How Wars Push Civilians and Refugees Towards Crypto

When banks pull out of war zones and currencies collapse, a phone with a stablecoin wallet becomes the last piece of civilization that fits in a pocket.

There is a sound, it turns out, that everyone in a war zone learns to recognize within a few weeks. It is the noise of the final slide of steel curtains being drawn over a bank, where no staff are inside and given the hammers that will follow, it's probably wise to make sure it's all tidied up before something worse. Some of the staff went south, some west, some are still in town but no longer working. The branch manager's vehicle went missing for 30 days. Seven weeks with no need to refill cash machines outdoors, which in other times had been refilled every two weeks. They have been pried open and gutted, two of them. A third was burned one night by nobody knows why. The cell network is up, and the bank's mobile app maybe still works, but transfers larger than a threshold amount are refusing with an unintelligible message. When you call customer service, it plays in two languages that are not useful.

This is the point at which someone who has never thought about crypto a day in their life suddenly realizes why it exists. Not because of some technical argument, not because of any libertarian theory, not for any speculative ambition. They get that because the alternative — the financial system they relied on until last month — has conspicuously and intentionally abandoned them. That mortgage they were paying is still there, just a number on some server. The savings account still exists. In some cases, the credit card remains functional. Yet the institution that swore it would stand behind any of it has determined this town imposes too much operational risk, and the experience on the ground for its customers is that none of it is accessible.

When the Banks Leave First

This pattern holds in modern warfare as well. Banks are commercial entities. These are not being supervised by folks who will work for a paycheck in artillery range. Once serious instability appears to be a possibility, the banks begin contingency planning. Cash gets taken off the shelf and into the safe. Reassigning or dismissing staff. Branches are closing down, sometimes with the paperwork to prove it, sometimes by authorities opening their doors one day only to find that they won't be opened again. The ATMs go offline. Certain transaction types are no longer accepted by the mobile apps. When anyone in the public is told that there is a bank out of operation in their community, the bank has actually been gone for weeks — if not longer — but effectively operational.

What remains for civilians from that point relies upon entirely to what they had amassed ahead of time. Sure, cash works but cash has all sorts of limits — it's heavy, it can be stolen, you cannot cross a border with it and during hyperinflation it is worth less every morning than it was the night before. Foreign currency is even better, but it seems most people in most nations do not keep substantial amounts of foreign currency in their homes. Gold and jewelry kind of work, but how long can one really convert them when local economies go bust at the same time? More and more of what is left in their pockets these days is whatever sits in mobile wallets — and for an increasing number of people that means crypto.

No one evangelized for a shift to happen; it just did. Because the truth is that a smartphone with a custodial wallet, a backup of a seed phrase memorized or hidden somewhere safe and some kind of access to even unreliable mobile internet is the only store of value you can have on you regardless of what happens to local infrastructure. The bank need not be functional. The branch does not necessarily need to be there. The country itself does not technically need to remain a state. The wallet works on the condition that the owner can find a charged phone and signal at any time.

In most of those scenarios, charging the phone is a minor daily logistics issue all its own. A neighbour with a petrol generator stretches wiring through a corridor for an hour every night and people form queues with their phones and power banks to charge. The amount for the call is only a fraction of USDT. Payment in domestic currency, if it is ever done again, has no value because it fluctuates too significantly from morning to afternoon. The wallet that holds savings is the same wallet that powers the device containing it. The arrangement is tenuous, but it is an arrangement.

Logistics of Survival in a World Where Trust Has Crumbled

These are not the types of use cases you read about at crypto conferences. As evidenced by a literal war zone: nobody is yield farming. A DEX pool has no liquidity being provided to it. The real uses are boring, urgent and exclusively between person A and B in circumstances where all other options have failed.

Case 1: someone stuck in a city wants out yet cannot connect to their family who lives abroad to assist him. Wire transfers from foreign countries mysteriously ceased to function; the receiving bank has closed down. Western Union temporarily suspended services in the region. The other is for family to send USDT to a non-custodial wallet on the phone, then sell cash on through informal networks of people who do exactly this — in basements, at markets or agreed meeting points. The conversion rates are punishing. Getting to the meeting point is risky. But the money arrives. A USDT transfer to a wallet in the war zone from abroad takes anything from minutes to hours depending on whether the sender knows what they are doing, and can cost almost nothing. A bank wire, if it even works, takes days and costs a sum no one wants to lose.

