Never-ending Competition Within Layer 2: Who's Winning?

Arbitrum, Optimism, Base, zkSync, Starknet, Polygon — who's actually winning the Layer 2 fight, and what each contender is fighting for.

A funny type of resistance creeps in every time a technology asks its users to learn just one more new thing. Even in new fields — and crypto is as text-book an example of a new field as you could get, the audience builds a kind of internal normal, and then even barely deviating from that internal normal raises suspicion. By the time you mention Arbitrum, to people who wax lyrical about Ethereum at a dinner party in front of their friends, they will roll their eyes and say "but we learned that already;" not because Arbitrum is particularly difficult to understand once someone explains it to you but rather that these folk either got the first thing and frankly weren't looking for a second. The first migration was educational. The second feels like homework.

More than any technical aspects, this dynamic has characterized the Layer 2 contest. The teams that built these networks knew from day one that they were not selling a faster, cheaper Ethereum. They had to fight against the existing user base that was already undersettled on the original chain and did not have a reason to leave. Enough for a new bridge to be worth the friction of learning — a new explorer, a new flow of contracts to approve and an entirely different mental model for which assets live where. That challenge has spurred some of the fiercest competition in crypto (save for perhaps early-DeFi protocol wars) — and unlike most fights in the industry this one actually has technical merit behind it.

What Layer 2 Actually Solves

Native Ethereum is expensive. This is expensive because the network is shared by every one wanting to do something with anything built on top of it, and every block could perform only a limited amount of computation. The outcome is a fee market where transactions are prioritized by user willingness to pay; the top of that curve has been economically infeasible for normal users to do anything at all during peak periods. A simple swap could set you back 50 dollars in fees. A complex DeFi transaction is 200. The network was obviously functional, in that it did what networks are meant to do — but for an increasingly small group of people.

Layer 2 networks were developed for this, moving most of the computation off-chain while still retaining the security benefits from the Ethereum ecosystem. The particulars are different depending on the terms — optimistic rollups, zero-knowledge rollups, validiums, plasma chains and so on — but the fundamental reasoning remains the same. The Layer 2 is the place where low fee high throughput transactions can happen, periodic summaries are committed to Ethereum where the security derives from and gives a user experience that feels like Ethereum but only costs very small fractions of the original. The complexity is real. The trade-offs are real. However, the fundamental value proposition — same security model, far lower cost — proved to be precisely what enough users wanted in order to make the entire category viable.

Through the mid-2020s, total value locked across all major Layer 2 networks had reached thirty billion dollars… then forty… and more. The total transaction number on Layer 2s routed far higher than Ethereum Mainnet. Whatever the remaining debates over purity or fragmentation, the Layer 2 thesis had been proven in literal terms: people were using them.

Meet the Contenders

By now, the main contenders in Layer 2 have become settled more or less tightly defined, even within a sector that can see different relative rankings each quarter. They each have a different identity, a different backer, and a different theory of victory.

