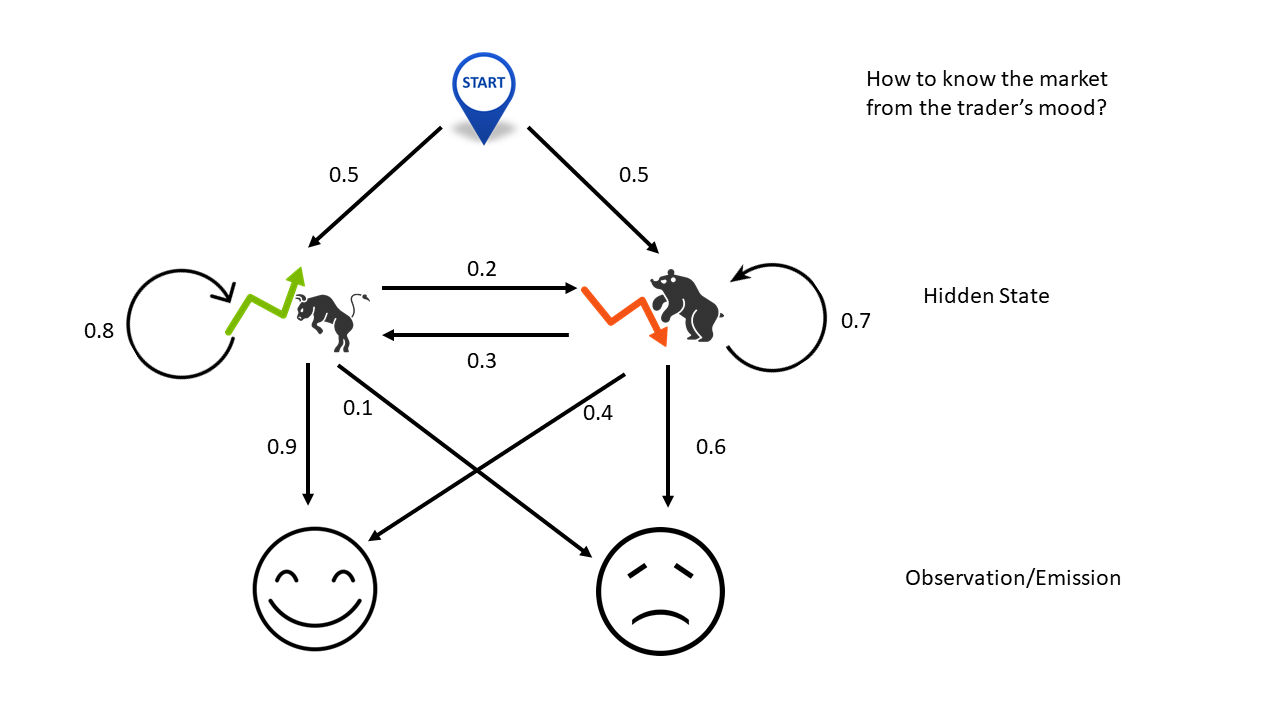

Yet another strong tool is the Hidden Markov Model (HMM). An HMM assumes that the market can be in various different “regimes” or hidden states — for instance, a ‘bull run’ state with high returns and low volatility, a bear market regime with negative returns and high volatility or a sideways consolidation regime. The model examines the price and tries to learn what state of the market it is in, and its next most probable state. In a market as subject to rapid pendulum swings of sentiment as crypto, where mood can change from euphoria to panic on an hourly basis, HMMs are the sort of tools that can shed light on these regime changes and turn traders onto skills that’ll allow them to adapt accordingly.

Last, Vector Autoregression (VAR) models assist in disentangling the intricate network of relationships between alternate cryptocurrencies. In a market with thousands of inter-connected tokens, you’d be naive to look at anyone in isolation. The VAR model then deals with this by considering many assets as a system. It can explore how a price shock to a major asset like Ethereum ripples through the ecosystem, impacting dozens of other token prices in the DeFi and NFT ecosystem. It maps the causal network and contagion effects in the market, it shows which coins lead the pack and which ones follow, delivering a more complete overview of systemic risk and opportunity.