Take another case of a family, in exit mode, who needs to pay someone: driver, smuggler, official at some checkpoint who they can persuade to look the other way; and they need to pay it in something that the recipient will demand. Local currency may be in hyperinflationary state where prices change between agreement and payment delivery. They only accept cash dollars even though paper bills are hard to print in that volume. USDT is the glue that holds all of these transactions together, because both parties know — from morning to night — that what they agreed upon this morning can be settled in USDT this evening.

Here is another example (third case) where a good-hearted citizen has elderly parents in the war zone who need medicines. The pharmacy that used to deliver no longer delivers. The pharmacist's son, now in charge running the operation, takes payment in USDT — because his supply chain connects through cousins across the border who do business exclusively in stablecoins. The USDT send takes thirty seconds.

The next day the medicine shows up. The grandfather lives another month. No, this is not a marketing tale. It is the real-world experience of millions of people, literally millions of people in countless conflicts, who never expected to have to use crypto for anything and then ended up using it for everything.

A Fourth Case: you can buy food by paying for it when the supply chains have been broken. Open-air car parks now double as markets, but only a handful of produce can be found there, delivered by independent operators driving lorries through the few remaining passable roads. Now it does not take the local currency. They have no equipment to take cards and the market has no wifi. They approve of some USDT payment via a wallet address that they hold out on a sheet of laminated paper against the front of the stall. The customer scans the QR code, signs the transaction via their phone, and walks out with their groceries. The entire transaction is quicker than it would take to fumble around in a wallet for cash.

Life After Crossing the Border

Things are better and the same for those who do escape. This reduces the immediate physical danger. Yet the financial isolation remains for many, frequently for years: refugees from conflict zones tend to be unbanked in their host countries — either by regulatory complexities or a lack of documentation, or simply the fact that no one wants to open an account for someone unable to provide an address they can return home to, let alone any clear paper trail.

Crypto fills the gap. Spending in refugee camps and informal housing across multiple regions, the ones that have stashed even a modest amount of digital wealth use those funds to support themselves and back home. They do freelance work paid out in stablecoins because the jobs they qualify for on the standard currency paying places require bank accounts that these workers don't have. They send their relatives who remain in the war zone small USDT transfers every so often — amounts that would have vanished due to fees in traditional remittance services but arrive intact on stablecoin transfers. They cover the cost of medicine, school fees, transport; all simply recurring obligations that do not cease in their existence because the family is more dispersed across geographical lines. With proper renting of Energy, the USDT gas fee on TRON for a single transfer can be measured in cents — this means tiny payments — completely unreachable for traditional finance — come to life.

This collateral freelance economy is another under-the-radar development all of its own. The on-demand remote work platforms are such that a big part of these digital workers are comprised of displaced workers of some rich countries relatively surrounding conflict zones, and stablecoin is the preferred way for quite some time already in this new segment. They do not have to wait for a check to clear, pay between 5-10 percent in remittance fees and explain to an angry compliance officer why someone else from a refugee camp is being paid by a company issuing invoices from Berlin. The labour is complete, the wallet has been topped up and the worker can change what they need into local currency but keep everything else in dollars.

Whatever the situation, host countries react very differently to all this. So some have incorporated quiet acceptance into their administrative routines, realizing that self-sufficient refugees do not require as many services from the host government. Others have responded with restrictions, suspicions, a further burden of compliance. The refugees, in most if not all cases, will find a work around whatever the obstacle is. They survived a war as it is. The paperwork of a peaceful country is an easier nut to crack.

Phone as Hopeless Last Resort

The second and deeper observation that comes from all of the above — made by anyone who has watched it first hand — is that for people in extremis, a phone with a wallet on it ceases to be merely a financial instrument. It is a kind of personal infrastructure that attaches the owner to the outside world that still works. While the phone still works, while the wallet still works and there is some signal available somewhere, the person on the receiving end has a means to function in a global economy that hasn't collapsed along with their local one.

That is not a small thing. Those who have lived through hyperinflations — not everyone, but enough — do not simply think of it as poverty; they think of it as a specific zone of mental tiredness: waking to the experience that numbers are moving in the wrong direction every day, planning is impossible, there are no savings because whatever small reserve you can scrape together vaporizes before you can use it.

For these people, stablecoins offer something that is truly scarce: a digit which does not change. The savings won't change in real value from one day to the next. The transfer you are promised will come in the amount they told you. In a world where practically every other asset is declining, hope stays still, both in terms of psychology and finance.

Hope, in this situation, is hardly a gentle virtue. It is the fuel for all of those things that run your style or operation. Surviving, in the minds of people in war zones, is a string of tiny choices a future must be reached because some part of them believes that there exists one. A functioning wallet is a tiny but concrete example of that belief. It is evidence that at least one person somewhere can still be reached. It signifies that even after your local economy has turned its back, the global economy still sees you. In a way it is the last piece of civilization that you can carry around in your pocket — and for those stuck in the most extreme positions modern history will allow, even holding on to it may be what allows them to make the next decision.

And when we all spend so much bloody time talking about speculation, regulation, technical roadmaps — and comparing other chains to us. Hardly any of this dialogue lands with the people who are actually using it to live. Those are not the kinds of people you see on the conference circuit. These are not thought-leading articles. They're, silently, feeding their families with stablecoins and a strange lack of loud voices in the conversation around crypto surrounding them is perhaps one of the less visible misalignments within how this industry talks about itself.

Silent Maths of One Transfer

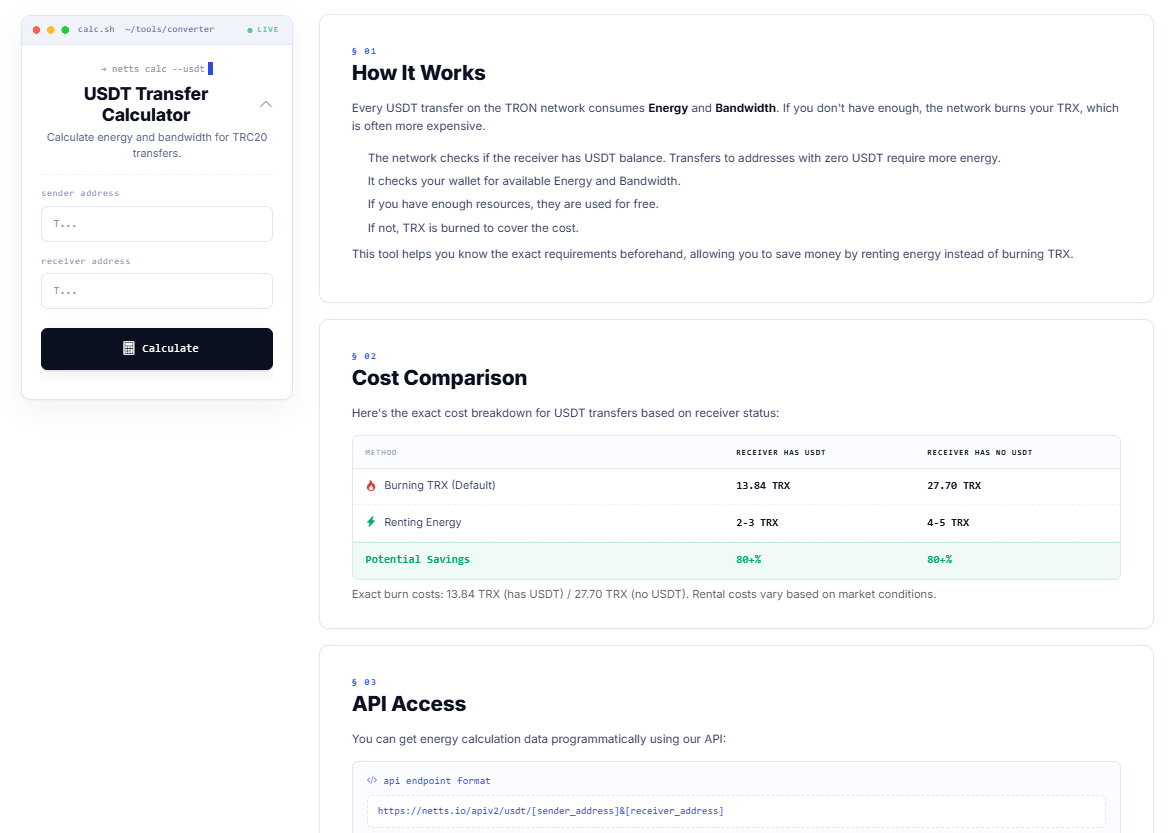

For anyone moving stablecoins on TRON for reasons connected to any of the above, the Netts.io USDT Transfer Calculator calculates the precise Energy and Bandwidth required to execute any given send, demonstrates the difference between burning TRX vs renting Energy and enables a sender to understand ahead of time what the actual transaction will cost.

A USDT transfer to an address which owns USDT by default will consume nearly 13.84 TRX if you pay with this fee method; but if you rent Energy for the same transfer, then it costs about 2-3 TRX. The difference is even larger — 27.70 TRX burned, only 4-5 TRX rented for transfers to new addresses with zero USDT balance. These savings come up to real cash-in-hand for small recurring payments that families in hard times need to make rather than disappear into a network fee structure built for users that never have had to worry whether their next transaction would be the last one they could afford.