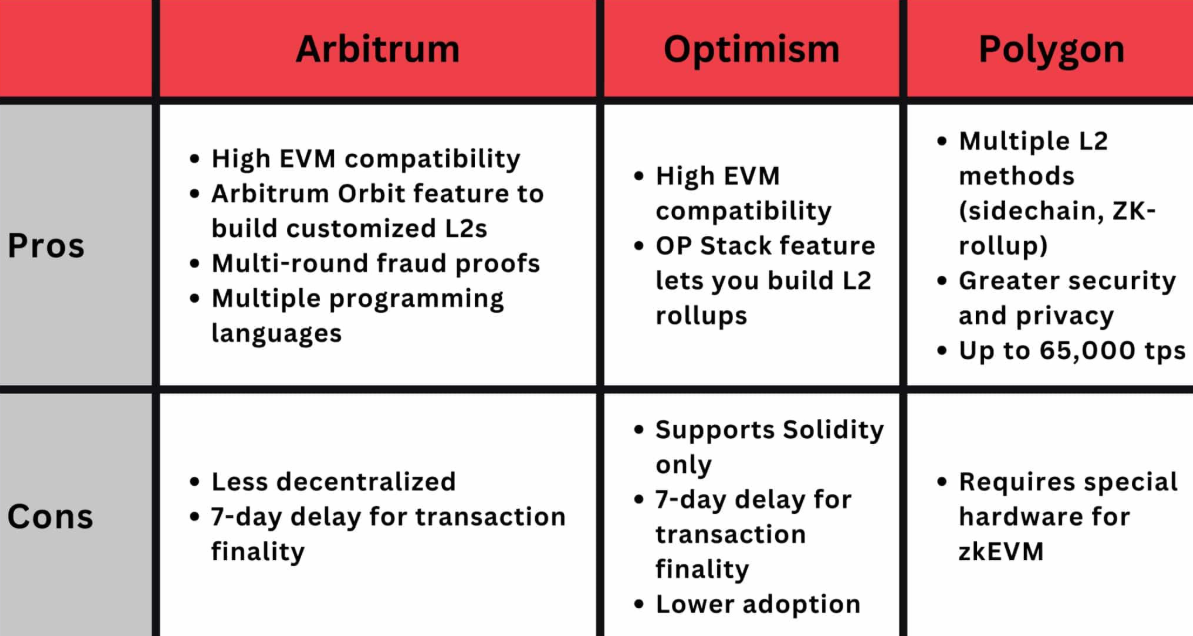

Developed by Offchain Labs, Arbitrum was for years the largest Layer 2 by total value locked, and still holds a very high tier within our new architecture. Its ecosystem has appealed to a steady stream of DeFi protocols that needed Ethereum compatibility without the Ethereum cost, and it is powered by a proven, well-understood optimistic rollup design. The ARB token launched in March 2023 with one of the largest airdrops in crypto history, with Arbitrum thoroughly decentralizing its ecosystem governance through the Arbitrum DAO. Maturity and stability is where Arbitrum shines. Its main challenge is that its design philosophy behind the original architecture is over a few generations of many surrounding competing designs, and as the new generation of zk based rollups keeps coming on stream now increasingly such differences are marketing than technological ones.

The closest peer to Arbitrum (in terms of design and history) is Optimism, operated under OP Labs. Also employs optimistic rollups, also has a robust ecosystem, and also has both a token (OP) and an evolving governance model.

By far the most distinguishing move from Optimism has been its Superchain initiative — a vision centered on multiple Layer 2 networks that share an underlying technical foundation (the OP Stack) while interoperation and value capture flows back to the base layer. Base (2023) — Base is an Ethereum Layer 2 from Coinbase that utilizes the OP Stack and has ranked among the largest Layer 2 networks by user activity. Others have built off the same ground work. The most important open question out there is whether the Superchain will become the standard substrate for an entire category or remain one of several competing visions.

Base while technically a deployment of the OP Stack constitutes such a large and culturally distinct entity that it deserves specifically calling out as a contender across its own ecosystem. Coinbase collateralizes it by providing the industry's deepest fiat onramp and disciplined regulatory positioning. For all of 2024 and through much of 2026, Base led the Layer 2 group with daily active users — propelled by viral consumer apps, memecoin activity, and Coinbase users regularly learning they could move on-chain for pennies. There is no token for Base, which any way you slice it has drawn fire or found fans depending on who you ask.

The zero-knowledge rollup camp is represented by zkSync, built by Matter Labs. Optimistic rollups rely on a challenge period, but ZK crypto is mathematically more elegant as it produces cryptographic proof of correctness — at the cost of engineering complexity that took years to get production-ready. The ZK token has launched, zkSync Era is actually live and the network has been adopted. The long term winner is zk technology, and optimistic rollups will ultimately be crowded out. The question is whether or not that displacement occurs on a timeline than matters to current investors.

Another major zk-rollup with bona fide ecosystem traction is Starknet, built by StarkWare. The Ethereum-native rollup uses a different proving system (STARKs instead of SNARKs) and programming language (Cairo instead of Solidity) — this has been beneficial for attracting dedicated developer community while negatively impacting compatibility with Ethereum's existing ecosystem. The STRK token was launched at the beginning of 2024. Starknet is betting that as the industry matures, the technical advantages of its approach will come into play.

Polygon, the granddaddy of all layers for Ethereum scaling, has pivoted several times. Polygon has evolved from a Plasma-based sidechain to its own proof-of-stake chain, to a launchpad for zkEVM, and with it a new position in the ecosystem: the AggLayer — settlement layer of a whole ecosystem of Polygon-CDK chains. The underlying token is POL, a rebranded MATIC. Polygon has the advantage of having been at this longer than anyone else, with partnerships, developer relationships and institutional integrations to match. The challenge it faces is that all the multiple strategic pivots since have led to a slight skepticism over what exactly the project really is.

Punches That Landed

A boxing metaphor will only go so far, but it captures something true about how this contest plays out. A specified, credible technical case for why every team eventually wins. Those cases have been made to the investors who back these projects. The same thing that changes capital from a maybe to a yes is the same thing that moves casual crypto users from chain to chain — observable evidence. Layer 2s with users, with TVL, with successful apps running on it, developers shipping things — that Layer 2 attracts more of all of them. Once the flywheel gets going, it is very difficult to stop.

Base led the flywheel through 2024 and 2025. Coinbase brand was a non-negligible trust anchor. Without a token, early users were not speculating on Base itself but rather the applications built atop it which made for clearer activity stats. The ability to onboard with Coinbase Pay streamlined the process for millions of users who already had accounts on exchange. This unleashed a network that, by certain metrics, surpassed the older Layer 2s in pure user activity. Whether that translates into long-term hegemony is debatable. A second lesson has to do with network effects in crypto, which have been proven more durable (and brittle) than anyone thought.

At least via raw ecosystem depth, Arbitrum and Optimism have held their ground. These networks with built-in DeFi protocols, from Aave and Uniswap to GMX, Synthetix, Velodrome to a hundred others represent huge switching costs both for the actual protocols as well as the users that have built positions on top of them. Taking a protocol from Arbitrum to use a competitor is not merely an idiosyncratic technical exercise, it requires taking the time to educate users about why this was necessary, to rebuild liquidity in that protocol on the new chain, re-enter partnerships that were formed with aiming at achieving synergy effects and so on — all of which involve substantial reputational risk. This gravitational pull has kept the established Layer 2s competitive in light of the challenges of up and coming ones.

The zk-based networks are still in the process of proving their performance during load. The technical achievements are remarkable. This user-facing experience is, arguably, indistinguishable from optimistic rollups; this is both a compliment and an issue — if the user cannot tell the difference, the technical case has to battle a promotional fight. Both zkSync and Starknet are pouring money into ecosystem grants, developer incentives and broadly consumer-focused applications. The results of those investments will unfold over the coming years.

Tokens and What They Tell You

The Layer 2 token economy is its own subplot. Each one of ARB, OP, STRK, ZK and POL has had a different price history, a different unlock schedule — its own narrative. A token price in isolation is not a reflection of the underlying health of the network. Well, on its own it is not also a piece of useless information. These networks on the other hand are priced, albeit imperfectly, as a function of expectations regarding which ones will accrue value over time.

For the most part, ARB and OP have traded as bellwethers of the category with prices that move on general market sentiment about Ethereum scaling rather than network-specific events. Moving over to POL, the journey through Polygon migration has been a bumpy one. ZK and STRK have had a hard time converting technical excitement to price action, partly attributable to token unlock schedules that hit supply during the transition period in which adoption metrics were growing. Arguably, the best performing token is simply not having a token — Base has been criticized for having no tokens, with commentary either predicting a strong Layer 2 does not necessarily need to go through the labor of creating its own crypto asset or making excuses for failing to get around to it.

For applications building atop these networks — especially those which will need to process high transaction volumes such as networks that provide automated Energy refills for TRON users or an API for TRON Energy management, the selection of Layer 2 substrate becoming less a decision and more a foregone conclusion. Many of them deploy on several. The infrastructure has actually matured to the point that adding support for Arbitrum, Optimism, Base and a couple of zk-rollups should be pretty low hanging fruit from an engineering perspective, and the marginal user on each respective network is worth it at scale.

Last Round

The really honest answer to who wins is that winning is happening in several places at once. Base is claiming the consumer audience. Arbitrum and Optimism are winning the depth of the DeFi ecosystem. If you believe that a long-term technical bet pays off, zkSync and Starknet are winning it. The battle for institutional integration, partnerships, and the enterprise narrative: Polygon is winning. What might be the cleverest of the lot are those investors who have been buying up this entire category through this period not just individual winners, because it seems most plausible that rather than one Layer 2 winning out against all other contenders or at least outsized market share, instead both continue to grow as a category and several will survive.

Why this is important for everybody outside of the inner circle. The Layer 2 choice is turning from strategic to routine. The networks are good enough. The bridges are mature enough. The wallets themselves take care of switching chains for you. The user does not have to go all-in on one ecosystem anymore. They could use Base to do one thing, Arbitrum to do another and then a zk-rollup to go do a third, the only difference that really matters is the fee structure and application catalog. This is how, slowly but surely, for an entire technology category what success looks like — when the topic goes from discussion to tool. The big question is whether that championship strap winds up in one set of hands or gets passed around for years. What matters has emerged from the fight itself.

Netts Workspace is an advanced Energy management platform tailored specifically for developers and businesses dealing with large-scale USDT workflows on TRON, featuring professional-grade manual rentals of 32K to 5M Energy units, a smart mode that tracks balance triggers/pauses working hours automatically, a host-mode offering 131K Energy plus 400 Bandwidth during twenty-four-hour cycles, and an automated integration-ready API with whitelisted IP access. It consists of a referral program accruing 15 percent commissions, transaction history with CSV export, control over deposits and withdrawals, as well as a dashboard that shows how much cost savings have been achieved as compared to the burn-TRX baseline — typical operational tooling you get when running any chain on which production workloads have to pay for each interaction.