Power And Pitfalls Of A Coded Market

Using these advanced mathematical models to study the crypto-markets offers great promise, but it is also not devoid of danger. The benefits are clear: the data-driven road map through what is otherwise a famously speculative terrain. But every quant also knows that their models are an abstraction of reality, and leaning too far into them can spell ruin. That is, there’s a balancing act that’s necessary here: The potential advantages have to be weighed against the intrinsic unlikeability of quant funds — so as not to end up like those others.

Main advantages and disadvantages are summarised below:

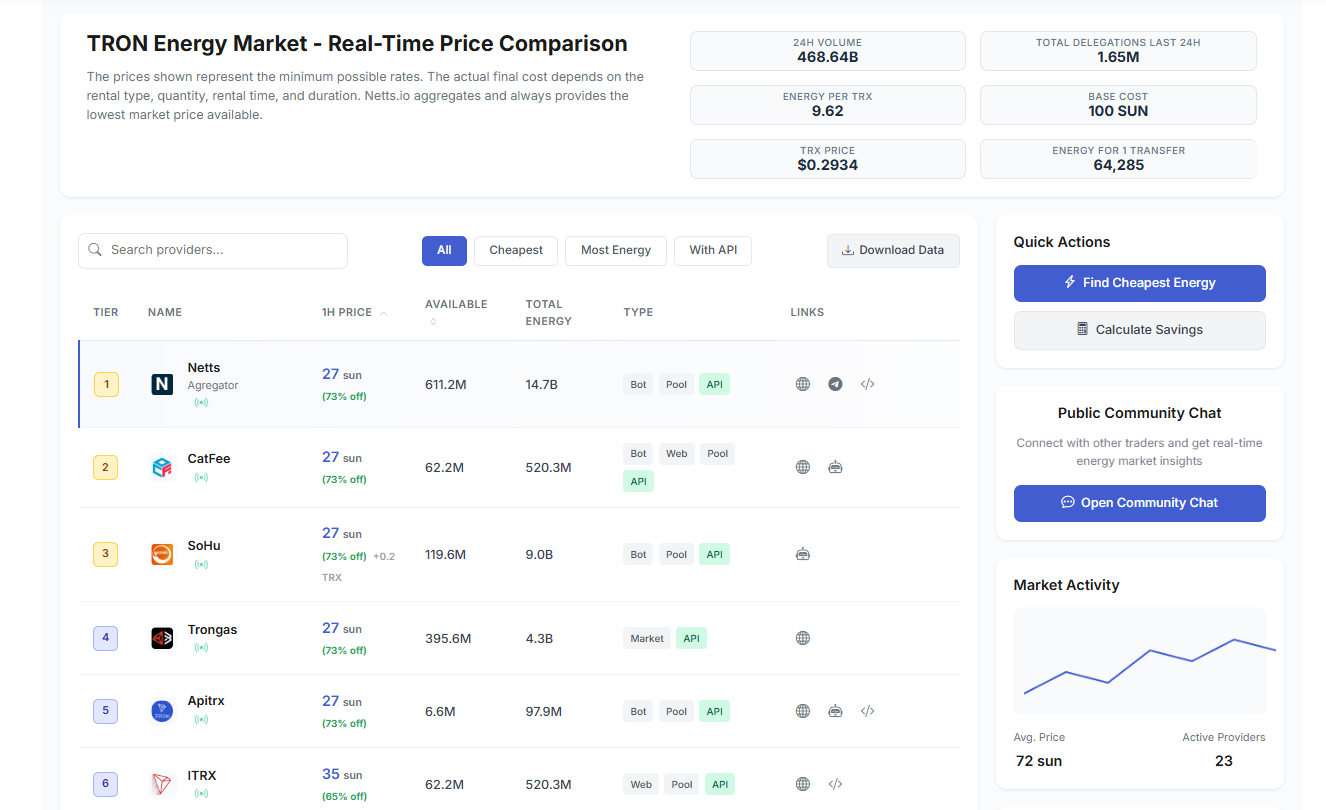

1. Pros: As to the advantage there is that we are able to compute some meaningful signal out of colossal data. Quantitative models can pick up nuanced correlations and patterns hiding in an ocean of thousands of assets and millions of trades that no human ever could. This, in turn leads to a more disciplined and methodical approach to risk management where losses can be measured and managed. On another level though, these models are the workhorses of algo trading – they enable strategies to be executed automatically at a rate that can take advantage of opportunities as short lived as milliseconds. This “sniffing” power is vital in complicated sub-sectors such as the TRON Energy market – where rates and quantities of availability change at lightning speed. It takes out the fear and greed from trading when we stick to a systematic way of doing things, which results in more consistent execution being made.

2. Cons: The biggest risk is ‘model risk.’ Any model is only as good as the assumptions from which it's formulated. When those assumptions are incorrect, or the market conditions change in some way the model was not designed to accommodate, it can fail spectacularly. The LTCM cases should remain timeless simply to show what happens when you ruin it for everyone due only to your short-term greed. The quality of the input data is another key weak point; faulty or ‘dirty’ data can result in a misguided decision and expensive trading mistake. Finally, numerical models are particularly poor at forecasting "black swan" events. Sudden regulatory attacks, huge exchange hacks or unforeseen technological advances are occurrences that fall outside the statistical patterns of historical data and can make even the most high-tech models obsolete overnight.

These models are tools in the end, not crystal balls. They offer investors some amount of what might be called a probabilistic edge, or a way to tilt the odds marginally in one’s favor across many trades. The best quantitative firms do not use them as a source of absolute truth, but as a way to help understand and cope with the inherent uncertainty in markets. They’re constantly iterating on models, tweaking them, and occasionally ditching them as the market changes; they know that the map is not the territory. The highly dynamic interaction of systems like the Energy rentals market of TRON is an example for this adaption, since new providers and pricing mechanisms constantly change the environment. A successful quant firm is as much a risk management firm as it is a prediction firm.

Hunt for the Next Simons

There is more to the Jim Simons and Medallion Fund story than the improbable riches it generated: It is a tale of a different way of thinking. He demonstrated that even in a profession influenced by human emotion and intuition, a sound, empirical method could win out. He showed that beneath the noise and fury of the markets there is a mathematical logic to how prices move that, while it doesn’t always lead to accurate predictions, can create opportunities for investment that are well grounded. His legacy looms large over the financial world — a living rebuke to the system, a reminder that the market’s code is, indeed, crackable. It reimagined what was achievable, and changed the paradigm of star stock-pickers versus anonymous teams of scientists.

As a new cadre of talented people apply themselves to the digital frontier that is cryptocurrency, it’s not a matter of if someone will duplicate his success but when. The crypto market, open for swashbuckling data science, entirely digital and never sleeping, is perhaps the perfect environment for a 21st-century quantitative revolution. The tools are more sophisticated, the data is more abundant, and the opportunities to discover and exploit inefficiencies are everywhere. It is an arena where novelty and mathematical experimentation are richly rewarded.

But the next Simons will have his work cut out for him. The competition is far greater too, with hundreds of quant funds, large and small scouring crypto markets for alpha. Market itself is also reflexive; the more quants who are taking advantage of an inefficiency, they tend to go away. It is an arms race that never ends, requiring more and more complex models and faster and faster execution times. It’s a perilous trip, one filled with gargantuan challenges along the way, but if there is anything to learn from Jim Simons, it’s that perhaps, just maybe, you too can beat the market — if you have enough mathematical genius and computing horsepower behind your back. That's where Netts Energy Market can help you find a strong Energy price right when you need it: